How to Save Tax in the New Tax Regime: FY 2026-27 Guide

Most 80C deductions are gone. HRA is gone. 80D is gone. But the new regime still has more tax-saving levers than most salaried employees realise — and the biggest one is a conversation with your HR department, not an investment decision.

When the new tax regime became the default in 2023, the conversation most salaried employees had was: “Should I stay or switch back to the old regime?” That is the right first question — and if you have not answered it properly for your specific salary and deductions, start with our guide on the comparison.

But once you have decided to stay on the new regime — or if you are new to earning and have never been on the old regime — the second question matters more: what can you actually do to reduce your tax bill under the new regime? Most articles answer this with a list of three or four deductions and leave it there. This article goes further — into salary restructuring, which is the lever most salaried employees never pull, not because it is complicated but because nobody told them it was available.

What the new regime already gives you — before you do anything

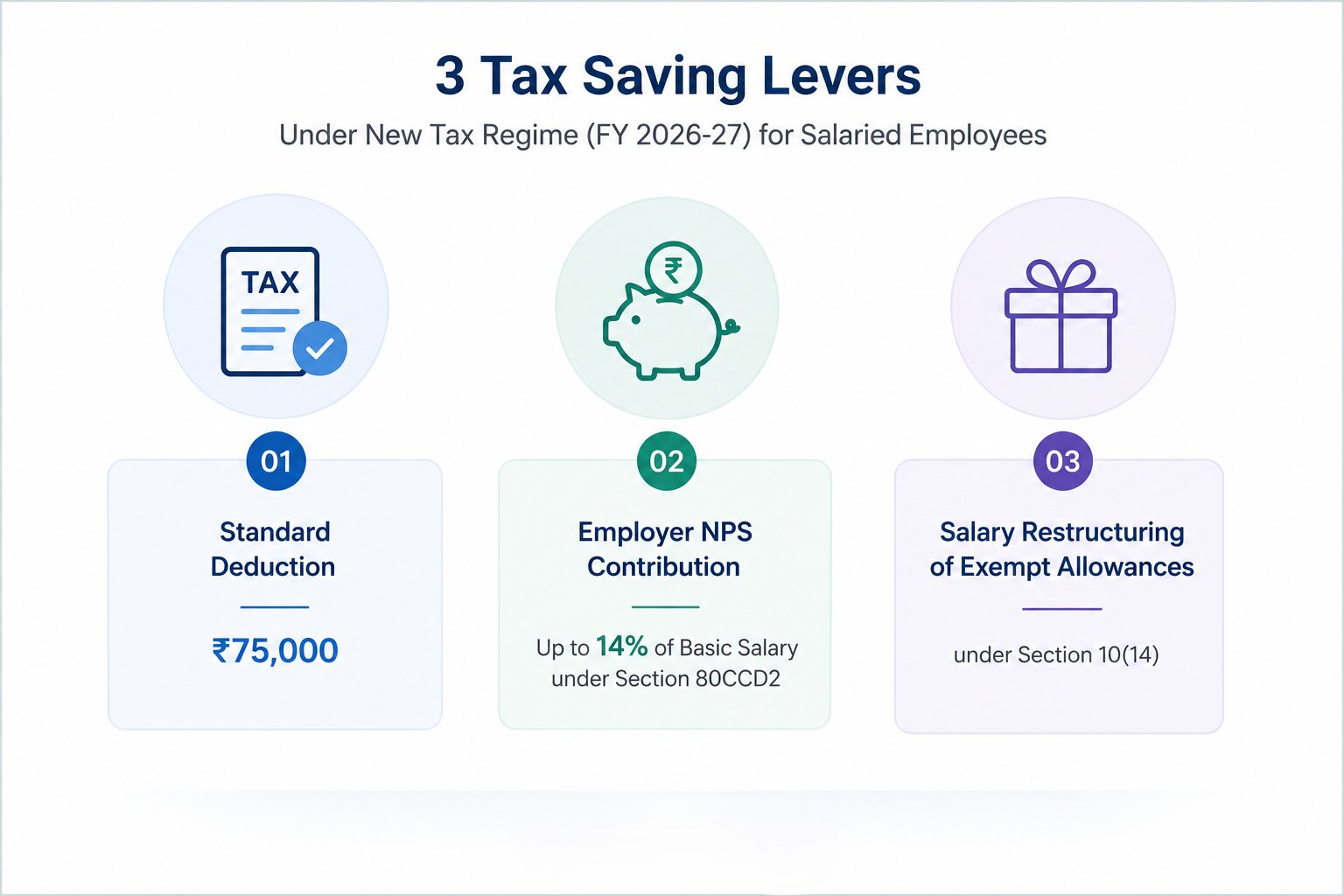

The new tax regime for FY 2026-27 gives every salaried individual two automatic benefits that do not require any action or investment:

