The Power of Compounding: Why Your 30s Are Not Too Late

Most people spend their 20s ignoring compounding and their 40s regretting it. This article is for the person in between — the one who still has time, but needs to see the numbers to believe it.

Transparency note: This article was drafted with AI assistance and reviewed by the NiveshKarlo team. All interest rates and return figures were live-verified on May 23, 2026. This is for informational purposes only — not financial advice.

Here is a question a lot of people in their 30s quietly carry around: is it too late?

They have watched the last decade go by without a PPF account, without a single SIP, maybe with a savings account they barely look at. They know compounding is supposed to be magical. They also know that every article about it uses a 25-year-old as the hero. And they wonder if they missed the bus.

The short answer is no. The longer answer — the one with actual rupee amounts and real Indian instruments — is what this article is about.

What compounding actually is — without the textbook definition

Every explanation of compound interest starts with a formula. We will get to numbers shortly, but first, here is the idea in plain language.

When you keep money in a fixed deposit, the bank pays you interest. Simple enough. Now, if that interest gets added to your balance and the bank then pays you interest on that larger balance next time — that is compounding. Your interest is earning interest. And then that interest earns interest on top. It keeps folding back on itself.

The reason this matters so much over time is that the fold gets bigger every year. In year one, the extra interest is small. In year ten, it is significant. In year twenty-five, it is the dominant force — the original money you put in might be a fraction of what your account holds.

