How to Fill a Cheque for Self: Step-by-Step Guide

Four fields to fill, one signature, and a few rules that matter more than ever after RBI’s 2025-26 cheque clearing updates.

Transparency: AI-assisted rewrite reviewed by the NiveshKarlo team. All RBI cheque clearing rules verified from the RBI circular CO.DPSS.RLPD.No.S536/04-07-001/2025-2026 dated August 13, 2025, and RBI’s January 2026 FAQ update. Informational only.

Most people go their entire adult life writing only two or three self cheques — for a KYC submission, a provident fund withdrawal, or a one-off bank transaction where digital payment is not accepted. Because cheques come up so rarely, filling one correctly when it matters feels more complicated than it actually is.

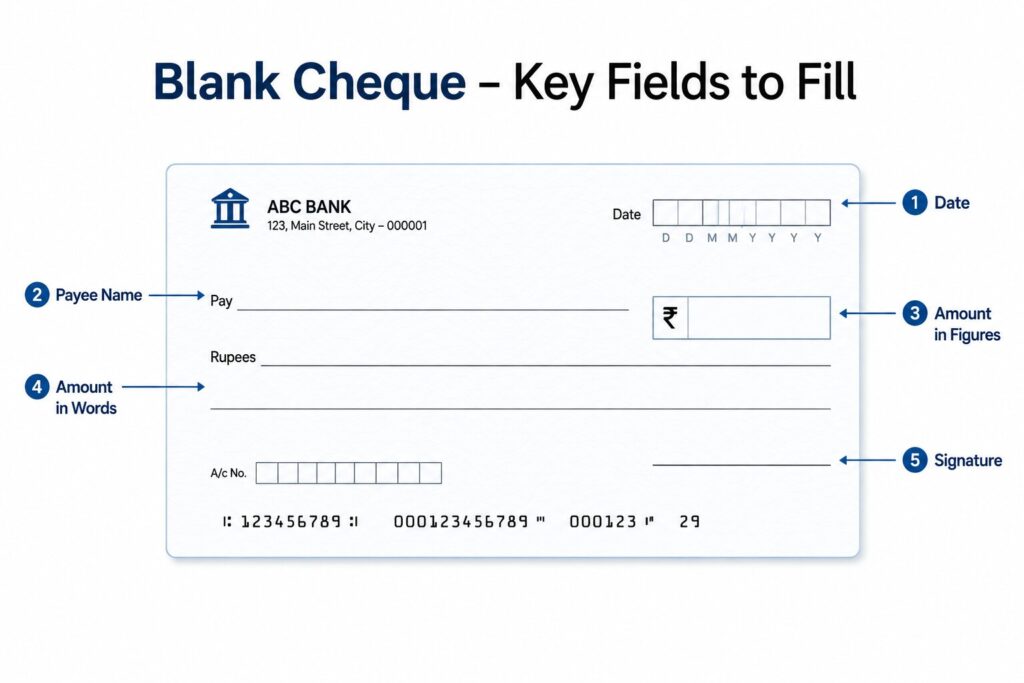

A self cheque is a cheque you write payable to yourself — used primarily to withdraw cash from your own account at a bank branch. It has four fields to fill: the date, the payee name, the amount (in figures and words), and your signature. That is the core of it. What has changed recently is the RBI’s updated cheque clearing rules from 2025-26 — including a strict no-alteration policy and a new same-day clearing system — which make getting the details right even more important the first time.

