Savings Account vs Fixed Deposit: Which Is Better for You?

A practical, India-specific comparison — interest rates, liquidity, tax treatment, and the situations where each one makes more sense.

| Quick Summary — Savings Account vs Fixed Deposit • Savings account: fully liquid, lower interest (2.5–6.75%+ depending on bank type, as of May 2026), no lock-in. • Fixed deposit (FD): higher interest (6–8%+), money locked for a chosen tenure, penalty on early withdrawal. • Use a savings account for: emergency fund, monthly expense buffer, short-term parking of funds. • Use an FD for: money you will not need for 3 months to 5 years and want a guaranteed return. • Both are insured up to ₹5 lakh per depositor per bank by DICGC. • Neither is an investment — both are savings instruments. For wealth creation, other options may be worth exploring. |

What Is a Savings Account and What Is an FD?

If you have ever wondered “savings account vs FD — which is better in India“, the honest answer is: it depends entirely on what you need the money to do. These are two of the most widely used savings instruments in India, and they serve different purposes. Understanding the difference is a foundational personal finance skill.

Savings account

A savings account is a deposit account held at a bank or small finance bank where you park money you may need to access at any time. It earns interest — usually calculated on the daily closing balance and credited monthly or quarterly — and there is no lock-in period. You can withdraw, transfer, or use a debit card at any time. The Reserve Bank of India (RBI) mandates that banks offer savings accounts, and interest rates are set by individual banks (not regulated by RBI since 2011).

Fixed deposit (FD)

A fixed deposit is an agreement where you deposit a lump sum with a bank for a fixed tenure — anywhere from 7 days to 10 years — at a pre-agreed interest rate. The interest rate is locked in at the time of opening and does not change during the tenure, regardless of what the market does. Premature withdrawal is allowed but typically attracts a penalty of 0.5–1% on the applicable interest rate. All bank FDs (and savings accounts) are insured up to ₹5 lakh per depositor per bank by the Deposit Insurance and Credit Guarantee Corporation (DICGC).

Savings Account vs FD: Side-by-Side Comparison

Here is a structured comparison of the two instruments across the factors that matter most to Indian depositors:

| Feature | Details |

| Interest rate — Savings account | Public sector banks (SBI, PNB): 2.7–3%Private banks (HDFC, ICICI, Axis): 3–3.5%Small finance banks (AU, Jana, Ujjivan): 5–8%+Rate can change anytime — not locked in. |

| Interest rate — Fixed deposit | Public sector banks: 6–7.5% (1–3 yr tenure)Private banks: 6.5–8% (varies by tenure)Small finance banks: 7–9%+Rate locked for full tenure on opening. |

| Liquidity | Savings account: Fully liquid. Withdraw anytime via ATM, NEFT, UPI, or branch.FD: Low liquidity. Premature withdrawal allowed but attracts 0.5–1% penalty on interest. |

| Minimum deposit | Savings account: ₹0 (zero-balance accounts available) to ₹10,000 (varies by bank).FD: Usually ₹1,000 minimum. No upper limit. |

| Tenure / lock-in | Savings account: No lock-in. Indefinite.FD: 7 days to 10 years. You choose at the time of opening. |

| Interest calculation | Savings account: Daily balance basis, credited monthly or quarterly.FD: Quarterly compounding (standard). Simple interest also available. |

| Tax on interest | Savings account: Interest up to ₹10,000/year exempt under Section 80TTA (old regime only). Senior citizens: up to ₹1 lakh under 80TTB (raised from ₹50,000 in Budget 2026, old regime only). Above that, taxed as per your income slab.FD: TDS of 10% if interest > ₹40,000/year (₹1 lakh for seniors — raised in Budget 2026). No 80TTA exemption. Taxed as per income slab. |

| DICGC insurance | Both savings accounts and FDs insured up to ₹5 lakh per depositor per bank. If you have both, the ₹5 lakh limit covers the combined total at that bank. |

| Suitable for | Savings account: Emergency fund, monthly expense buffer, short-term fund parking.FD: Surplus funds not needed for 3 months to 5 years, capital preservation, guaranteed returns. |

Interest Rates in India: What Are Banks Offering? (May 2026)

Interest rates vary significantly between bank types. The following are indicative figures as of May 2026 — always verify with the bank directly before opening an account. These are examples for illustration and do not constitute a recommendation of any specific bank. The RBI publishes a bank-wise FD rate comparison on its website that is a useful reference.

