What Happens to Your SIP When the Market Falls?

Your SIP keeps running. Your NAV drops. You panic. Here is what is actually happening — and why the crash might be doing you a favour.

Transparency: AI-assisted draft reviewed by the NiveshKarlo team. All market data, SIP inflow figures, and Nifty crash/recovery statistics were live-verified on June 13, 2026. Informational only — not investment advice.

You check your phone one morning. The market is down 3%. Your SIP went through last week at a NAV of ₹42. Today it is ₹38. Your portfolio shows a loss. Your instinct says: pause the SIP until things stabilise.

That instinct is understandable. It is also, in most cases, the single most expensive financial decision you will make.

This article explains what is actually happening to your SIP when the market falls — mechanically, mathematically, and in terms of real outcomes from real Indian market crashes. Not theory. Numbers. Because the AMFI data for February 2026 showed SIP inflows of ₹29,845 crore — up 15% year-on-year — even as markets fell sharply due to FII selling, crude oil crossing $105, and geopolitical pressure. That means millions of investors kept going. This article explains why that was the right call.

What literally happens to your SIP when the market falls

When the market falls, your mutual fund’s NAV (Net Asset Value) drops. On the date your SIP is scheduled, your bank account is debited for the same fixed amount — say ₹5,000 — and that amount is used to purchase units of your fund at the prevailing NAV.

Here is the key: when the NAV is lower, your ₹5,000 buys more units than it would have at a higher NAV. This is not a consolation — it is the core mechanic that makes SIP investing powerful over time.

| A simple example: SIP amount: ₹5,000 per month Month 1 (market normal): NAV = ₹50 → Units purchased = 100.00 Month 2 (market falls): NAV = ₹40 → Units purchased = 125.00 Month 3 (market falls): NAV = ₹35 → Units purchased = 142.86 Month 4 (market recovers): NAV = ₹50 → Units purchased = 100.00 Total invested over 4 months: ₹20,000 Total units accumulated: 467.86 Value at Month 4 (NAV = ₹50): ₹23,393 Had NAV stayed at ₹50 throughout, you would have bought only 400 units — worth ₹20,000. The fall actually made you ₹3,393 richer over the same period. |

This mechanism is called rupee cost averaging. It is not unique to India — but in a country where markets periodically see sharp corrections, it is especially powerful. The fall is not the enemy. Your reaction to the fall is.

What actually happened in two real crashes — 2008 and 2020

Data from NSE India’s 35-year Nifty 50 history gives us two clean case studies of what happened to SIP investors who continued versus those who stopped during major falls.

The 2008 financial crisis — Nifty fell 65%

Between January 2008 and October 2008, the Nifty 50 fell approximately 65% — from around 6,300 to 2,250. For a lump-sum investor, this was catastrophic. For a SIP investor who kept going, it was something different.

| Investor A: Continued SIP | Investor B: Paused SIP in Oct 2008 | |

| SIP amount | ₹5,000/month | ₹5,000/month (paused Oct 2008) |

| Units bought Oct 2008 | More units at crash low NAV | Zero — paused |

| Units bought Nov–Dec 2008 | More units at depressed prices | Zero — still paused |

| When market recovered (2009–10) | Large unit base appreciating | Fewer units, missed recovery |

| Outcome | Significantly higher corpus | Lower corpus, re-entered later at higher NAV |

The investors who paused did not just miss the low-NAV purchases during the crash. They missed re-entering at the right time too — most waited until the market had already recovered significantly, which meant buying at higher NAVs and with the psychological drag of having ‘sat out’ the bottom.