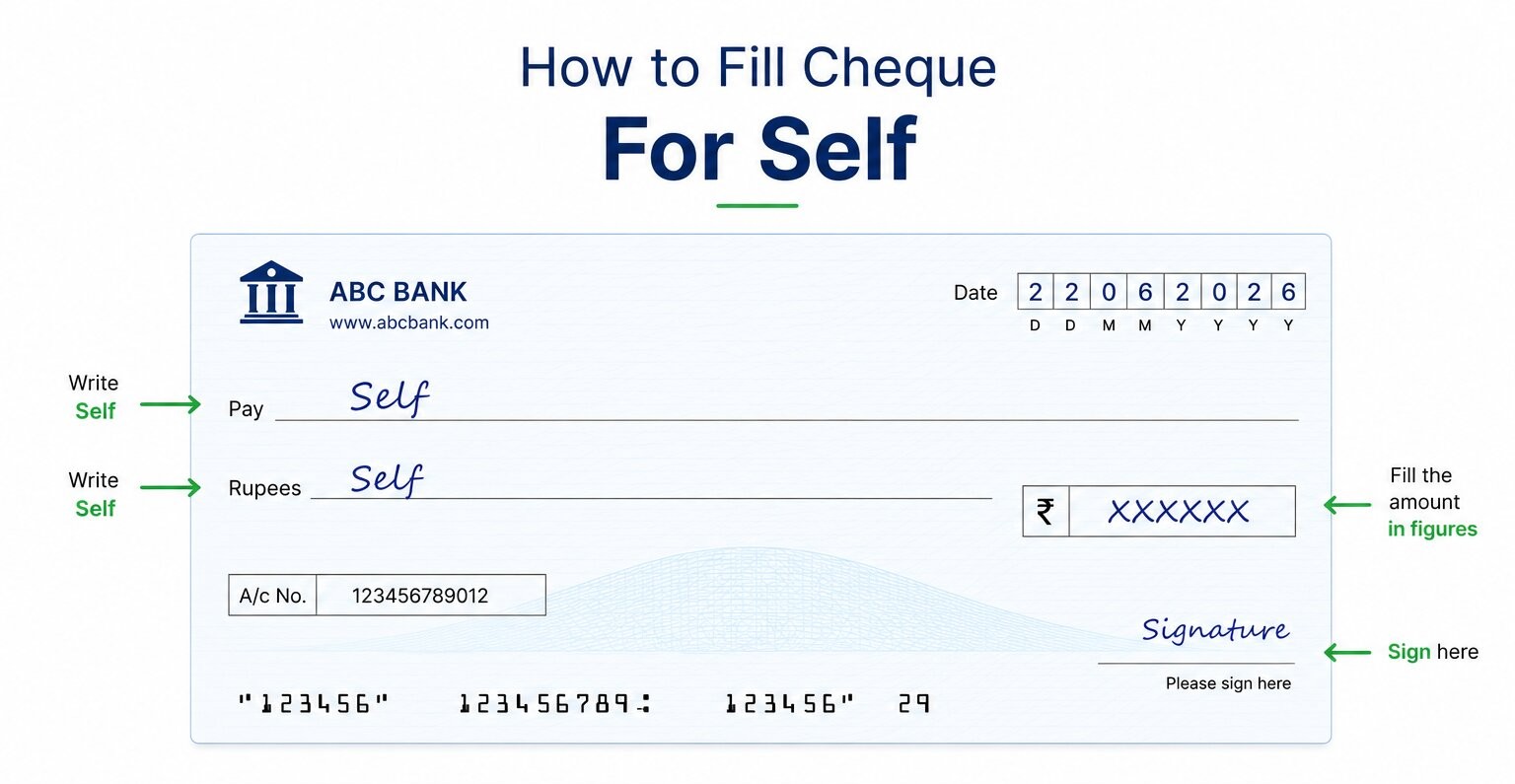

How to fill a self cheque — the four fields

Go through these in order. Each field builds on the one before it, and a mistake in any one of them is grounds for the cheque being returned.

1. Date

Write today’s date in the format DD/MM/YYYY — for example, 22/06/2026. Use the actual date you are writing the cheque, not a future date (post-dated cheques can be valid but are a different use case from self-withdrawal).

A cheque is valid for 90 days from the date written on it. After 90 days, it becomes stale and the bank will not process it. If you write a cheque and do not use it for three months, you will need to issue a fresh one.

2. Payee name

In the “Pay” line, write the word SELF in capital letters. This tells the bank that you — the account holder — are the person presenting the cheque for withdrawal. Do not leave this line blank and do not write your own name here unless your bank specifically requires it. Most banks accept “SELF” as the payee for self-withdrawal purposes.

Draw a line through any blank space remaining after writing SELF — this prevents anyone from adding another name to the cheque after you have written it.

