Old vs New Tax Regime: Which One Actually Saves You More?

Every April, your employer asks you to declare your tax regime. Most salaried employees guess. This article does the maths for you — at five salary levels — so you can decide in five minutes.

Transparency note: Drafted with AI assistance and reviewed by the NiveshKarlo team. All tax slabs, rebate limits, and deduction rules were live-searched and verified on May 28, 2026 before any calculation was made. Budget 2026 confirmed no changes to FY 2026-27 slab rates. For informational purposes only — not tax advice.

Every April in India, the same thing happens. Your HR or payroll team sends a form — usually one line: “Please declare your tax regime for the current financial year: Old or New.” And most salaried employees either guess, go with whatever they chose last year, or pick whichever their colleague mentioned in passing.

This article skips the theory and goes straight to the numbers. The short version: under the new tax regime, income up to ₹12.75 lakh is effectively zero tax for salaried employees in FY 2026-27. But once you cross that, or if you have significant deductions — a home loan, HRA in a metro, heavy 80C investments — the old regime can still save you more. The break-even point shifts at every income level, which is exactly what the five worked examples below calculate.

FY 2026-27: What changed and what stayed the same

Before the calculations, one important fact: Budget 2026 made no changes to either regime’s slab rates, rebate limits, or standard deductions for FY 2026-27. The structure from last year continues exactly as-is. What did change is that the new Income Tax Act 2025 came into effect from April 1, 2026 — replacing the 1961 Act — but this is a structural and language change, not a rates change.

So if you are comparing this year’s decision to last year’s, your break-even point is in the same place. What may have changed is your personal situation — a new home loan, a salary hike that pushed you to a higher slab, or moving to a rented flat in a new city.

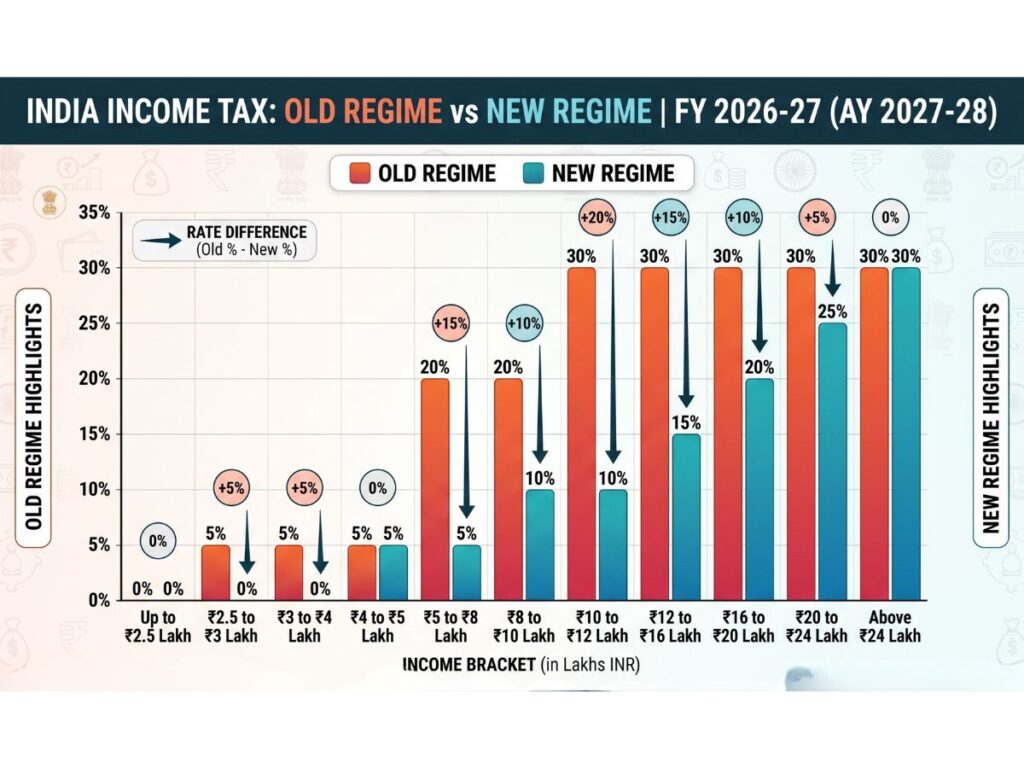

The new regime at a glance — FY 2026-27

| Taxable Income | Tax Rate |

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Standard deduction: ₹75,000. Section 87A rebate: ₹60,000 for taxable income up to ₹12 lakh → gross salary up to ₹12.75 lakh is zero tax. 4% health and education cess applies on final tax liability.