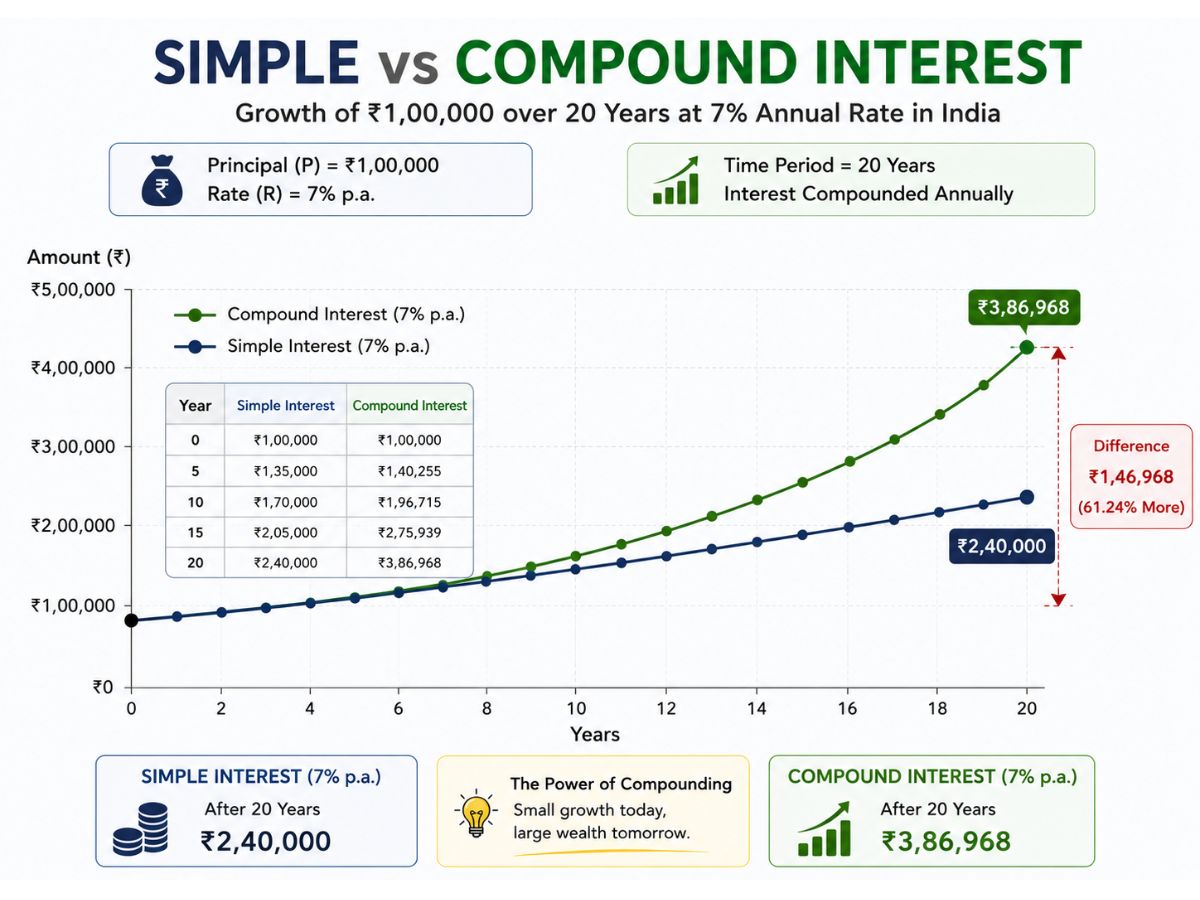

Here is a concrete example to make this real. Two people invest ₹1,00,000. One earns simple interest at 7% per year. The other earns compound interest at the same 7%, compounded annually. After 20 years:

| Simple Interest at 7% | Compound Interest at 7% | |

| After 5 years | ₹1,35,000 | ₹1,40,255 |

| After 10 years | ₹1,70,000 | ₹1,96,715 |

| After 15 years | ₹2,05,000 | ₹2,75,903 |

| After 20 years | ₹2,40,000 | ₹3,86,968 |

Same rate. Same starting amount. But compounding delivers ₹1,46,968 more after 20 years — without any extra effort from you. That extra amount is entirely from interest earning interest.

The PPF (Public Provident Fund) is one of the cleanest examples of this in India. It currently earns 7.1% per annum, compounded annually, and the entire return is tax-free. Over a 15-year lock-in at 7.1%, ₹1,00,000 grows to roughly ₹2,81,400 — without any active management from you. That ₹1,81,400 in growth is compounding doing its work, silently, year after year.

How compounding works across Indian instruments — and why the frequency matters

Not all compounding is the same. The frequency — how often interest is calculated and added back to your balance — changes your final outcome, sometimes significantly.

In India, different instruments compound at different intervals:

- PPF: Compounded annually. Interest is calculated monthly on the lowest balance between the 5th and the last day of the month, but credited to your account at the end of the financial year. One practical implication: deposit before the 5th of each month to count that month’s balance.

- Fixed Deposits: Most Indian bank FDs compound quarterly. SBI, HDFC Bank, ICICI Bank — all use quarterly compounding as standard. This means a 6.40% p.a. FD is slightly better than it sounds because the interest compounds four times a year, not once.

- Recurring Deposits: Also quarterly compounding — same as FDs. If you are building savings month by month rather than investing a lump sum, an RD gives you the compounding benefit of an FD but with monthly deposits.

- Mutual Funds via SIP: Compounding here is continuous — it happens every market day as the NAV of your fund changes. This makes it different from an FD. Each instalment in a SIP starts compounding from the day it is invested. The first month’s investment compounds for the entire duration; the last month’s barely has time to compound at all. This is why long SIP durations matter so much.

To show you what frequency does to the same rate, here is ₹1,00,000 at 7% for 10 years under different compounding schedules:

| Frequency | Where it applies in India | ₹1 lakh after 10 years at 7% |

| Annually | PPF | ₹1,96,715 |

| Quarterly | FDs, RDs at most Indian banks | ₹1,99,372 |

| Monthly | Some savings accounts | ₹2,00,967 |

| Daily | Certain digital products | ₹2,01,373 |

The difference between annual and daily compounding on ₹1 lakh over 10 years is only about ₹4,658. This tells you something important: the frequency of compounding matters far less than the rate and the time. Spending energy chasing a slightly higher compounding frequency is less valuable than simply starting sooner or choosing an instrument with a better rate.

If you are 35 and haven’t started — here is what the next 25 years look like

This is the section for the person who opened this article because they are worried they are too late.

Let us put actual numbers to it — using real Indian instruments with verified May 2026 rates.