3. Amount — figures and words

Fill in the amount twice: once in the box on the right side of the cheque (in numbers), and once on the line provided for the amount in words.

- In figures: Write the amount without leaving gaps — for example, ₹5000/- rather than ₹ 5 0 0 0. The forward slash and dash at the end (/-) after the amount is a standard practice that prevents anyone from adding extra digits after the number.

- In words: Write the full amount in words followed by the word “Only” — for example, “Five Thousand Rupees Only”. Draw a line through any blank space remaining on that line after writing the amount.

| Important: Both amounts must match exactly. If the amount in figures and the amount in words do not match, the bank will return the cheque unpaid. There is no provision to correct this under the current CTS system — you will need to issue a fresh cheque. Under RBI’s Cheque Truncation System (CTS), no alterations or overwriting are accepted. This applies to the amount fields as well. |

4. Signature

Sign in the bottom right box — the designated signature area on your cheque. Use the same signature that is registered with your bank. Banks verify cheque signatures against the specimen signature on record, and a mismatch — even a minor variation — is grounds for returning the cheque.

Some banks also ask you to write your contact number on the reverse side of the cheque, so that the branch can reach you if a query arises. Check with your branch whether this is required.

What changed in 2025-26 that affects how you fill cheques

RBI’s circular dated August 13, 2025 introduced two significant changes to cheque clearing that every account holder should know before writing a cheque:

1. Cheques now clear the same day — not in 2-3 days

Under the old Cheque Truncation System (CTS), a cheque deposited on Monday morning might be credited only by Wednesday. From October 4, 2025, RBI implemented Continuous Clearing — cheques are now scanned and submitted to the clearing house continuously between 10:00 AM and 4:00 PM on working days.

From January 3, 2026 (Phase 2), the drawee bank has a 3-hour window to confirm or reject each cheque after it is presented. If no action is taken within that window, the cheque is automatically approved and included in settlement. In practical terms: a cheque deposited before 1:00 PM is typically cleared the same day.

| What this means for you when filling a self cheque: Because clearance is now same-day, there is less time for the bank to contact you if something is wrong with the cheque. Getting the date, amount, and signature correct the first time matters more than it did under the old 2-day system. Any error that would have taken a day to flag now returns the cheque within hours. |

2. No alterations — not a single correction

Under CTS, RBI explicitly states that cheques with alterations or modifications are not accepted. If you need to change the payee’s name, the amount in figures, or the amount in words — even by a single digit — you must use a fresh cheque leaf. The only exception is the date field, which can be corrected with the account holder’s initials under some bank policies — but even this varies by bank and it is safer to use a fresh cheque.

This is a significant change from how many people learned to fill cheques years ago, when a correction initialled by the account holder was often accepted. That practice is no longer valid under the current CTS framework.

3. Use permanent, image-friendly ink

Because cheques are now processed as digital images rather than physical instruments, RBI’s updated guidance specifies that account holders should use image-friendly coloured ink — blue or black — and permanent ink to prevent fraudulent alteration of contents. Gel pens with permanent ink are preferable over ballpoint pens that may smear. Avoid pencil or erasable ink under any circumstances.

The Positive Pay System — required for high-value cheques

The Positive Pay System (PPS) is an additional security layer introduced by RBI and implemented through NPCI. It requires account holders to pre-register the details of a cheque — payee name, date, and amount — through their bank’s app, net banking, or branch before the cheque is presented for clearing.

When the cheque reaches the clearing house, the details are matched against the pre-registered information. If they match, the cheque is processed. If they do not, the bank flags it for review.

| Cheque amount | Positive Pay requirement |

| Below ₹50,000 | Optional at most banks — but available if you want to use it |

| ₹50,000 and above | Mandatory at most banks — register details before presenting the cheque |

| ₹5 lakh and above | Mandatory — some banks require branch registration, not just app-based |

For a self cheque used to withdraw cash at your own branch, Positive Pay is typically not required for smaller amounts. But if you are issuing a cheque of ₹50,000 or more to someone else, confirm with your bank whether Positive Pay registration is needed before the cheque is presented.