The old regime at a glance — FY 2026-27 (below 60 years)

| Taxable Income | Tax Rate |

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Standard deduction: ₹50,000. Section 87A rebate: ₹12,500 for taxable income up to ₹5 lakh. Deductions available: 80C, 80D, HRA, home loan interest (Section 24b), LTA, and others. 4% cess applies.

What deductions you keep — and what you give up in the new regime

The new regime is not simply the old regime with lower rates. It removes almost all the deductions that reduce your taxable income in the first place. This table is the most important thing to check before looking at the salary examples.

| Deduction / Exemption | Old Regime | New Regime |

| Standard deduction (salaried) | ₹50,000 | ₹75,000 |

| Section 80C — EPF, PPF, ELSS, LIC, home loan principal, tuition fees | Up to ₹1,50,000 | Not available |

| Section 80D — health insurance premium | Up to ₹25,000 (₹50,000 seniors) | Not available |

| HRA — House Rent Allowance | Actual exemption or formula, whichever is lower | Not available |

| Home loan interest — Section 24(b), self-occupied property | Up to ₹2,00,000 | Not available |

| LTA — Leave Travel Allowance | Available | Not available |

| NPS — your own contribution — Section 80CCD(1B) | Up to ₹50,000 additional | Not available |

| NPS — employer’s contribution — Section 80CCD(2) | Up to 10% of basic salary | Up to 14% of basic salary |

| Section 87A rebate | ₹12,500 (income up to ₹5L) | ₹60,000 (income up to ₹12L) |

One deduction the new regime actually improves on: employer NPS contribution under Section 80CCD(2) — up to 14% of basic salary, versus 10% in the old regime. If your employer contributes to NPS as part of your CTC, this deduction still applies under the new regime and can make a meaningful difference at higher salary levels. Worth confirming with your payroll team.