1. Zero tax up to ₹12.75 lakh

The ₹75,000 standard deduction brings a ₹12.75 lakh gross salary down to ₹12 lakh taxable income. The Section 87A rebate of ₹60,000 then wipes out the entire tax liability on that ₹12 lakh. Budget 2026 confirmed no changes to these figures for FY 2026-27 — they continue unchanged from FY 2025-26. If your gross salary is at or below ₹12.75 lakh, your tax liability is zero under the new regime regardless of any investments or deductions, and you do not need to read further. File your ITR, declare the new regime, and you are done.

2. Lower slab rates above ₹12.75 lakh

Above ₹12.75 lakh, the new regime’s slab rates are meaningfully lower than the old regime’s — especially in the ₹12–24 lakh range where the old regime charged 20–30% and the new regime charges 15–25%. For someone whose total old-regime deductions are not large enough to bridge this rate gap, the new regime is simply cheaper even before any additional planning.

This is the core trade-off — explained in detail with worked examples at five salary levels in our guide to old vs new tax regime for FY 2026-27. The rest of this article assumes you have already established that the new regime is the right choice for you, and now want to know what further savings are available within it.

The deductions that still work in the new regime

Most Chapter VI-A deductions — 80C, 80D, 80TTA, 80G and others — are not available in the new regime. But a specific set of deductions and exemptions do survive. Here is the complete list with what each one actually means for your tax calculation:

| What survives | How much | What it means in practice |

| Standard deduction (salaried) | ₹75,000 | Automatic — no action needed. Reduces taxable salary by ₹75,000 before any other calculation. |

| Section 80CCD(2) — employer NPS contribution | Up to 14% of basic + DA | Your employer’s NPS contribution on your behalf — not your own. The single biggest active tax-saving lever in the new regime. Requires coordination with HR. |

| Section 80CCH — Agnipath scheme | Entire contribution exempt | Applicable only to Agniveer scheme participants. Not relevant for most private sector employees. |

| Home loan interest on let-out property | Actual interest paid | If you have rented out a property with a home loan, the interest is deductible even under the new regime. Self-occupied property interest (Section 24b) is NOT allowed. |

| Transport allowance for specially-abled | Actual amount | Applicable only to employees with disabilities — specific notification-based exemption. |

| Conveyance allowance for official duty | Actual amount | Reimbursements for official travel duty — not the same as conveyance for commuting. |

| Gratuity exemption (Section 10(10)) | Up to ₹20 lakh | Tax-free on retirement or departure — limits as per Payment of Gratuity Act. |

| Leave encashment (Section 10(10AA)) | Up to ₹25 lakh | Tax-free on retirement for government employees; for private sector, same limit applies. |

| VRS compensation (Section 10(10C)) | Up to ₹5 lakh | Voluntary Retirement Scheme — one-time exemption. |

| The one deduction that matters most for most salaried employees: Section 80CCD(2) Employer NPS contribution under 80CCD(2) is allowed in the new regime at up to 14% of your basic salary + DA. This is MORE generous than the old regime (which allowed only 10% of basic). It is also completely separate from your own NPS contributions, which are NOT deductible under the new regime. If your employer offers NPS as part of CTC and you have not opted into it, or if you have opted in but your employer is only contributing the minimum — this is the conversation to have with your HR team. |

How much Section 80CCD(2) actually saves — the numbers

This is the only meaningful active deduction available under the new regime for most private sector salaried employees. Its impact depends on your basic salary. Here is what it looks like at three salary levels, assuming the employer agrees to restructure the CTC to include a 14% NPS contribution (the maximum allowed):

| Gross salary | Basic salary (assume 40%) | Employer NPS at 14% of basic | Tax saving at 20% slab | Tax saving at 30% slab |

| ₹10,00,000 | ₹4,00,000 | ₹56,000/year | ₹11,200/year | ₹16,800/year |

| ₹15,00,000 | ₹6,00,000 | ₹84,000/year | ₹16,800/year | ₹25,200/year |

| ₹20,00,000 | ₹8,00,000 | ₹1,12,000/year | ₹22,400/year | ₹33,600/year |

| ₹30,00,000 | ₹12,00,000 | ₹1,68,000/year | Not applicable | ₹50,400/year |

At ₹20 lakh gross salary with a basic of ₹8 lakh, the employer NPS contribution saves approximately ₹33,600 per year in tax at the 30% slab — without requiring you to lock up any personal savings. The money goes into your NPS account and grows for retirement. For a full explanation of how NPS works and what your NPS corpus grows to over time, see our detailed guide on NPS: A Smart Way to Build Your Retirement Fund.