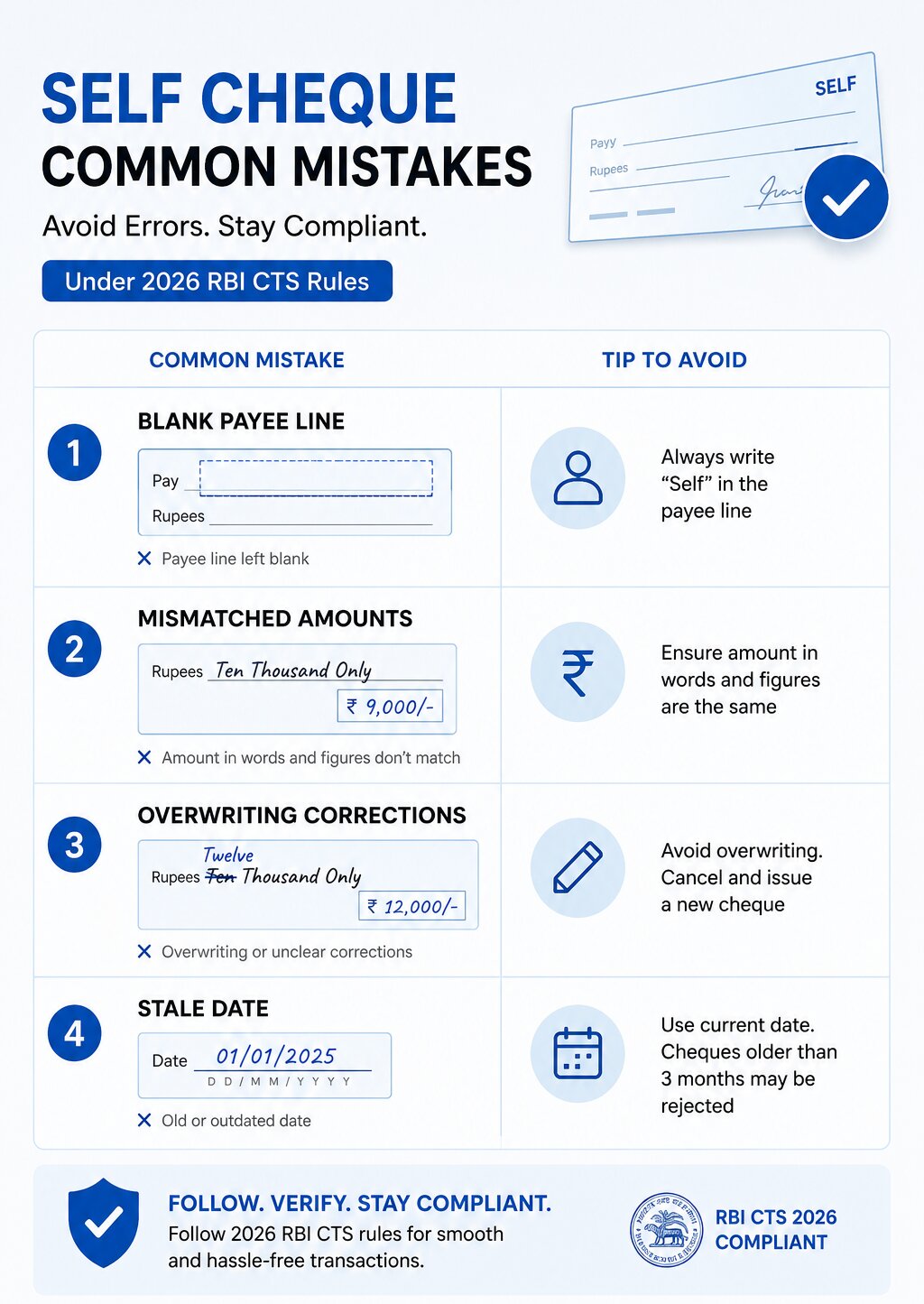

Mistakes that get cheques returned — and how to avoid them

| Mistake | What happens / how to avoid it |

| Date left blank or wrong | Cheque is returned as invalid. Always write the current date in DD/MM/YYYY format. Validity is 90 days from this date. |

