Which Date Is Best for SIP? The Honest Answer

Short answer: it doesn’t matter much. Here is the data behind that claim — and the one factor that actually should guide your date choice.

Transparency: AI-assisted draft reviewed by the NiveshKarlo team. SIP date analysis data sourced from Zerodha Fund House (18+ year study, July 8 2025) and Scripbox (Nifty 100 analysis, September 2025). Informational only — not investment advice.

When you set up a SIP on any mutual fund app, it asks you to pick a date. Almost everyone pauses here. The 1st? The 5th? The 10th? Some have heard the 25th is better. Some pick the 1st because it feels like a clean start. Some pick a date that happens to be available. None of this matters as much as you think — and the data now covers 18 years to prove it.

Zerodha Fund House ran a scenario analysis across 31 different SIP dates over more than 18 years, using three different Nifty indices. The result: there is no specific date that consistently gives better returns. The difference in XIRR between the best-performing date and the worst-performing date across their analysis was too small to be a meaningful factor in any investment decision.

This is the honest answer to a question that generates an enormous amount of speculation online. The rest of this article explains what the data actually shows, why the date doesn’t matter for returns, and what the date choice actually does matter for — which is something different entirely.

What 18 years of Nifty data says about SIP dates

The Zerodha Fund House analysis tested all 31 possible SIP dates using three indices — Nifty 50, Nifty LargeMidcap 250, and a third index — over 18+ years of historical data. For each date, they calculated what an investor’s XIRR would have been if they had invested on that specific date every single month for the entire period.

