Health Insurance Basics: What You Need to Know Before You Buy

Medical costs are rising at 14% a year — faster than almost anything else. This article explains what health insurance covers, which policy terms actually matter, and how much cover is enough in 2026.

Transparency: AI-assisted draft reviewed by the NiveshKarlo team. All figures — medical inflation rate, IRDAI CSR data, GST changes, PED waiting period rules — were live-verified June 29, 2026. Informational only. No specific insurer is recommended. Consult an IRDAI-licensed advisor before buying.

A bypass surgery that cost ₹5 lakh in 2021 costs over ₹8 lakh in 2026. At the current rate of medical inflation — approximately 14% annually — that same procedure will cost close to ₹20 lakh by 2036. This is not a hypothetical. It is arithmetic.

The average company-provided group health policy covers ₹2–5 lakh per employee. For a weekend hospitalisation with a moderate surgery, that may be enough. For a cardiac event, a cancer diagnosis, or a major accident, it almost certainly is not. The health insurance sector covered 58 crore lives in FY 2024-25 and collected ₹1,17,505 crore in premiums — yet significant gaps remain in both coverage amounts and awareness of what policies actually cover.

This article is not a product comparison or a list of the best insurers. It is an explanation of how health insurance works, what the terms in a policy document actually mean, and what decisions matter most when choosing or reviewing a policy.

What health insurance actually covers — and what it does not

A standard health insurance policy — also called a mediclaim policy in India — covers hospitalisation expenses when you are admitted for at least 24 hours. This includes room charges, doctor fees, surgery costs, anaesthesia, medicines during hospitalisation, and diagnostic tests done as part of the treatment.

Most policies also cover:

- Pre-hospitalisation expenses: Medical costs incurred in the 30–60 days before admission — investigations, specialist consultations, and medicines related to the condition that led to hospitalisation.

- Post-hospitalisation expenses: Follow-up costs for 60–90 days after discharge — physiotherapy, medicines, tests. The exact duration varies by policy.

- Day care procedures: Treatments that used to require overnight admission but can now be completed in a few hours — cataract surgery, dialysis, chemotherapy. IRDAI mandates that all standard policies cover at least 400 day care procedures.

- Ambulance charges: Emergency ambulance costs, typically up to a defined limit per claim.

What standard policies typically do not cover — unless you specifically buy add-ons or choose a comprehensive plan:

- Outpatient (OPD) expenses: Doctor consultations, pharmacy bills, diagnostic tests done without hospitalisation. OPD cover is available as an add-on or in premium plans but is not standard in basic policies.

- Dental and vision: Routine dental treatment and eyeglasses are excluded from most standard plans.

- Cosmetic procedures: Any treatment for aesthetic purposes rather than medical necessity.

- Pre-existing conditions during the waiting period: Conditions you had before buying the policy — diabetes, hypertension, thyroid — are covered only after the waiting period ends.

The policy terms that actually determine your out-of-pocket cost

Most people compare health insurance by premium alone. The premium is the least useful number to compare. These are the terms that determine what you actually pay when you make a claim.

Sum insured

The maximum amount the insurer will pay in a policy year. Once you exhaust this amount, all additional costs in that year come from your pocket. Medical inflation at 14% annually means a ₹5 lakh policy bought five years ago is worth ₹2.6 lakh in today’s purchasing power for healthcare. The minimum recommended sum insured in 2026 is ₹10 lakh for an individual in a Tier-2 city and ₹25 lakh or higher in a metro. These are not arbitrary numbers — they reflect the actual cost of a week-long hospitalisation with a moderate procedure at a private hospital in those cities.

Room rent limit

Many policies cap the room rent they will cover — often at 1% of the sum insured per day. On a ₹5 lakh policy, that is ₹5,000 per day. If you are hospitalised in a room that costs ₹8,000 per day, you pay the ₹3,000 difference — and that difference also proportionally reduces what the insurer pays for other items like doctor fees, surgery costs, and diagnostics billed against that room.

A room rent cap can significantly increase your out-of-pocket cost even when your sum insured has not been exhausted. Policies with no room rent capping — which allow you to choose any room category — are meaningfully better, even if their premium is slightly higher.