Scenario 1: ₹5,000 per month in PPF for 15 years (starting at 35)

PPF has a 15-year lock-in, so if you start at 35, your account matures at 50. You can then extend in 5-year blocks. Annual rate: 7.1%, compounded annually, fully tax-free under the EEE category (contribution, interest, and maturity are all exempt from income tax).

| ₹5,000/month for 15 years = ₹9,00,000 total invested Estimated maturity at 7.1% compounded annually: ₹16,27,000 (approx.) That is ₹7,27,000 in tax-free interest — earned without any market risk. Extend for another 5 years (to age 55) and the corpus grows to approximately ₹23,00,000. [Figures are illustrative; use the official PPF calculator for precision.] |

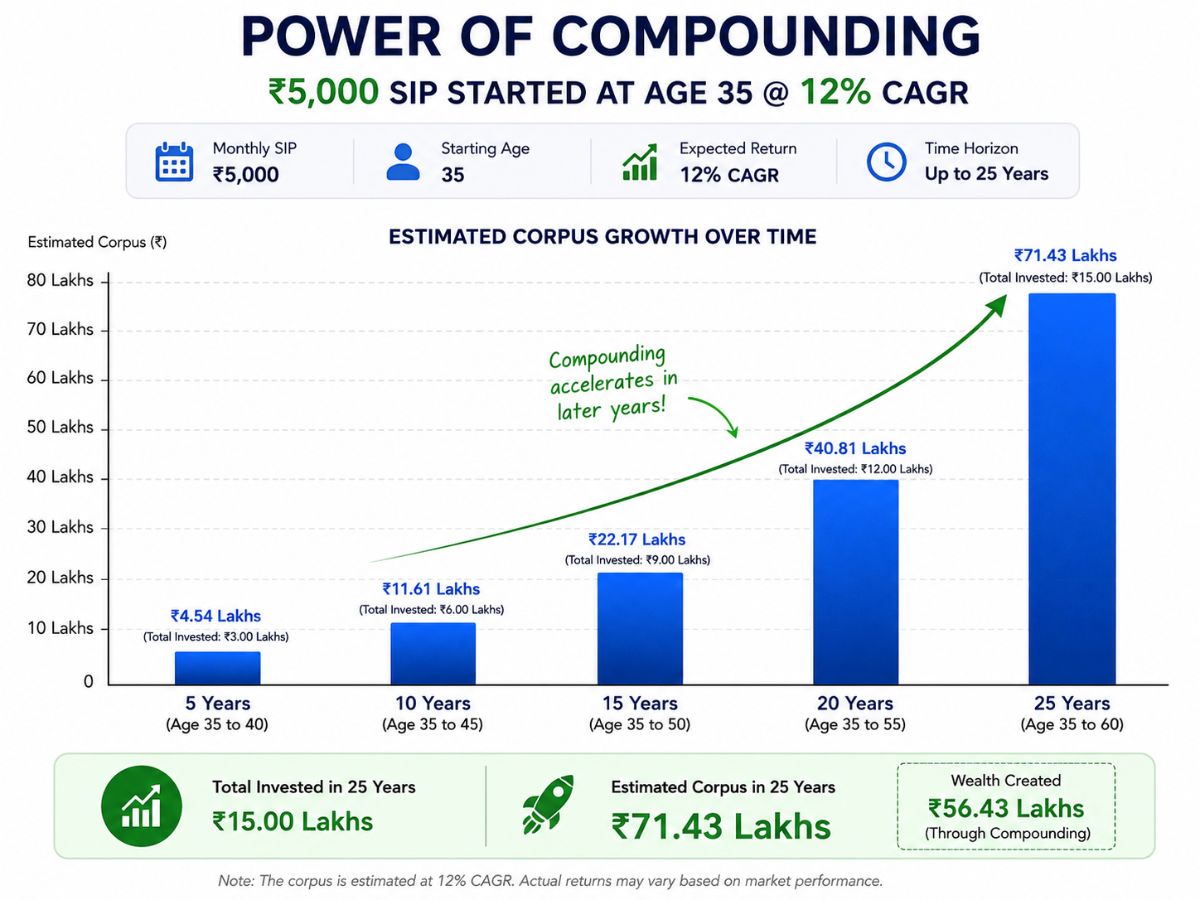

Scenario 2: ₹5,000 per month in an index fund SIP for 25 years (starting at 35)

The Nifty 50 has delivered approximately 12–13% CAGR over the last 10 years (April 2016 to April 2026, NSE Indices data). For this illustration, a conservative 12% is used — past performance is not a guarantee of future returns. Actual returns from index funds will vary, and can be negative in the short term.

| ₹5,000/month SIP for 25 years = ₹15,00,000 total invested Estimated corpus at 12% CAGR (illustrative): ₹94,88,000 (approx.) The compounding gain: ₹79,88,000 — more than 5× the amount invested. Important: equity SIP returns are market-linked and not guaranteed. Short-term value can fall significantly. This projection assumes uninterrupted investing through market ups and downs over 25 years. [Not a recommendation. Verify returns at amfiindia.com before any decision.] |

What if you split the ₹5,000 — some in PPF, some in SIP?