Savings account interest rates (indicative, May 2026)

| Bank Type | Example Banks | Indicative Rate |

| Public sector banks | SBI, Bank of Baroda, PNB | 2.7–3% |

| Large private banks | HDFC Bank, ICICI Bank, Axis Bank | 3–3.5% |

| Small finance banks | AU SFB, Jana SFB, Ujjivan SFB | 5–6.75% (AU SFB revised to 6.75%, April 2026) |

| Payments banks | Airtel Payments Bank, India Post Payments Bank | 2–4% |

FD interest rates — 1-year tenure (indicative, May 2026)

| Bank Type | Example Banks | Indicative Rate (General / Senior) |

| Public sector banks | SBI, Bank of Baroda, Canara Bank | 6.25–6.45% / 6.75–6.95% (senior) |

| Large private banks | HDFC Bank, ICICI Bank, Axis Bank | 6.25–6.60% / 6.75–7.10% (senior) |

| Small finance banks | AU SFB, Jana SFB, Suryoday SFB | 7.0–8.30% / up to 8.80% (senior) |

| Important note on interest rates FD rates are influenced by the RBI repo rate, currently at 5.25% (held at April 2026 MPC after cuts from 6.5% in 2024-25). With rates on hold, FD rates have stabilised. RBI repo rate is currently 5.25% (held unchanged at April 2026 MPC). It was cut from 6.5% in 2024–25, FD rates may fall. If you are considering a long-tenure FD (3–5 years), locking in now during a rate cut cycle can be advantageous — but again, this is information for you to weigh, not a recommendation. |

How Interest Is Taxed: Savings Account vs FD

Tax treatment is one of the most misunderstood aspects of the savings account vs FD comparison. Here is how the Income Tax Act treats interest from each:

Savings account — Section 80TTA / 80TTB

Interest earned on a savings account is added to your total income and taxed at your applicable slab rate. However:

- Under Section 80TTA, individuals and HUFs (below 60 years) can claim a deduction of up to ₹10,000 per year on savings account interest.

- Under Section 80TTB, senior citizens (60+) can claim up to ₹1 lakh per year on savings account AND FD interest combined — raised from ₹50,000 in Budget 2026. Available under old tax regime only.

- No TDS (tax deducted at source) is deducted on savings account interest by the bank.

Fixed deposit — TDS applies

FD interest does not get the 80TTA benefit (for non-senior citizens). Instead:

- TDS of 10% is deducted if total FD interest exceeds ₹40,000 in a financial year. For senior citizens, the TDS threshold is now ₹1 lakh (raised from ₹50,000 in Budget 2026).

- If your total income is below the taxable limit, you can submit Form 15G (or Form 15H for seniors) to avoid TDS.

- TDS is deducted annually even on cumulative FDs — so tax liability accrues each year, not just at maturity.

- All FD interest is ultimately taxed as per your income slab, regardless of TDS.

| Tax example — 30% slab individual, ₹5 lakh in FD at 7% for 1 year FD interest earned: ₹35,000 Since ₹35,000 < ₹40,000, no TDS deducted by bank Tax liability at 30% slab: ₹10,500 Net interest after tax: ₹24,500 (effective yield: ~4.9%) Compare: ₹5 lakh in AU SFB savings account at 7%, 80TTA exemption up to ₹10,000: Interest earned: ₹35,000 Taxable after 80 TTA deduction: ₹25,000 Tax at 30% slab: ₹7,500 Net interest after tax: ₹27,500 (effective yield: ~5.5%) In this scenario, the savings account gives a better post-tax yield — illustrating whythe ‘FD always gives higher returns’ assumption is not always accurate. |