Co-payment

A co-pay clause requires you to pay a fixed percentage of every claim — typically 10% or 20%. On a ₹3 lakh surgery bill with a 10% co-pay, you pay ₹30,000 regardless of how much of your sum insured remains. Co-pay clauses are common in senior citizen plans and in policies offered in specific geographies. They reduce the premium but increase every claim’s out-of-pocket cost. Zero co-pay is preferable unless the premium difference is substantial.

Pre-existing disease (PED) waiting period

IRDAI reduced the maximum PED waiting period from 4 years to 3 years in 2025. This means conditions you had before buying the policy — diabetes, hypertension, asthma — must now be covered by the insurer within 3 years at most. Some insurers offer shorter waiting periods (1–2 years) at a higher premium. During the waiting period, claims related to the pre-existing condition are rejected — so declaring all existing conditions accurately at the time of purchase is essential.

Restoration benefit

If your sum insured is exhausted during a hospitalisation, a restoration benefit refills it — fully or partially — for subsequent claims in the same policy year. This is particularly relevant for families on a floater policy, where one person’s serious illness can exhaust the entire sum insured before the year ends. Unlimited restoration, which refills the sum insured multiple times in a year, is available in premium plans.

Claim settlement ratio (CSR)

The CSR is the percentage of claims an insurer settled in a financial year, as reported by IRDAI in its annual report. A CSR of 95% means the insurer settled 95 out of every 100 claims received. According to IRDAI FY 2024-25 data, four insurers — Aditya Birla Health, Niva Bupa, Galaxy, and Narayana — achieved 100% CSR. The CSR is a useful signal for how reliably an insurer pays claims, though it does not capture how much of each claim was paid or how smooth the process was.

How much health insurance cover do you actually need?

This depends on three things: where you live, your family size, and your age. Here is a practical framework based on 2026 private hospital costs:

| Situation | Minimum recommended cover | Why |

| Individual, Tier-2 city | ₹10 lakh | A week-long hospitalisation with moderate surgery at a private Tier-2 hospital routinely crosses ₹5–7 lakh |

| Individual, metro city | ₹25 lakh or higher | Same procedure in a metro private hospital costs 40–60% more; ICU stays can cross ₹1 lakh per day |

| Family floater (2 adults + children), Tier-2 | ₹15–20 lakh | Floater sum insured is shared — one hospitalisation should not exhaust cover for the whole family |

| Family floater (2 adults + children), metro | ₹25–50 lakh | Higher base cost plus restoration benefit for multiple claims in a year |

| Senior citizens (60+) | ₹10–15 lakh individual | Higher claim frequency; floater policies for seniors are expensive — individual policies often better value |

These are minimum figures — not targets to cap at. A super top-up policy (which covers bills above a defined deductible, like a ₹5 lakh base policy topped up by a ₹45 lakh super top-up) is a cost-effective way to reach higher coverage levels without paying the premium of a ₹50 lakh base policy.

Your employer’s health cover is not enough — here is why

Employer group health insurance is a benefit, not a substitute for personal health insurance. The gaps are structural, not incidental:

- Coverage ends with employment. If you resign, are laid off, or retire, the group cover ends immediately. There is typically a 30-day grace period during which you can convert to an individual policy — but this often costs significantly more than buying an individual policy when you were younger and healthier.

- Sum insured is usually inadequate. Most employer policies cover ₹2–5 lakh. As the figures above show, this is insufficient for a serious illness in a metro city.

- You have no control over the policy. The employer chooses the insurer, the sum insured, and the terms. If the company switches insurers at renewal, your waiting period with the old insurer does not transfer.

- Portability does not apply to group policies. The portability benefit — which lets you transfer your waiting period credits to a new insurer — applies only to individual and family retail policies, not employer group covers.

The practical recommendation: buy a personal health policy when you are young and healthy, independently of whatever employer cover you have. The younger you are when you buy, the lower the premium and the shorter the time before pre-existing conditions (if any develop later) are covered. This is the same logic as buying term insurance early — the cost of waiting compounds in the form of higher premiums and potentially uncoverable conditions.