Many people in their 30s do exactly this: put ₹2,500 in PPF for guaranteed, tax-free growth, and ₹2,500 in a Nifty 50 index fund SIP for long-term wealth creation. This is not advice — it is simply one approach people use to balance certainty against growth potential. The compounding in both cases runs simultaneously, which is the real advantage.

The Rule of 72: a 10-second check you will use forever

There is a shortcut that every person who understands compounding uses instinctively. It is called the Rule of 72, and it tells you how many years it takes for your money to double at a given interest rate.

| Years to double = 72 ÷ Annual interest rate PPF at 7.1% → 72 ÷ 7.1 = ~10.1 years to double FD at 6.40% (large bank) → 72 ÷ 6.4 = ~11.2 years to double Nifty 50 index fund (12% historical CAGR) → 72 ÷ 12 = 6 years to double Savings account at 3% → 72 ÷ 3 = 24 years to double This is an approximation, not a precise formula. Use it for quick mental comparisons. |

The practical use of this: when you see an interest rate quoted anywhere — a bank ad, a mutual fund factsheet, a fixed deposit offer — you can immediately translate it into doubling time. A savings account at 3% takes 24 years to double your money. A PPF account at 7.1% takes just over 10. An index fund at 12% historical CAGR takes 6. These are fundamentally different propositions, and the Rule of 72 makes that visible instantly.

For a detailed look at how savings accounts and FDs compare on this dimension, see our piece on Savings Account vs FD which goes through the numbers for current May 2026 rates.

Three things that quietly kill compounding — and how to protect against them

Understanding how compounding works is only useful if your money actually gets to compound uninterrupted. Here are three forces that erode it, specific to the Indian context.

Inflation — the return you don’t see

The RBI projects CPI inflation at 4.6% for FY 2026–27. If your PPF earns 7.1% and inflation runs at 4.6%, your real return — the actual increase in what your money can buy — is roughly 2.5%. This is still positive, which is good. But an FD at 6.25% (large bank, general public, May 2026) yields a pre-tax real return of about 1.65% — and after paying income tax at your slab rate, potentially close to zero or negative in real terms for higher earners.

This does not mean FDs are bad — they have a role. It means compounding in a tax-inefficient, inflation-exposed instrument over long periods can feel more powerful than it actually is in purchasing power terms.

Breaking the chain — withdrawals and paused SIPs

Compounding requires continuity. A two-year pause in a 20-year SIP costs you more than the two years of contributions you missed — it costs you the compounding that would have run on those contributions for the remaining years. Similarly, breaking an FD early does not just cost you a penalty. It resets the compounding clock.

This is one reason building an emergency fund before investing matters. If your savings are tied up in a SIP or an FD and a crisis hits, you are forced to break the compounding chain. A liquid emergency fund protects the chain.

Tax drag — compounding after tax is smaller than it looks

FD interest is added to your income and taxed every year at your applicable slab rate. For someone in the 30% bracket, a 6.40% FD effectively yields about 4.5% after tax. Meanwhile, PPF compounds at the full 7.1% because the interest is exempt from tax under Section 10(11) of the Income Tax Act — a meaningful structural advantage over long durations. Similarly, equity mutual fund SIPs held for more than one year attract long-term capital gains tax at 12.5% on gains above ₹1.25 lakh, rather than your full income slab rate. Understanding which instruments give you better post-tax compounding is as important as understanding the nominal rate. For a deeper look at the tax side of mutual fund returns, the AMFI India investor education section covers this in accessible language.