The COVID crash of 2020 — Nifty fell 38% in 7 weeks

From January 2020 to March 23, 2020, the Nifty 50 fell approximately 38% — from around 12,300 to 7,610. This was faster and sharper than 2008. The news was dominated by lockdowns, economic shutdowns, and predictions of prolonged depression.

| Date | Nifty 50 level | What happened to SIP investors |

| Jan 2020 | ~12,300 | Normal month. ₹5,000 buys standard units at full price. |

| Feb 2020 | ~11,100 | Market dipping. Same ₹5,000 buys slightly more units. |

| Mar 2020 | ~7,610 | Crash bottom. ₹5,000 buys the most units in years. Cheapest purchase ever. |

| Apr–Oct 2020 | Rising | Recovery begins. Units bought at the bottom now appreciating fast. |

| Nov 2020 | ~12,900 | Market fully recovered. Units bought in March worth ~70% more than purchase price. |

| Apr 2026 | ~23,000+ | Nifty more than 3× the March 2020 low. March 2020 units are worth 3× what was paid. |

The investor who paused their SIP in March 2020 — out of panic — missed the single most valuable month of unit accumulation in that entire market cycle. The investor who kept going bought their cheapest units ever, which then tripled in value over the next six years.

Image Source : AI

The one number that should make you stop worrying

Across 35 years of Nifty 50 data, there has never been a single 5-year period that delivered a negative return for a SIP investor. Not through the dot-com bust. Not through the 2008 global financial crisis. Not through COVID. Not through the 2025 market fall triggered by US tariff wars and FII outflows. Every 5-year SIP window in Nifty’s history has ended in positive territory.

This does not mean the next five years are guaranteed. Past performance is not a guarantee of future returns. But it does mean that the combination of rupee cost averaging and long holding period has historically been enough to overcome every crash the market has seen.

| What this means practically: If your SIP goal is 10, 15, or 20 years away — a market fall in year 2 or year 5 is not a threat. It is an opportunity. Your SIP buys more units at lower prices. Those units appreciate when the market recovers. The fall accelerates your wealth creation — if you do not stop. The only scenario where a market fall genuinely hurts a SIP investor is if they stop during the fall and miss the recovery. That is a self-inflicted wound. |

What happened in early 2026 — and what SIP investors did

This is not abstract history. Markets fell sharply in early 2026, driven by a combination of FII outflows, US-Iran geopolitical tensions pushing crude oil above $105 per barrel, and global risk-off sentiment. The Nifty saw several sessions of sharp single-day falls, and investor anxiety was visible across social media and financial forums.

What actually happened to SIP inflows? According to AMFI’s data, February 2026 SIP inflows were ₹29,845 crore — up 15% year-on-year. The number of SIP accounts contributing each month remained close to 9.72 crore. In other words: the overwhelming majority of SIP investors did not stop. They kept going. And they bought more units at lower NAVs during those falls than they would have in a stable month.

This is the maturity that the Indian mutual fund investor has shown over the last decade. It was not always this way — in 2008 and 2013, SIP cancellations spiked during market falls. The pattern has shifted. More investors now understand that a falling market is not a reason to stop a SIP. It is a reason to be glad you have one running.