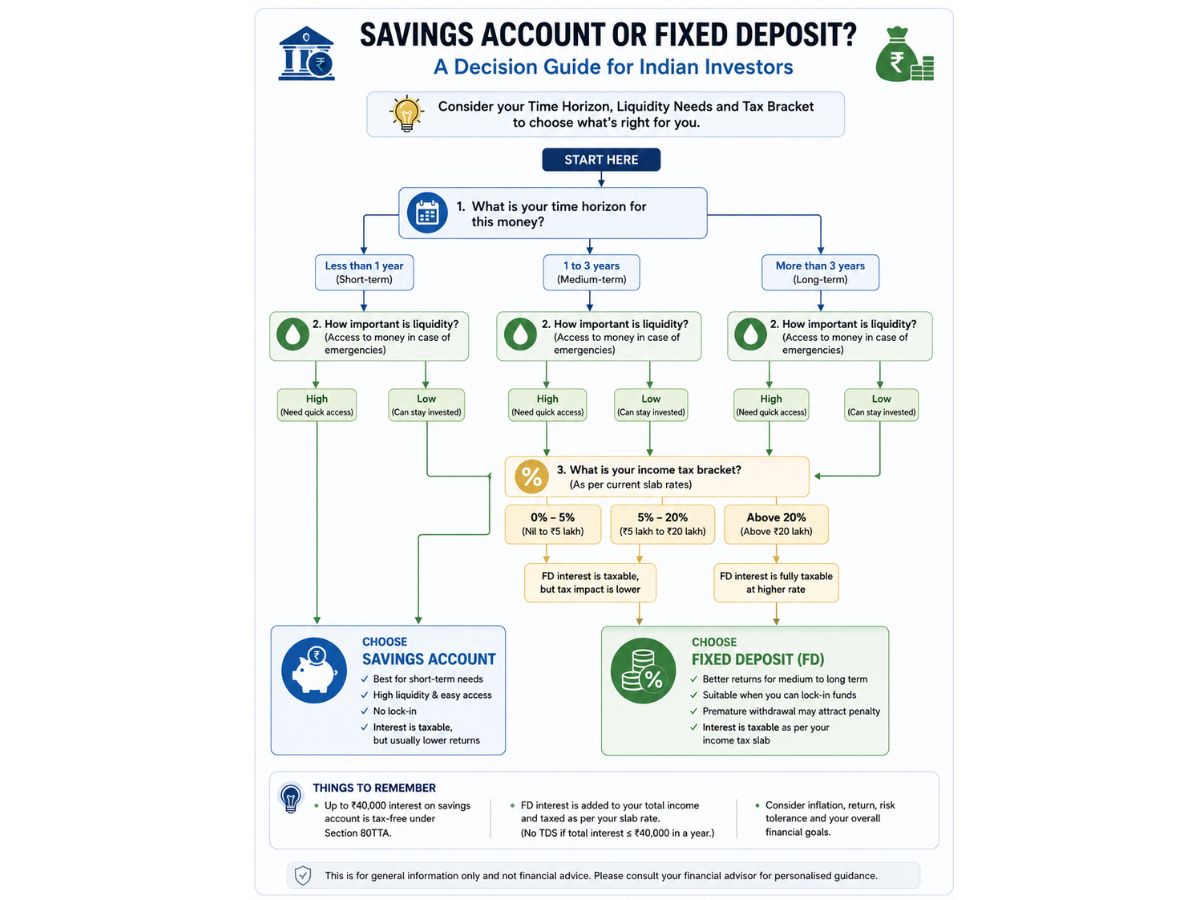

Savings Account or FD: Which Suits Your Situation?