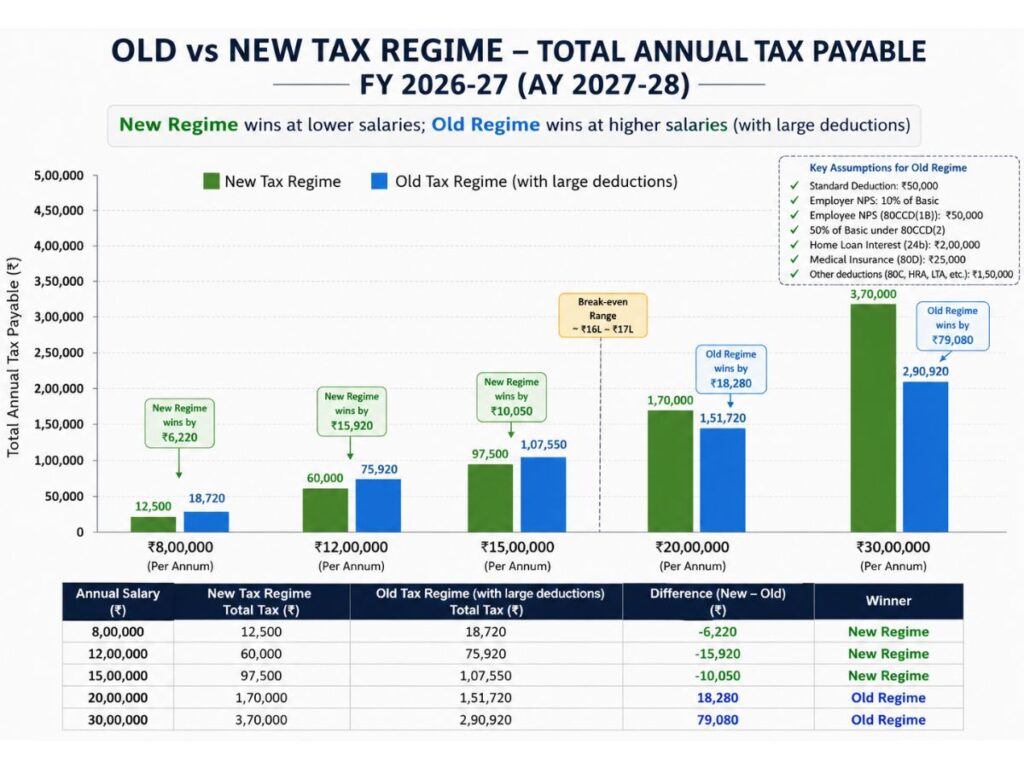

Five salary levels, real calculations — which regime wins where

All figures below use verified FY 2026-27 slab rates from incometax.gov.in. The method: gross salary minus standard deduction = taxable income, then apply slab rates, apply 87A rebate where eligible, add 4% cess. For old regime examples, deductions are layered in progressively to show exactly where the break-even sits. These are illustrations — your actual liability depends on your specific income components and documented deductions.

₹8 lakh gross salary

Early career, 3–4 years in. Paying rent, EPF being deducted, possibly an LIC policy. No home loan yet.

| New Regime | Old Regime (80C ₹1L + 80D ₹25K) | |

| Gross salary | ₹8,00,000 | ₹8,00,000 |

| Standard deduction | −₹75,000 | −₹50,000 |

| 80C + 80D | — | −₹1,25,000 |

| Taxable income | ₹7,25,000 | ₹6,25,000 |

| Tax before cess | ₹36,250 | ₹37,500 |

| Section 87A rebate | — | — |

| 4% cess | ₹1,450 | ₹1,500 |

| Total tax payable | ₹37,700 | ₹39,000 |

| New regime saves | ₹1,300 |

At ₹8 lakh, the new regime wins even when you are claiming both 80C and 80D in the old regime. The lower slab rates and higher standard deduction outweigh those deductions at this income level. If your gross is below ₹12.75 lakh, the case for the new regime is even stronger — your tax is zero.

₹12 lakh gross salary

Mid-career. Metro city, paying rent, PPF contributions, health insurance in place.

| New Regime | Old Regime (80C ₹1.5L + 80D ₹25K + HRA ₹1.2L) | |

| Gross salary | ₹12,00,000 | ₹12,00,000 |

| Standard deduction | −₹75,000 | −₹50,000 |

| 80C + 80D + HRA | — | −₹2,95,000 |

| Taxable income | ₹11,25,000 | ₹8,55,000 |

| Tax before cess | ₹56,250 | ₹71,000 |

| 4% cess | ₹2,250 | ₹2,840 |

| Total tax payable | ₹58,500 | ₹73,840 |

| New regime saves | ₹15,340 |

Even with a significant HRA claim, full 80C, and health insurance, the new regime still wins at ₹12 lakh. This surprises most people — the assumption that old regime + deductions always beats the new regime is not accurate at this income level.

₹15 lakh gross salary — the break-even zone

Senior professional or mid-level manager. This is where the regimes become genuinely competitive, and your specific deduction total decides it.

| New Regime | Old (80C + 80D + HRA ₹1.5L) | Old (80C + 80D + HRA + Home Loan ₹2L) | |

| Gross salary | ₹15,00,000 | ₹15,00,000 | ₹15,00,000 |

| Standard deduction | −₹75,000 | −₹50,000 | −₹50,000 |

| All deductions | — | −₹3,25,000 | −₹5,25,000 |

| Taxable income | ₹14,25,000 | ₹11,25,000 | ₹9,25,000 |

| Tax before cess | ₹1,48,750 | ₹2,12,500 | ₹1,42,500 |

| 4% cess | ₹5,950 | ₹8,500 | ₹5,700 |

| Total tax payable | ₹1,54,700 | ₹2,21,000 | ₹1,48,200 |

| Winner | New regime | New regime saves ₹66,300 vs old | Old regime saves ₹6,500 |

| The break-even at ₹15 lakh salary: If your total deductions above the standard deduction exceed ~₹3.75 lakh → old regime saves more. Below ₹3.75 lakh in deductions → new regime saves more. At ₹15 lakh, the home loan interest deduction of ₹2 lakh is what tips the balance. Without it, the new regime still wins comfortably. |

₹20 lakh gross salary

Department head or senior manager. Home loan, metro HRA, full 80C and 80D. The old regime becomes noticeably competitive here.