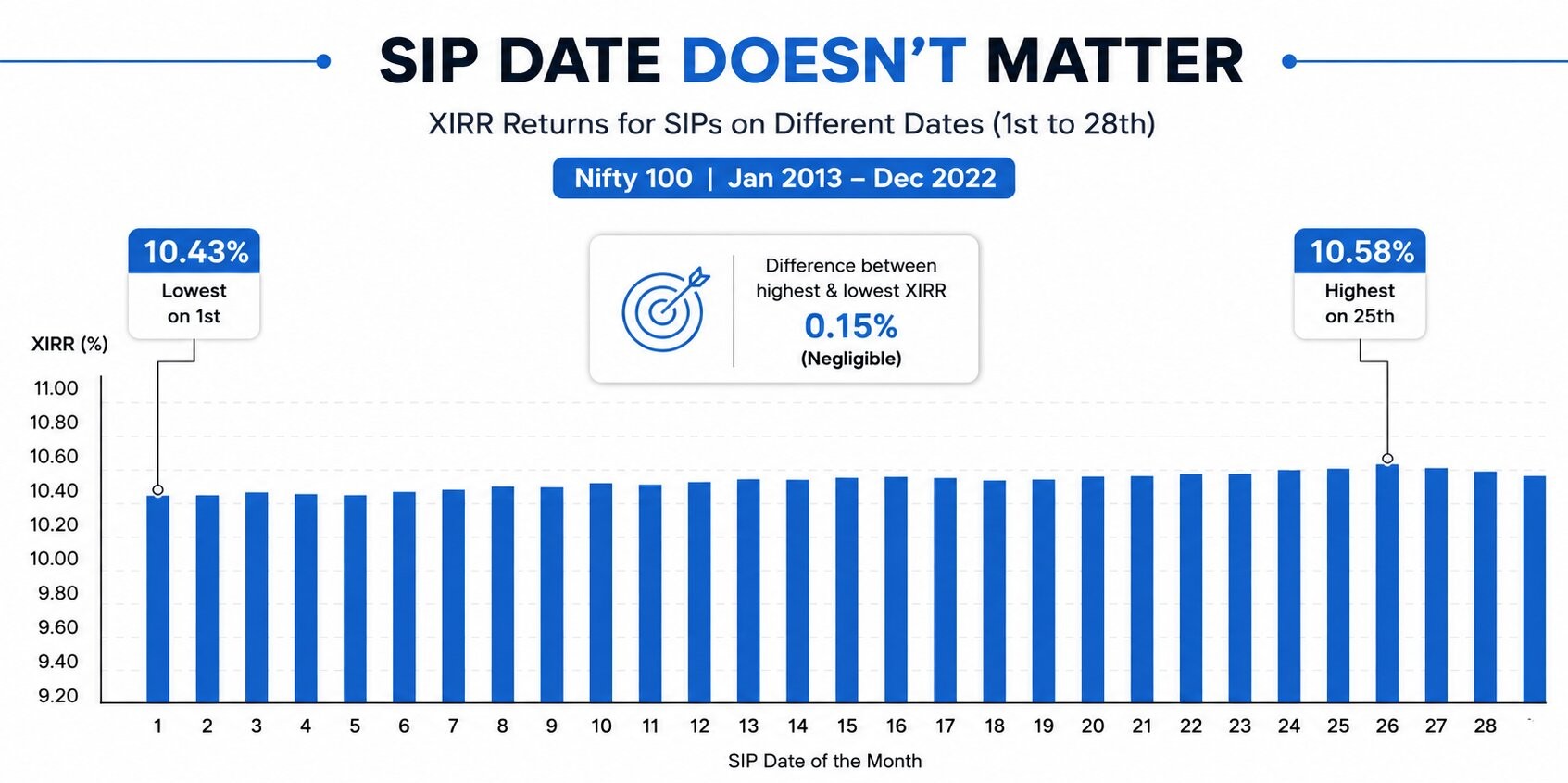

| What they found: The XIRR across all 31 dates was nearly identical. The gap between the highest-returning date and the lowest-returning date was so small it would not change a financial decision. A Scripbox analysis on the Nifty 100 (January 2013 to December 2022, ₹10,000/month SIP) tested 7 specific dates: 1st: 10.43% XIRR 5th: 10.46% XIRR 10th: 10.49% XIRR 15th: 10.51% XIRR 20th: 10.53% XIRR 25th: 10.58% XIRR ← highest 28th: 10.47% XIRR Difference between highest (25th) and lowest (1st): 0.15% in XIRR. In rupee terms over the entire period: approximately ₹2,300. On a ₹10,000/month SIP running for 10 years, ₹2,300 is the total difference between the best possible date and the worst. This is not a meaningful number. |

The reason the date doesn’t matter is the same reason SIP investing works in the first place: rupee cost averaging. A SIP buys units at whatever NAV the market happens to be on that date. Over months and years, market ups and downs on any given date average out. A date that happens to fall on a market high one month may fall on a market low the next. There is no predictable pattern to exploit, and no date that avoids the highs or catches the lows with any consistency over a long horizon.

What the date choice actually affects — and why it matters

If returns don’t meaningfully differ by date, why does the question keep coming up? Because there is one thing the date genuinely affects, and it’s not returns. It’s whether the SIP goes through at all.

A SIP instalment that fails because your bank account doesn’t have enough balance on the debit date means you miss that month’s unit purchase entirely. A missed instalment is not a small rounding error — it is zero units bought at that month’s NAV, which may have been higher or lower than the months before and after. Repeated missed instalments compound into real underperformance, not from the date chosen but from the inconsistency of the investment.

This is the single most important practical consideration in choosing a SIP date. Pick a date when your bank account reliably has money in it. For most salaried people, that means 2–4 days after salary credit — enough time for the salary transfer to clear, but not so long that other expenses have depleted the balance.

How to choose your date based on when you get paid

| Salary credit date | Suggested SIP date |

| 1st of the month | 3rd to 5th — salary clears, buffer for transfer delays |

| 5th of the month | 7th to 10th — same logic |

| 7th of the month | 10th to 12th |

| 10th of the month | 12th to 15th |

| Last working day | 3rd to 5th of following month |

| Variable / freelance income | Split across two dates — e.g. 5th and 20th — or align with when clients typically pay |

One additional consideration: if you already have EMIs going out on specific dates, avoid setting SIP dates too close to those debits. The combined outflow may leave the account thin. The NACH mandate (which authorises the auto-debit) makes no allowance for days when the balance is low — the debit is attempted on the date you set, and if it fails, the instalment is missed.

The mistakes that actually affect SIP outcomes — not the date

Since the date itself is not a meaningful lever, here are the factors that actually determine how much wealth a SIP builds over time — and the common errors that erode it:

- Pausing during market falls. This is the most damaging behaviour, and it has nothing to do with the date. Investors who stopped SIPs in 2020 when markets fell missed the cheapest unit purchases of that cycle. The date of the month is irrelevant; the decision to stay invested through a fall is what matters. See our detailed article on what happens to your SIP when the market falls.