The right choice depends on three factors: how soon you might need the money, what return you want, and your tax situation. Here is a practical decision guide:

| Situation | Consider | Why |

| Emergency fund (3–6 months of expenses) | Savings account | Needs to be instantly accessible — an FD with a penalty is not ideal |

| Monthly salary buffer / expense account | Savings account | You will need this money regularly — no sense in locking it |

| Short-term surplus (under 3 months) | Savings account or liquid MF | FD tenures start at 7 days but short-term rates are low; liquid funds may be more flexible |

| Money not needed for 1–5 years | FD (or RD for monthly savings) | Locked-in higher rates suit money with no immediate purpose |

| Saving for a specific future goal (child’s fees, down payment) | FD with matching tenure | Guaranteed return, known maturity date aligns with the goal |

| Regular monthly savings habit | Recurring Deposit (RD) | Same FD-like rates but you invest monthly — similar to a SIP for savings |

| Senior citizen income supplementation | FD (higher rates + 80TTB) | Senior citizens get higher rates and up to ₹1 lakh tax exemption on interest (Budget 2026, old regime) |

| High tax bracket (30%), smaller amounts | Savings account | 80TTA benefit makes post-tax yield competitive against FD for smaller amounts |

The Sweep-in FD: Getting the Best of Both

If the liquidity vs returns trade-off is your main concern, a sweep-in FD (also called an auto-sweep or flexi-deposit) is worth understanding. Here is how it works:

- You set a threshold — say ₹25,000 — in your savings account.

- Any balance above that threshold is automatically “swept” into an FD, earning FD-level interest.

- When you need money and your savings balance falls below the threshold, the FD is broken in chunks (smallest first) to replenish your account — automatically, without you doing anything.

- Interest earned on the swept portion is at FD rates; the savings account portion earns savings rates.

| Example banks offering sweep-in FDs in India SBI: Multi-Option Deposit (MOD) — minimum ₹10,000 sweep amount HDFC Bank: Sweep In Account — threshold set by account holder Axis Bank: Prime Savings Account with auto-sweep Kotak Mahindra Bank: ActivMoney — auto-sweeps in ₹1 multiples [These are examples for illustration. Check current terms, minimums, and rates directly with the bank.] |

What About Recurring Deposits (RDs)?

If FDs suit people who have a lump sum, Recurring Deposits (RDs) are the FD equivalent for people who want to save a fixed amount every month. RDs offer the same interest rates as FDs for the same tenure, but you deposit monthly — making them useful for building a corpus steadily. If you are comparing savings account vs FD because you want to save regularly, an RD may actually be more relevant to your situation.

When Neither a Savings Account Nor an FD Is Enough

Both savings accounts and FDs are savings instruments — they are designed to preserve your money and earn a modest guaranteed return. They are not designed to grow your wealth significantly over time, especially after accounting for inflation and tax.

| Inflation context India’s average CPI inflation has hovered around 4–6% in recent years. An FD at 7% pre-tax in the 30% slab gives a post-tax return of ~4.9%. If inflation is 5%, your real return is close to zero — your purchasing power is barely maintained. This is not an argument against FDs — they serve a specific purpose well. But for long-termwealth creation, other instruments are worth understanding alongside these. |

For long-term goals (retirement, children’s education, 10+ year horizons), options like SIPs in mutual funds, index funds, or NPS are worth exploring for their potential to outpace inflation over time — though they carry different risk profiles. This article covers only savings accounts and FDs; for investing, see our separate guides.

Frequently Asked Questions

Is a savings account or FD better for an emergency fund?

A savings account is generally more suitable for an emergency fund because it can be accessed instantly at any time without penalty. An FD with a lock-in and a premature withdrawal penalty is not ideal for money you may need urgently. See our detailed guide: Emergency Fund: How Much Is Enough?

Can I have both a savings account and an FD at the same bank?

Yes — and many people do. The ₹5 lakh DICGC insurance limit covers the combined total of all deposits (savings + FD) at a single bank per depositor. If you have more than ₹5 lakh to keep safe, consider spreading across multiple banks.

Which gives better returns — savings account or FD?