| Payee line left blank | A blank payee makes the cheque a bearer instrument — anyone who holds it can cash it. Always write SELF for self-withdrawal. |

| Amount in figures and words do not match | Cheque returned immediately. Double-check both before signing. |

| Any overwriting or correction on the cheque | Not accepted under CTS. Issue a fresh cheque leaf for any correction, including the amount. |

| Signature mismatch | Cheque returned. Use exactly the same signature on file with your bank. |

| Using erasable or pencil ink | Facilitates fraud. Use permanent blue or black ink only. |

| Not registering Positive Pay for high-value cheques | Cheque may be held for manual review or returned. Register via your bank’s app or net banking before presenting. |

| Presenting a stale cheque (older than 90 days) | Cheque returned. Issue a new cheque with today’s date. |

Also Read: How to cancel a cheque – What is it and How to use it? | India Post Payment Bank Account Opening Online

Frequently asked questions

What do I write in the payee field for a self cheque?

Write the word SELF in capital letters. This is the standard way to indicate that you — the account holder — are withdrawing the money yourself. After writing SELF, draw a line through any blank space remaining on that line to prevent additions.

How long is a cheque valid?

A cheque is valid for 90 days (3 months) from the date written on it. After that, it becomes stale and the bank will return it unpaid. If your cheque has expired, issue a fresh cheque with today’s date.

Can I correct a mistake on a cheque?

Under the current RBI Cheque Truncation System (CTS), alterations and corrections are not accepted — except for the date field at some banks, with the account holder’s initials. For any correction to the payee name or amount, you must use a fresh cheque leaf. Do not strike through and rewrite — the corrected cheque will be returned.

How quickly does a self cheque clear now?

Since January 3, 2026, RBI’s Phase 2 Continuous Clearing gives banks a 3-hour window to confirm or reject a cheque after it is presented. If you present a self cheque at your bank branch before 1:00 PM, the amount is typically credited the same day. This is a significant improvement from the earlier 2-3 day clearance cycle. For full details, see RBI’s FAQ on Cheque Clearing.

What is Positive Pay and do I need it for a self cheque?

Positive Pay is a system where you pre-register the details of a cheque (payee, date, amount) through your bank’s app or net banking before it is presented. Most banks require it for cheques above ₹50,000. For a self cheque used for cash withdrawal at your own branch, Positive Pay is generally not required for smaller amounts — but confirm with your bank, as the threshold varies.

What ink colour should I use to fill a cheque?

Use blue or black permanent ink — gel pens with permanent ink are preferred. RBI guidance updated in January 2026 specifies that cheques should be filled with image-friendly coloured ink, since they are scanned and processed as digital images under CTS. Avoid pencil, erasable ink, or any ink that may smear or fade.

Can someone else cash my self cheque?

A self cheque is intended for the account holder’s own use. However, if it falls into someone else’s hands, they may be able to present it at the issuing bank’s branch — which is why a blank payee line is a security risk. Always write SELF in the payee field and draw a line through any remaining blank space. If you lose a signed blank cheque, contact your bank immediately to stop payment on it.

Before you fill the next one

A self cheque has not changed in its essentials — four fields, one signature. What has changed under RBI’s 2025-26 updates is the zero-tolerance policy on corrections and the speed at which cheques are now cleared. Writing it right the first time, in permanent ink, with matching amounts and a consistent signature, is all that is needed. If a mistake happens, use a fresh leaf — the old habit of crossing out and initialling is no longer accepted.

If you are looking at the broader picture of managing your bank account — what type of account suits different goals, or how savings account interest compares to other options — see our guide on savings account vs fixed deposit and the difference between savings and current accounts.

Disclaimer: This article is for educational and informational purposes only. All RBI cheque clearing rules and Positive Pay thresholds referenced are based on RBI’s circular CO.DPSS.RLPD.No.S536/04-07-001/2025-2026 dated August 13, 2025, and the RBI FAQ on Cheque Clearing updated January 2026. Bank-specific policies on Positive Pay thresholds and date correction procedures may vary — always confirm with your bank before presenting a cheque. NiveshKarlo does not endorse any specific bank or banking product.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.