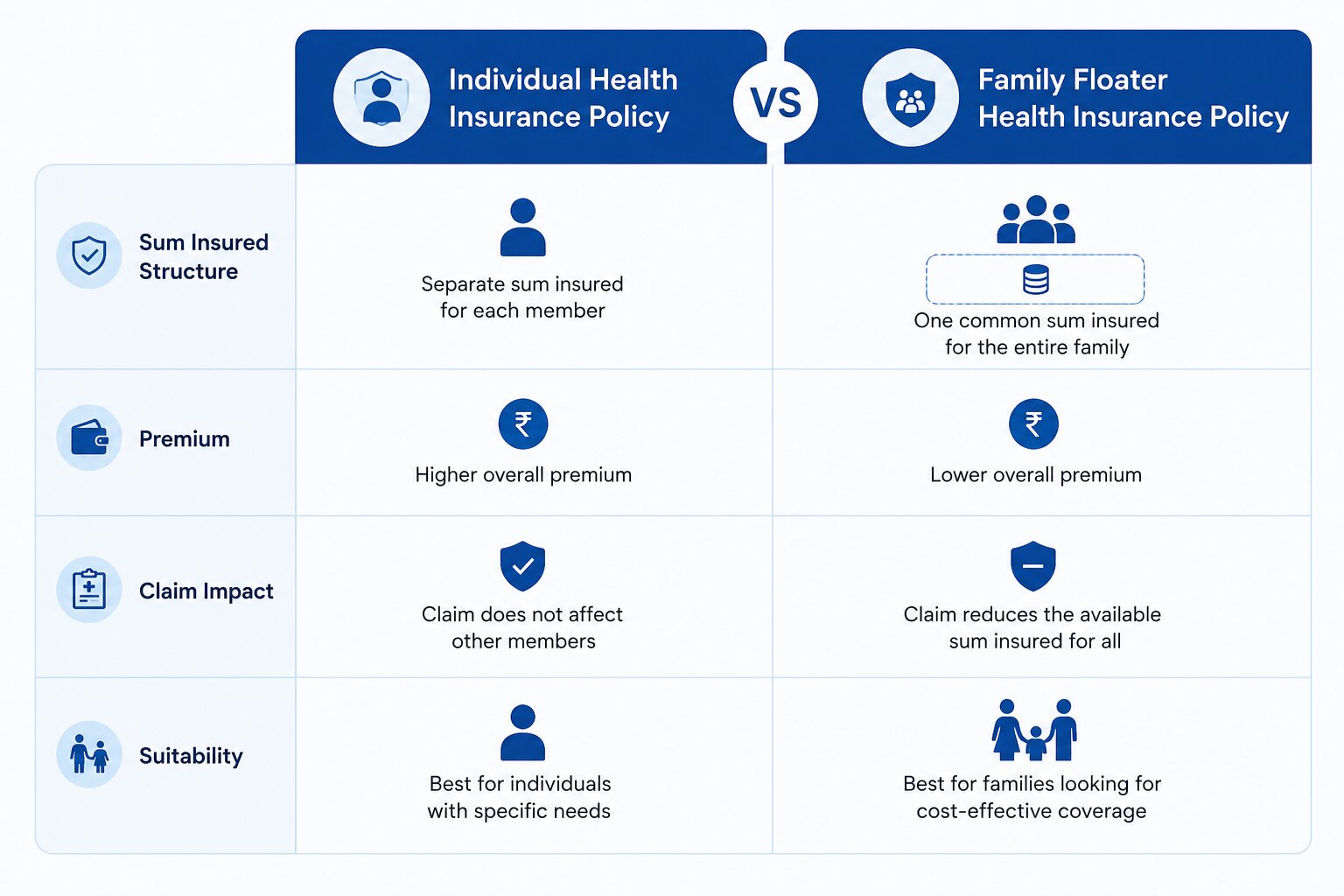

Individual policy vs family floater — which makes more sense

A family floater is a single policy with one sum insured shared among all family members. It is typically cheaper than buying separate individual policies for each member. But the shared nature is also its limitation.

| Family Floater | |

| How it works | One pool of sum insured shared by all covered members |

| Advantage | Usually 30–40% cheaper than equivalent individual policies for each member |

| Risk | One member’s serious illness can exhaust the entire sum insured, leaving others with no cover for the rest of the year |

| Best for | Young families where serious simultaneous illness for multiple members is unlikely |

| Caution for seniors | Adding senior parents to a floater significantly raises premiums; individual senior policies are often better value |

A common approach: individual policies for senior parents, a family floater for the working adults and children, with a super top-up on top for extended coverage at lower additional cost.