In most cases, FDs offer a higher nominal interest rate. However, after accounting for tax (especially in higher income brackets), the savings account’s 80TTA exemption (up to ₹10,000) can make it competitive for smaller amounts. The tax example in Section 4 above illustrates this. Rates also vary widely by bank type — a small finance bank savings account at 7–8% can sometimes match or exceed a public sector bank FD.

Is FD interest taxable every year or only at maturity?

FD interest is taxable on an accrual basis — meaning every year as it accrues, not just when the FD matures. For a 3-year cumulative FD, you owe tax in each of the three financial years even though you receive the full amount only at the end. TDS is also deducted annually if interest crosses the ₹40,000 threshold. Submit Form 15G/15H to avoid TDS if your income is below the taxable limit.

What is the safest bank to open an FD with in India?

All scheduled commercial banks are regulated by the RBI and deposits up to ₹5 lakh per bank are insured by DICGC. This is informational context — NiveshKarlo does not assess or rate the safety of individual banks. For amounts above ₹5 lakh, spreading across multiple banks is one approach people take.

Should I break my FD to invest in mutual funds?

This is a personal financial decision that depends on your goal, timeline, risk tolerance, and tax situation — and one that NiveshKarlo cannot make for you. What we can say is that breaking an FD early costs you 0.5–1% of your interest rate as a penalty. If you are curious about mutual funds or index funds, read our guides to understand how they work before drawing any conclusions.

Are small finance bank FDs safe?

Small finance banks in India are licensed and regulated by the RBI, and their deposits are covered by DICGC insurance up to ₹5 lakh — the same coverage as any other scheduled commercial bank. They offer higher interest rates partly because they cater to underserved segments and need to attract deposits. This is factual context; please evaluate your own comfort level before opening any account.

| Key Takeaways 1. Savings accounts are for liquidity — money you might need anytime. 2. FDs are for money you can lock away for a known period in exchange for a higher guaranteed rate. 3. FD rates are higher in nominal terms, but post-tax returns can be closer than they appear — especially for those in the 30% slab with smaller amounts. 4. Both are insured up to ₹5 lakh per depositor per bank by DICGC. 5. Sweep-in FDs offer a middle ground — FD-level interest with savings account-like accessibility. 6. For regular monthly savings, a Recurring Deposit (RD) may suit better than a lump-sum FD. 7. Neither instrument is designed for long-term wealth creation — for that, other avenues exist. |

What to Read Next on NiveshKarlo

Continue building your personal finance knowledge:

- Emergency Fund: How Much Is Enough? — Where a savings account fits into your safety net

- What Is a Recurring Deposit Account? — The monthly savings alternative to lump-sum FDs

- National Pension Scheme (NPS): Build Your Retirement Fund — Long-term savings beyond bank deposits

- What Is SIP in Mutual Funds and How Does It Work? — For wealth creation beyond savings instruments

- What Are Index Funds? — A low-cost way to understand market-linked investing

- Stocks vs Mutual Funds — Understanding your options beyond bank products

Sources & External References

- Reserve Bank of India (RBI) — Bank savings account and FD rate data, regulatory guidelines

- DICGC (Deposit Insurance and Credit Guarantee Corporation) — ₹5 lakh deposit insurance coverage details

- Income Tax India (Section 80TTA / 80TTB / TDS on FDs) — Tax rules on savings account and FD interest

- SEBI — Regulation of investment products (mutual funds, liquid funds referenced)

- AMFI India — Liquid fund category data (referenced as an alternative to FD)

Disclaimer: This article is for educational and informational purposes only. It does not constitute financial advice, investment advice, or a recommendation to open any bank account, fixed deposit, or any other financial product. All bank names, interest rates, and product examples are illustrative only — NiveshKarlo does not endorse or recommend any specific bank, institution, or financial product. Interest rates are indicative as of May 2026 and are subject to change — verify current rates with your bank before making any decision. Please consult a qualified financial advisor for advice specific to your situation.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.