| New Regime | Old (80C ₹1.5L + 80D ₹25K + HRA ₹2L + Home Loan ₹2L) | |

| Gross salary | ₹20,00,000 | ₹20,00,000 |

| Standard deduction | −₹75,000 | −₹50,000 |

| All deductions | — | −₹5,75,000 |

| Taxable income | ₹19,25,000 | ₹13,75,000 |

| Tax before cess | ₹3,37,500 | ₹2,62,500 |

| 4% cess | ₹13,500 | ₹10,500 |

| Total tax payable | ₹3,51,000 | ₹2,73,000 |

| Old regime saves | ₹78,000 |

At ₹20 lakh with this deduction profile, the old regime saves close to ₹78,000 per year. That is a meaningful amount — roughly six times the annual cost of a standard family health insurance policy.

₹30 lakh gross salary

Senior leadership or specialist role. The old regime advantage widens further as the 30% slab applies to a smaller portion of income when deductions are large.

| New Regime | Old (80C + 80D + HRA ₹2.4L + Home Loan ₹2L) | |

| Gross salary | ₹30,00,000 | ₹30,00,000 |

| Standard deduction | −₹75,000 | −₹50,000 |

| All deductions | — | −₹6,15,000 |

| Taxable income | ₹29,25,000 | ₹23,35,000 |

| Tax before cess | ₹7,07,500 | ₹5,90,500 |

| 4% cess | ₹28,300 | ₹23,620 |

| Total tax payable | ₹7,35,800 | ₹6,14,120 |

| Old regime saves | ₹1,21,680 |

At ₹30 lakh, the old regime advantage exceeds ₹1.2 lakh per year with this deduction profile. The gap is driven by the same principle: in the old regime, a larger portion of income is shielded from the 30% slab through deductions.

How to decide in under five minutes

All five examples reduce to a single principle: the new regime wins when your deductions are small; the old regime wins when they are large. Use this quick check:

Step 1 — Add up only the deductions you will actually have documented this year:

- Section 80C: EPF (your contribution), PPF, ELSS, LIC premium, home loan principal, tuition fees — up to ₹1,50,000

- Section 80D: health insurance premium — up to ₹25,000

- HRA: if you live in rented accommodation — actual exemption amount (use formula: least of actual HRA received, 50%/40% of basic, actual rent minus 10% of basic)

- Home loan interest Section 24(b): up to ₹2,00,000 for self-occupied property

- Employer NPS contribution 80CCD(2): NPS employer contribution — 14% of basic in new regime, 10% in old. Available in BOTH regimes.

Step 2 — Add them up and find yourself in this table:

| Gross salary | If total deductions above std. deduction are… | Pick this regime |

| Up to ₹12,75,000 | Any amount | New regime — zero tax regardless |

| ₹12.75L – ₹15L | Below ~₹3.75 lakh | New regime |

| ₹12.75L – ₹15L | Above ~₹3.75 lakh | Old regime |

| ₹15L – ₹20L | Below ~₹4.5 lakh | New regime |

| ₹15L – ₹20L | Above ~₹4.5 lakh | Old regime |

| Above ₹20L | Below ~₹5.5 lakh | New regime likely saves more |

| Above ₹20L | Above ~₹5.5 lakh | Old regime likely saves more |

These are approximations based on the worked examples. Your precise break-even depends on your income components, HRA city tier, and actual deduction amounts. The official income tax calculator at incometax.gov.in computes both regimes simultaneously from your inputs and gives a precise answer.

If you choose the new regime — what happens to your 80C investments?

A common worry: if 80C deductions are unavailable, should you stop investing in PPF, ELSS mutual funds, or continuing your LIC premiums?

The answer is no — and this distinction matters. Choosing the new regime means you cannot claim a tax deduction for those investments. It does not mean the investments themselves stop working. Your PPF account still earns 7.1% tax-free interest. Your EPF contributions continue. Your ELSS fund keeps running.

Whether 80C instruments still make financial sense without the deduction depends on the specific product. PPF at 7.1% tax-free remains a strong savings instrument regardless of the regime you choose. ELSS funds — equity mutual funds with a 3-year lock-in — need to be evaluated on their own merits as market-linked products; our guide on how to analyse a mutual fund covers what to look for. If you are in the new regime and reconsidering how to deploy monthly savings, index funds and SIP-based investing are worth understanding — they do not require a lock-in and are not tied to tax saving.