What changed in 2025-26 that affects your health insurance

Several regulatory changes from IRDAI affect health insurance buyers in 2026:

- PED waiting period capped at 3 years. IRDAI reduced the maximum Pre-Existing Disease waiting period from 4 years to 3 years in 2025. Any policy that previously had a 4-year PED waiting period must now comply with the 3-year cap. If you were approaching the end of a 4-year waiting period, this change may mean you are already covered.

- GST reduced on individual health insurance. GST on individual health insurance policies dropped from 18% to 5% or 0% for some categories in early 2026. This has meaningfully reduced the effective cost of buying a new policy for individuals — check with your insurer for the applicable GST rate on the specific plan you are considering.

- Senior citizen premium increases capped. IRDAI now requires insurers to limit premium increases for senior citizens to 10% per year, and must consult the regulator before implementing higher increases. This provides more predictability for senior policyholders who had previously seen sharp annual premium hikes.

- Portability rules strengthened. You can now port your health policy to a new insurer at least 45 days before renewal, with all accrued waiting period credits transferring. The porting process has been made more transparent, with IRDAI requiring insurers to process portability requests within defined timelines.

The Section 80D tax benefit — and why it should not drive your decision

Health insurance premiums qualify for deduction under Section 80D of the Income Tax Act, under the old tax regime. The limits for FY 2026-27 are: ₹25,000 for yourself, spouse, and children; ₹25,000 additional for parents under 60; ₹50,000 for senior citizen parents. The combined deduction can reach ₹75,000 if your parents are seniors. See our detailed guide on old vs new tax regime for how this interacts with your regime choice.

The tax benefit is real and worth claiming. But it should not be the primary reason to choose a particular cover amount or policy. A ₹5 lakh policy chosen because it fits neatly within the 80D limit is inadequate if your healthcare needs require ₹20 lakh cover. The cover amount should be determined by your actual risk exposure — the tax benefit is secondary.

Five things to do before buying any health insurance policy

Rather than a checklist of features, these are the five decisions that most affect your outcome:

- Decide your minimum sum insured first. Use the framework in Section 3. Do not start from the premium and work backwards to a cover amount — that is the most common mistake and the one most likely to leave you underinsured.

- Check for room rent limits and co-pay before anything else. These two terms have the biggest impact on out-of-pocket cost at claim time. A lower-premium policy with room rent capping can cost you more in the end than a higher-premium policy without it.

- Verify the CSR on IRDAI’s website, not the insurer’s own materials. IRDAI publishes the annual CSR for all insurers — this is the authoritative figure. Insurer-published CSR numbers sometimes use different calculation methodologies.

- Disclose all pre-existing conditions accurately. Non-disclosure is the leading cause of claim rejection. A claim discovered to involve an undisclosed pre-existing condition can be rejected and the policy cancelled — even if the condition was not the direct cause of hospitalisation.

- Buy before you need it. Health insurance is priced on current health. A diagnosis of diabetes or hypertension before buying will result in higher premiums, a loading, or an exclusion on that condition. The best time to buy is when you are young and healthy — not when you first need it.

Also Read: Jeevan anand (plan-149) maturity calculator | How to Increase Your SIP Amount Over Time

Questions people ask when buying health insurance

Is a ₹5 lakh health cover enough in 2026?