- Not increasing the SIP amount as income grows. A ₹5,000 SIP started at 26 and never increased is significantly less effective than the same SIP stepped up by 10% annually. The date has no role in this; the amount and its growth rate do. See how to increase your SIP amount over time.

- Missing instalments due to low balance. As described above — this is the one outcome the date choice can influence, and it’s solved by aligning with salary cycle rather than optimising for marginal XIRR differences.

- Starting too late because the ‘right date’ hasn’t been decided. The time cost of waiting while deliberating over SIP date is concrete and measurable. A month’s delay in starting a 20-year SIP costs more in foregone compounding than any date-selection benefit could recover. Pick any date, start, and adjust later if needed.

Also Read: Health Insurance Basics: What You Need to Know Before You Buy | How to File ITR for Salaried Individuals: FY 2025-26 Guide

Questions people ask about SIP dates

Does the SIP date affect returns?

An 18+ year analysis by Zerodha Fund House across 31 different dates found no meaningful difference in XIRR between any dates tested. A Scripbox analysis on Nifty 100 from 2013 to 2022 found the highest and lowest performing dates differed by just 0.15% in XIRR — equivalent to approximately ₹2,300 in rupee terms over the full period. For a long-term SIP, this is not a number worth optimising around.

Is the 1st or 5th or 25th the best date for SIP?

No single date is consistently best across funds, time periods, or market conditions. Different analyses using different funds and time windows produce different ‘winning’ dates because market movements don’t follow calendar patterns. The 25th was marginally best in one Nifty 100 analysis over one specific decade — that doesn’t make it the best date for a different fund, a different decade, or your specific situation.

Should I split my SIP across two dates?

Some investors split a monthly SIP into two instalments — say, half on the 5th and half on the 20th — to smooth out short-term NAV fluctuations within a month. This is operationally fine but adds no meaningful long-term benefit that a single monthly SIP doesn’t already provide through rupee cost averaging. Rupee cost averaging already averages out price variations across months; splitting within a month adds another layer of averaging across a period that doesn’t accumulate to meaningful differences over years. It is not wrong, but it is not necessary.

What if my salary comes on different dates each month?

If your income is irregular — freelance work, variable pay, or a salary that credits on different dates — consider a weekly SIP if your platform supports it, or split across two monthly dates to reduce the chance of a low-balance failure on either. The more important step is to maintain a buffer in your account — ideally as part of your emergency fund — so SIP instalments go through regardless of when income arrives.

Can I change my SIP date after it has started?

Yes. Most platforms and AMCs allow you to modify the SIP date. The process varies by platform — on most apps it is a straightforward change in the SIP settings. Note that the change typically takes effect from the next SIP cycle, not the current month. If your current date is causing consistent balance problems, changing it is far better than pausing the SIP.

Does the SIP date matter for tax purposes?

For equity mutual funds, the holding period — which determines whether a gain is short-term (STCG at 20%) or long-term (LTCG at 12.5% above ₹1.25 lakh) — is calculated from the purchase date of each unit. Since each SIP instalment is a separate purchase, each instalment’s holding period starts on its own SIP date. This means if you plan to redeem after exactly 12 months, the units from your first instalment will be long-term while units from a later instalment may still be short-term. This is a redemption planning consideration, not a reason to change your SIP date. Your CA or the capital gains statement from your AMC handles this correctly at redemption time.

The short version: any date works. The only constraint worth applying is your own salary cycle. Pick a date 2–4 days after your salary credits, check that no other large debits land on the same day, and start. Every month spent deliberating over the optimal SIP date is a month of compounding not happening. And as the data from 18 years of Nifty indices shows, the difference between the ‘optimal’ date and the one you picked at random is smaller than a month’s bank charges.

Disclaimer: This article is for educational and informational purposes only. XIRR figures cited are from third-party analyses (Zerodha Fund House and Scripbox) based on historical index data — they do not represent the performance of any specific mutual fund scheme. Past performance does not guarantee future returns. Mutual fund investments are subject to market risk. NiveshKarlo does not recommend any specific fund, SIP date, or investment platform. Please consult a SEBI-registered investment advisor before making investment decisions.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.