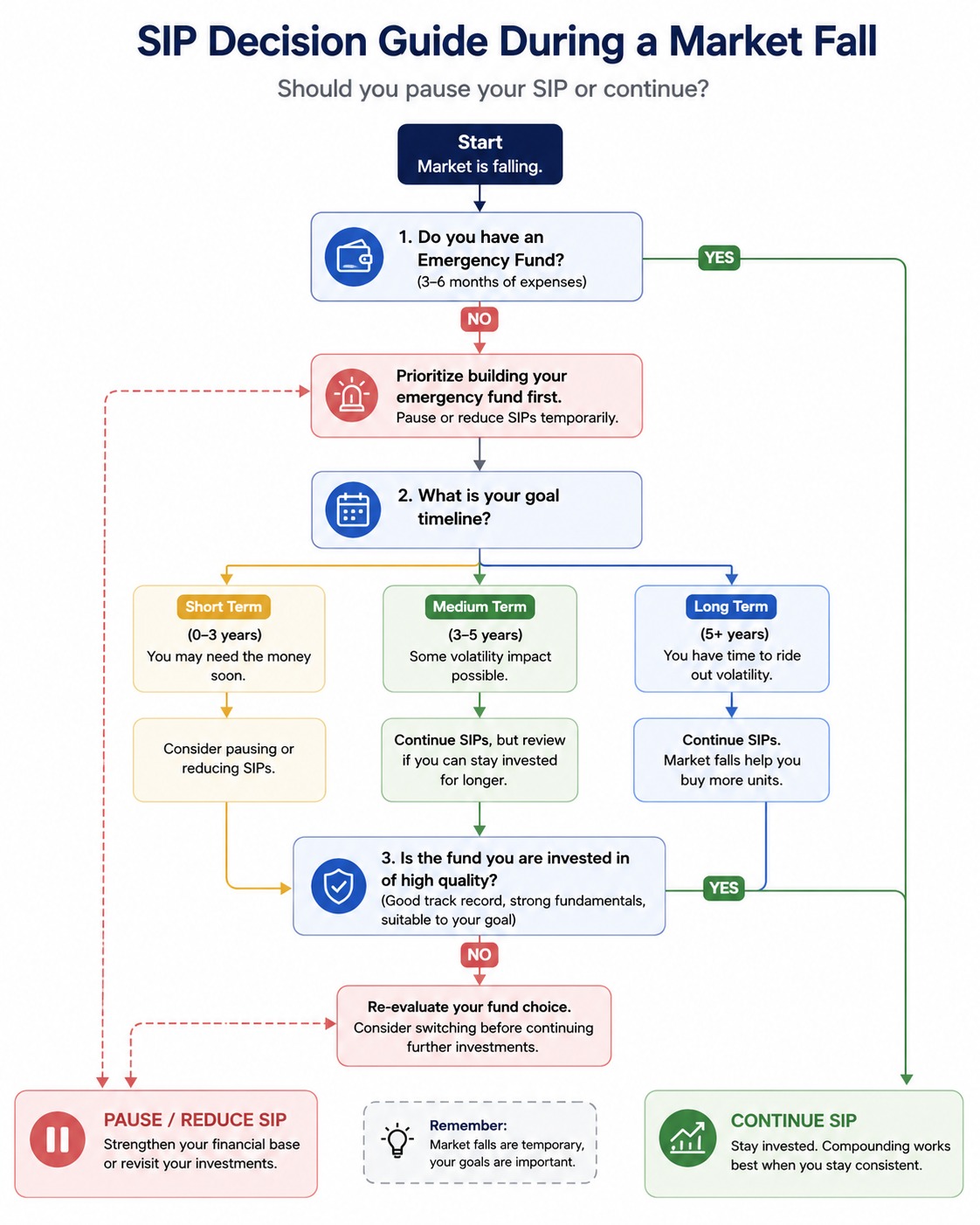

The only situations where pausing a SIP might actually make sense

Everything above argues for continuing your SIP through a market fall. But there are genuine exceptions — not based on market conditions, but based on your personal situation.

- You do not have an emergency fund. If a market fall coincides with a job loss or medical expense and you have no liquid buffer, you may be forced to redeem mutual fund units at a loss to cover expenses. This is the strongest argument for building an emergency fund before investing in equity SIPs. The emergency fund protects your SIP from being disrupted by life events.

- Your SIP goal has become short-term. If you originally started a SIP for a 10-year goal and that goal is now 12 months away, you should not be in equity in the first place — regardless of whether the market is up or down. Move to debt or liquid funds. But this is not a reason to pause. It is a reason to exit the equity fund entirely and reallocate.

- The fund itself has fundamentally underperformed. A market fall affects all equity funds. But if your specific fund has consistently underperformed its benchmark for 3+ years across market cycles, a review of the fund is warranted — not because the market fell, but because of the fund’s quality. See our guide on how to analyse a mutual fund for the right way to evaluate this.

Notably absent from this list: ‘the market has fallen X%’, ‘the news is bad’, ‘FIIs are selling’, or ‘a recession might be coming.’ None of these are valid reasons to pause a long-term SIP. They are reasons people use to rationalise a decision driven by fear.