For most serious illnesses requiring a week of private hospital care in a metro city, ₹5 lakh is insufficient in 2026. A cardiac procedure, a cancer treatment cycle, or a major accident with ICU stay routinely costs ₹8–15 lakh in major cities. At 14% medical inflation annually, ₹5 lakh in 2026 has the purchasing power of roughly ₹2.6 lakh in 2021 terms. The minimum recommended cover for an individual in a metro is ₹25 lakh — achievable at lower premium cost through a ₹5–10 lakh base policy topped with a super top-up plan.

Can I buy health insurance if I already have a condition like diabetes or hypertension?

Yes — insurers cannot refuse to cover you solely because of a pre-existing condition. They will cover it after the waiting period, which is now capped at a maximum of 3 years by IRDAI (reduced from 4 years in 2025). During the waiting period, claims related to the pre-existing condition are excluded; all other conditions are covered from day one or after the standard initial waiting period (typically 30 days). Declaring the condition accurately is essential — non-disclosure can result in claim rejection.

What is the difference between a cashless claim and a reimbursement claim?

In a cashless claim, the hospital bills the insurer directly — you pay only what is not covered (co-pay, non-payable items, amounts above room rent limit). In a reimbursement claim, you pay the hospital first and then submit bills to the insurer for repayment. Cashless claims require you to be at a network hospital — a hospital that has an empanelment agreement with your insurer’s TPA. Reimbursement claims allow treatment anywhere but require documentation and take longer to process. In an emergency, any hospital can admit you and a reimbursement claim can be filed afterwards.

My employer gives me ₹5 lakh group cover. Do I still need a personal policy?

Yes. Employer cover ends when employment ends — which may happen through resignation, layoff, or retirement at exactly the moment your healthcare needs are highest. The sum insured (₹5 lakh) is also typically insufficient for a serious illness. Buying a personal policy when you are young and employed costs significantly less than buying one after losing the employer cover, when you may be older or have developed conditions. Building a personal policy alongside employer cover is the same logic as maintaining your own emergency fund even when your employer provides some financial security — the two serve the same purpose at different layers.

What is a super top-up policy and how is it different from a regular top-up?

A top-up policy covers a single hospitalisation bill above a deductible amount. A super top-up covers the total of all hospitalisation bills in a year that exceed the deductible — meaning it can be triggered multiple times. For example, with a ₹5 lakh base policy and a ₹20 lakh super top-up with ₹5 lakh deductible: if you have two hospitalisations of ₹7 lakh each in a year, your base policy covers the first ₹5 lakh of each, and the super top-up covers the remaining ₹2 lakh from each. A regular top-up would only cover the first incident above the deductible, not subsequent ones. Super top-ups are significantly more useful for families.

Is health insurance premium tax-deductible under the new tax regime?

No. Section 80D deductions — including health insurance premiums — are not available under the new tax regime. They apply only under the old regime. If you are on the new regime, you do not get a tax benefit from your health insurance premium, but you should still maintain adequate health cover regardless. The health insurance decision should be made independently of tax considerations. See our guide on old vs new tax regime for the full picture of what deductions are available under each.

The one number to remember from this article

14% annual medical inflation. That single figure is the reason health insurance is not optional, not adequately replaced by an emergency fund alone, and not something to under-buy based on today’s premium cost. A ₹3 lakh hospitalisation in 2026 will cost ₹6 lakh by 2031 and ₹12 lakh by 2036.

An emergency fund handles predictable financial shocks. Health insurance handles unpredictable, large-ticket medical events that no emergency fund is realistically sized to absorb. The two are complementary, not alternatives. Once you have a policy in place, review the sum insured every 3–5 years — the same 14% annual medical inflation that makes insurance necessary also erodes the real value of a fixed sum insured over time.

Disclaimer: This article is for educational and informational purposes only. It does not constitute insurance advice or a recommendation to buy any specific health insurance policy or insurer. All figures — including medical inflation rate, CSR data, IRDAI rule changes, and premium thresholds — are based on publicly available sources verified June 29, 2026, and are subject to change. Sum insured recommendations are indicative frameworks, not personalised advice. Policy terms, premiums, and IRDAI regulations may have changed after the date of verification. NiveshKarlo does not endorse any specific insurer or health insurance product. Please consult an IRDAI-licensed insurance advisor for guidance specific to your health profile, family composition, and city of residence.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.