Why SIP compounding is different — and why that actually helps you

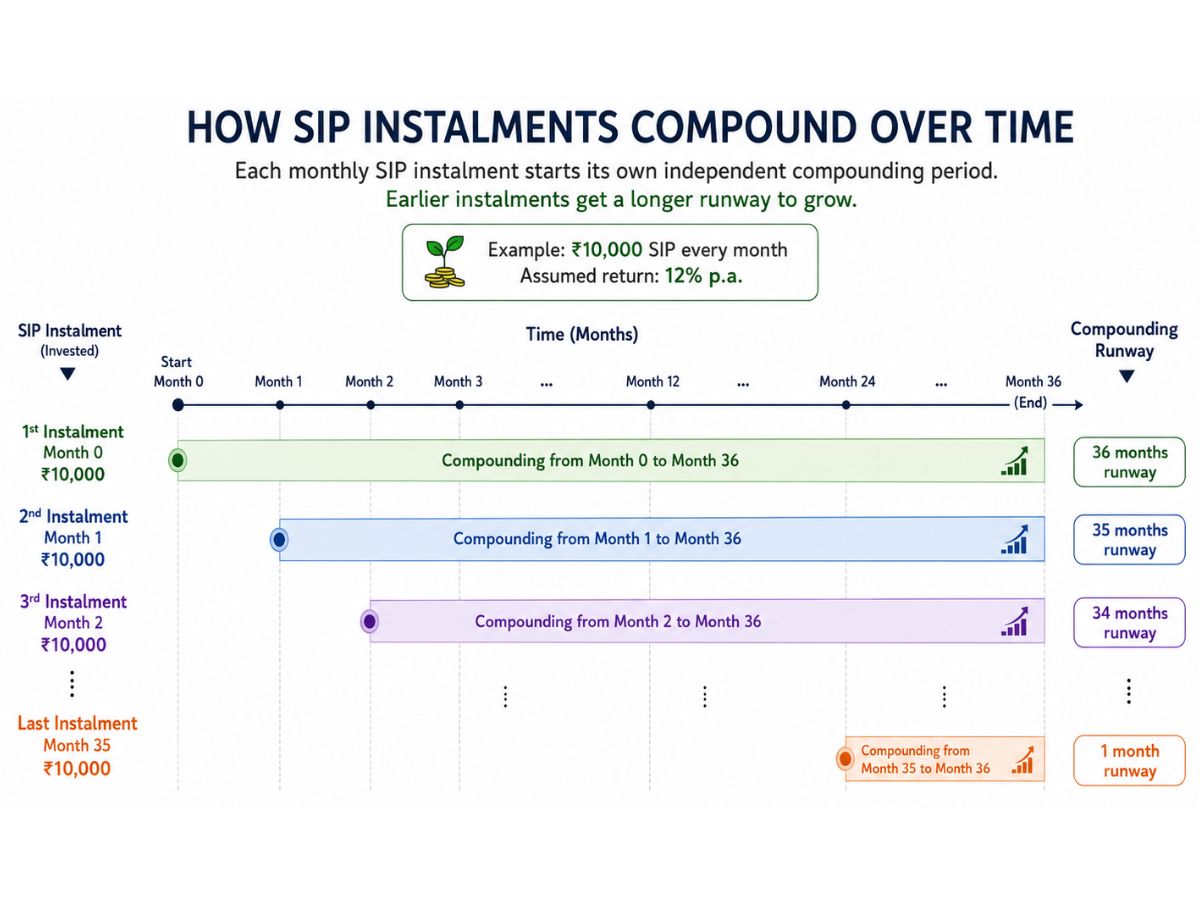

There is a common misconception that a SIP does not benefit from compounding the way a lump sum does. It does — but the mechanics are different, and once you understand them, you will see why the SIP structure actually suits the 35-year-old investor rather well.

When you invest ₹5,000 in month one of a 25-year SIP, that ₹5,000 has all 25 years to compound. The ₹5,000 you invest in month 25 has 24 years and 11 months. The ₹5,000 you invest in the final month has almost no time. Each instalment is its own independent compounding journey, running simultaneously with all the others.

This has a counterintuitive implication: the first few years of contributions are disproportionately valuable — they have the longest runway. But it also means that starting a SIP at 35 still gives your early contributions 25 years of runway, which is substantial. And it means that even an irregular investor — someone who can only invest ₹2,000 some months and ₹8,000 others — still benefits from compounding on whatever they put in.

SIP returns are calculated using XIRR (Extended Internal Rate of Return) rather than simple CAGR, because each instalment has a different start date. If you want to understand the underlying mechanics of the funds you would invest in, our guide to analysing a mutual fund walks through what to look at before you start.

Questions people actually ask about compounding in India

Is PPF compound interest? How does it actually work?