Image Source: AI

The actual rupee cost of stopping your SIP during a fall

If you read our article on the power of SIP over time, you saw that pausing a ₹5,000/month SIP for just two years can cost approximately ₹16 lakh in final corpus over a 25-year horizon. During a market fall, the cost of pausing is even higher — because you are missing the months with the lowest NAVs and therefore the highest unit accumulation. The months you are most tempted to stop are the most valuable months to keep going.

| A rough illustration — ₹5,000/month SIP, 20-year horizon at 12% CAGR (illustrative): Uninterrupted SIP for 20 years: Estimated corpus ~₹49,96,000 Same SIP paused for 6 months at market bottom: ~₹44,80,000 (miss ~₹5.16 lakh) Same SIP paused for 12 months at market bottom: ~₹39,80,000 (miss ~₹10.16 lakh) The figures above assume the 6 and 12 months of pause occur during the lowest NAV period. Pausing at the bottom is more expensive than pausing at any other point in the cycle. All figures are illustrative. Actual returns are market-linked and not guaranteed. |

Also Read: Daily SIP Calculator: Start Investing from ₹100/Day | Top investors in Indian stock market

Questions investors ask when markets fall

Should I stop my SIP when the market is falling?

For a long-term SIP (5+ years remaining), stopping during a market fall is generally counterproductive. A falling market means your SIP buys more units per rupee — which is advantageous when prices recover. The Nifty 50’s 35-year history shows no 5-year period with a negative SIP return. The exception is if you have a personal financial reason to stop — like an absent emergency fund or a goal that has become short-term. Market conditions alone are not a valid reason.

My SIP portfolio is showing a loss. Should I exit?

A portfolio showing a loss during a market fall is normal — it reflects current market prices, not permanent loss. The loss only becomes permanent if you exit (redeem) at that point. If your goal is 5+ years away, the paper loss is temporary. Every major market fall in Indian history has been followed by a recovery and new highs. Exiting locks in the loss. Staying invested allows recovery.

Is it a good idea to increase my SIP during a market fall?

Some investors do this — it is a variant of lump-sum investing at a discount. If you have surplus funds and a long horizon, increasing your SIP amount during a fall means buying more units at lower prices. However, this should only be done if: (a) your emergency fund is fully in place, (b) you will not need the additional investment amount for at least 5 years, and (c) you are doing it from a position of financial stability, not desperation to ‘average down.’ NiveshKarlo does not recommend any specific action — this is informational context.

What if the market does not recover this time?

This is the fear that drives most SIP pauses. In 35 years of Nifty 50 data, every major crash has been followed by a full recovery and subsequent new highs. This does not guarantee the future — no one can. But India’s long-term economic growth story — demographics, urbanisation, formalisation of the economy — provides structural support for equity markets over long periods. For a nuanced understanding of long-term compounding, see our article on how compound interest works which explains why time in the market matters more than timing the market.

I started my SIP recently and it is already showing a loss. Did I invest at the wrong time?

The concern about starting at the wrong time is very common — and largely misplaced for long-term SIP investors. Because SIPs invest a fixed amount every month, even if you start at a market peak, subsequent months buy at lower prices, gradually averaging down your cost per unit. The only scenario where starting timing matters significantly is for lump-sum investments — which is why many financial planners suggest SIPs over lump sums for new investors. Your SIP is doing exactly what it is supposed to do. Give it time.

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice or a recommendation to continue, pause, or change any SIP. All corpus projections are illustrative and based on historical data or assumed CAGR rates. Mutual fund returns are market-linked and not guaranteed — past performance is not a guarantee of future returns. Market crashes referenced (2008, 2020) are historical facts; future market behaviour cannot be predicted. NiveshKarlo does not endorse any specific mutual fund, platform, or investment strategy. Please consult a SEBI-registered investment advisor before making investment decisions.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.