Can you switch every year — and when should you review?

Salaried employees with no business income can switch between regimes every financial year. The new regime is the default — if you do nothing when submitting your tax declaration to HR, you land on the new regime. You can opt for the old regime by informing payroll at the start of the year, usually through your company’s tax declaration form or Form 10-IEA.

The practical implication: review your regime choice whenever your personal situation changes meaningfully. Taking a new home loan, paying off the last EMI, moving from a rented flat to your own property, or a significant salary hike can all shift your break-even point.

One specific scenario worth noting: if you have built an emergency fund and are now starting to invest more aggressively, your 80C investments may increase — which could push you over the break-even deduction threshold and make the old regime worth revisiting. The regime decision and your overall savings plan interact with each other.

Questions salaried employees ask every April

Is the new tax regime always better in FY 2026-27?

Not always. For gross salary up to ₹12.75 lakh, yes — zero tax under the new regime regardless of deductions, so there is no reason to choose the old regime. For higher incomes, the answer depends entirely on your total deductions. The five worked examples in this article show where each regime wins.

I have a home loan and also pay rent. Can I claim both?

HRA exemption and home loan interest deduction can both be claimed in the old regime, but only if the rented property and the mortgaged property are in different cities — for example, you work in Bengaluru (renting) and own a property in Pune. If both are in the same city, you cannot claim HRA simultaneously with home loan benefits on that property. This is a common point of confusion; confirm with your CA before claiming.

My employer defaulted me to the new regime. Can I switch now?

Yes. The new regime is the default, but you can switch to the old regime at the time of filing your ITR — even if your employer deducted TDS under the new regime all year. Any excess TDS will be refunded. If you want your employer to deduct TDS under the old regime going forward, submit the regime declaration at the start of the financial year.

Does NPS help reduce tax in the new regime?

Only the employer’s contribution to NPS is deductible under the new regime — under Section 80CCD(2) at up to 14% of basic salary. Your own NPS contribution is not deductible under the new regime. If your employer offers NPS contribution as part of your CTC, this deduction applies in the new regime and reduces your taxable income. Worth confirming with your payroll team whether this is structured in your salary.

What is the break-even deduction level at ₹15 lakh?

At ₹15 lakh gross salary, if your total deductions above the standard deduction exceed approximately ₹3.75 lakh, the old regime saves more. The home loan interest deduction of ₹2 lakh combined with 80C and 80D typically crosses this threshold for someone with a home loan — which is why the old regime wins in Example 3 when all four deductions are included.

How this article was put together

All tax slabs, rebate limits, standard deductions, and deduction rules were live-searched and verified on May 23, 2026 from incometax.gov.in, ClearTax, and multiple tax portals before any calculation was made. Budget 2026 confirming no slab changes for FY 2026-27 was cross-checked across HDFC Bank, Axis Max Life, and Bajaj Finserv budget analysis pages published in April 2026.

The worked examples were calculated manually step-by-step using verified slab rates, then cross-checked against online calculators. Small rounding differences may appear in the cess calculation. All examples are illustrative — actual tax liability depends on precise income components, HRA city classification, documented deduction amounts, and individual circumstances.

This is informational content, not tax advice. For a precise calculation, use the official income tax calculator. For advice specific to your situation, consult a qualified Chartered Accountant.

Sources

Tax slab rates and rebate limits are from the Income Tax Department India. The confirmation that Budget 2026 made no changes to FY 2026-27 slab rates was verified from HDFC Bank and ClearTax budget analysis published April 2026. The Section 80CCD(2) NPS limit of 14% of basic salary under the new regime was confirmed from the SEBI investor education portal and incometax.gov.in. Monetary policy context referenced from RBI.

Disclaimer: This article is for educational and informational purposes only. It does not constitute tax advice or financial advice. All worked examples are based on verified slab rates as of May 23, 2026 and are illustrative only. Actual tax liability depends on individual income structure, deductions, and applicable exemptions. Tax laws are subject to change. NiveshKarlo does not recommend any specific tax regime — the choice is a personal financial decision. Please consult a qualified Chartered Accountant for advice specific to your situation.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.