PPF is compound interest — annual compounding at 7.1% for Q1 FY 2026–27. The interest is calculated monthly on the lowest balance between the 5th and last day of the month, but it is credited once at year end (March 31). One practical consequence: if you deposit ₹1.5 lakh on April 6, you lose April’s interest calculation. Deposit by April 5 and you gain a full month’s interest. Over 15 years, timing your annual deposit before the 5th of a month can make a meaningful difference.

Does a savings account give compound interest?

Yes. Savings account interest in India is calculated daily on the closing balance and credited monthly or quarterly depending on the bank. That makes it compound interest — though at rates between 2.7% and 6.75% depending on the bank (small finance banks like AU SFB currently offer up to 6.75% as of April 2026). For a side-by-side of how this compares with FD compounding, our piece on the two instruments covers the current rates in detail.

Why does starting early matter so much more than the amount?

Because compounding is exponential. Each additional year does not add a fixed amount — it multiplies the existing total. This means the gains in year 20 are larger than the cumulative gains of years 1 through 10 combined. A person who starts investing ₹5,000 a month at 25 ends up with more at 60 than someone who starts ₹10,000 a month at 35 — despite investing half as much. The 10 extra compounding years at the start matter more than the doubled investment amount. If you are 35 now, your advantage over someone starting at 45 is just as real.

How do I calculate compound interest for an Indian FD?

The formula is A = P × (1 + r/n)^(n×t) where P is the principal, r is the annual rate as a decimal, n is 4 for quarterly compounding, and t is years. For a ₹2,00,000 FD at 6.40% for 3 years: A = 2,00,000 × (1 + 0.064/4)^(4×3) = 2,00,000 × (1.016)^12 = 2,00,000 × 1.2090 = ₹2,41,800. The ₹41,800 in interest is about 8.7% more than simple interest would give at the same rate.

What is the Rule of 72 and is it accurate for Indian FDs?

The Rule of 72 estimates doubling time by dividing 72 by your interest rate. For a 6.40% FD: 72 ÷ 6.40 = 11.25 years. The actual answer (using the compound interest formula) is approximately 11.2 years — so the rule is accurate enough for practical use. It is slightly less accurate for very high or very low rates, but for the 6–8% range typical of Indian FDs and PPF, it works well.

Can I benefit from compounding even if I invest small amounts?

Yes — and this is one of the most important things to understand about compounding. The mathematics does not require large amounts. ₹1,000 per month compounding at 12% for 20 years grows to approximately ₹9,99,000 — nearly ₹10 lakhs from a total investment of ₹2,40,000. The amount matters less than the time. Starting with a small amount today is almost always better than waiting until you can invest a larger amount.

How this article was put together

We believe in being transparent about how our content is created, especially on financial topics that matter to your real money decisions.

This article was drafted with AI assistance and reviewed by the NiveshKarlo team for accuracy and India-specific context. All interest rates — PPF 7.1% (Q1 FY 2026–27 per India Post), FD rates 6.25–6.45% for large banks (May 2026), Nifty 50 10-year CAGR approximately 12–13% (NSE India, April 2016–April 2026), and RBI CPI inflation projection 4.6% for FY 2026–27 — were live-searched and verified on May 23, 2026, before the article was written. We searched before we wrote, not after.

No financial product is recommended anywhere in this article. All figures — including SIP projections — are illustrative. Past returns are not a guarantee of future performance. If you are making a financial decision based on numbers you read here, please verify them with the relevant institution first and speak to a SEBI-registered financial advisor if you need guidance specific to your situation.

This article will be reviewed when the PPF rate changes, when FD rates shift materially, or when the Nifty 50 long-term CAGR data is updated by NSE Indices.

Sources

The PPF rate and rules referenced throughout this article are from the India Post PPF scheme page.

Nifty 50 historical CAGR data is available at NSE India.

Mutual fund returns and category data can be verified at AMFI India.

RBI monetary policy decisions and inflation projections are published at rbi.org.in.

Tax rules referenced — Section 10(11) PPF exemption, LTCG on equity funds — are available at incometax.gov.in.

Disclaimer: This article is for educational and informational purposes only. It does not constitute financial advice or a recommendation to invest in any instrument. All return projections are illustrative and based on historical data or current indicative rates as of May 2026. Market-linked returns can go up or down — past performance is not a guarantee of future results. All product names mentioned are examples only. NiveshKarlo does not endorse any specific financial product or institution. Please consult a SEBI-registered financial advisor before making investment decisions.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.