One important clarification: the employer NPS contribution comes out of your CTC — it reduces your in-hand salary by the same amount it saves in tax. Whether this is worthwhile depends on your liquidity needs. NPS funds are locked until retirement (with partial withdrawal allowed under specific conditions). This is informational context — the decision involves weighing tax saving against reduced monthly cash flow.

The lever most people miss: salary restructuring

This is the section that most articles on new regime tax saving skip. The reason is that it requires coordination with your employer rather than an individual investment decision — but for salaried employees, it often has a larger impact than any single deduction.

Under the new regime, most salary allowances are taxable. But a specific set of allowances and reimbursements are either fully or partially exempt under Section 10(14) of the Income Tax Act — and these exemptions survive in the new regime. They do not reduce the tax rate. They reduce the taxable income by changing how salary is classified.

What can be restructured

| Salary component | New regime treatment |

| Food/meal allowance | ₹50 per meal × 2 meals × 22 working days = ₹2,200/month (₹26,400/year) tax-free. Requires meal vouchers or cafeteria deduction through employer. |

| Mobile phone and internet reimbursement | Actual expense reimbursed against bills — fully exempt. Typically ₹1,500–₹2,500/month. |

| Books and periodicals allowance | Actual expense against bills — fully exempt. Relevant for professionals who read industry publications. |

| Vehicle maintenance / driver allowance (for higher grades) | Partially exempt under specific limits for official use. Requires documentation. |

| Uniform allowance | Actual cost of purchase and maintenance of uniform required for the job — exempt. |

| Gift from employer (non-cash) | Up to ₹5,000 per year — tax-free. Beyond this, treated as perquisite. |

The cumulative effect of restructuring even a few of these components can be meaningful. A ₹20 lakh CTC employee who restructures ₹26,400 in food allowance, ₹24,000 in phone/internet reimbursement, and ₹12,000 in books allowance into exempt components reduces their taxable income by ₹62,400 — saving approximately ₹18,720 per year at the 30% slab.

The key step: ask your HR whether the company’s payroll system allows CTC restructuring, and if so, which components are available. Many mid-to-large employers offer a flexible benefit plan where employees can allocate part of their CTC into exempt components. This is the conversation most salaried employees never initiate.

Image Source: AI

What does not reduce your tax in the new regime — even if you keep doing it

This is worth being explicit about because a large number of salaried employees in the new regime continue making investments under the assumption that they are saving tax. They are not — and the sooner this is understood, the better the investment decisions become.

- PPF contributions: PPF at 7.1% tax-free growth is still a strong savings instrument. But under the new regime, the contribution does not reduce your taxable income. You are investing for the tax-free compounding benefit, not for a current-year deduction. See our article on how compound interest works for the long-term case for PPF regardless of regime.

- ELSS mutual funds: The 3-year lock-in ELSS category exists for tax saving under Section 80C. Under the new regime, 80C does not apply. Continuing to invest in ELSS is fine if the fund’s performance merits it — but the tax-saving rationale for the lock-in disappears in the new regime.

- LIC and life insurance premiums: Premium paid under traditional endowment policies was often motivated by the 80C deduction. Under the new regime, this deduction is gone. The insurance coverage and maturity benefits may still have merit — but the tax-saving argument does not apply.

- Health insurance premiums: Section 80D (health insurance deduction) is not available in the new regime. Buy health insurance for the medical coverage it provides — not for tax saving. The cover amount should be driven by your healthcare needs, not the ₹25,000 deduction limit.

- Your own NPS contributions (Section 80CCD(1B)): The additional ₹50,000 NPS deduction under 80CCD(1B) is not available in the new regime. Only the employer’s contribution under 80CCD(2) survives. Voluntary NPS contributions are still sensible for retirement planning — just not for current-year tax reduction under the new regime.

What the actual tax saving looks like — three salary levels

Here is what a salaried employee on the new regime can achieve with optimal use of all available levers:

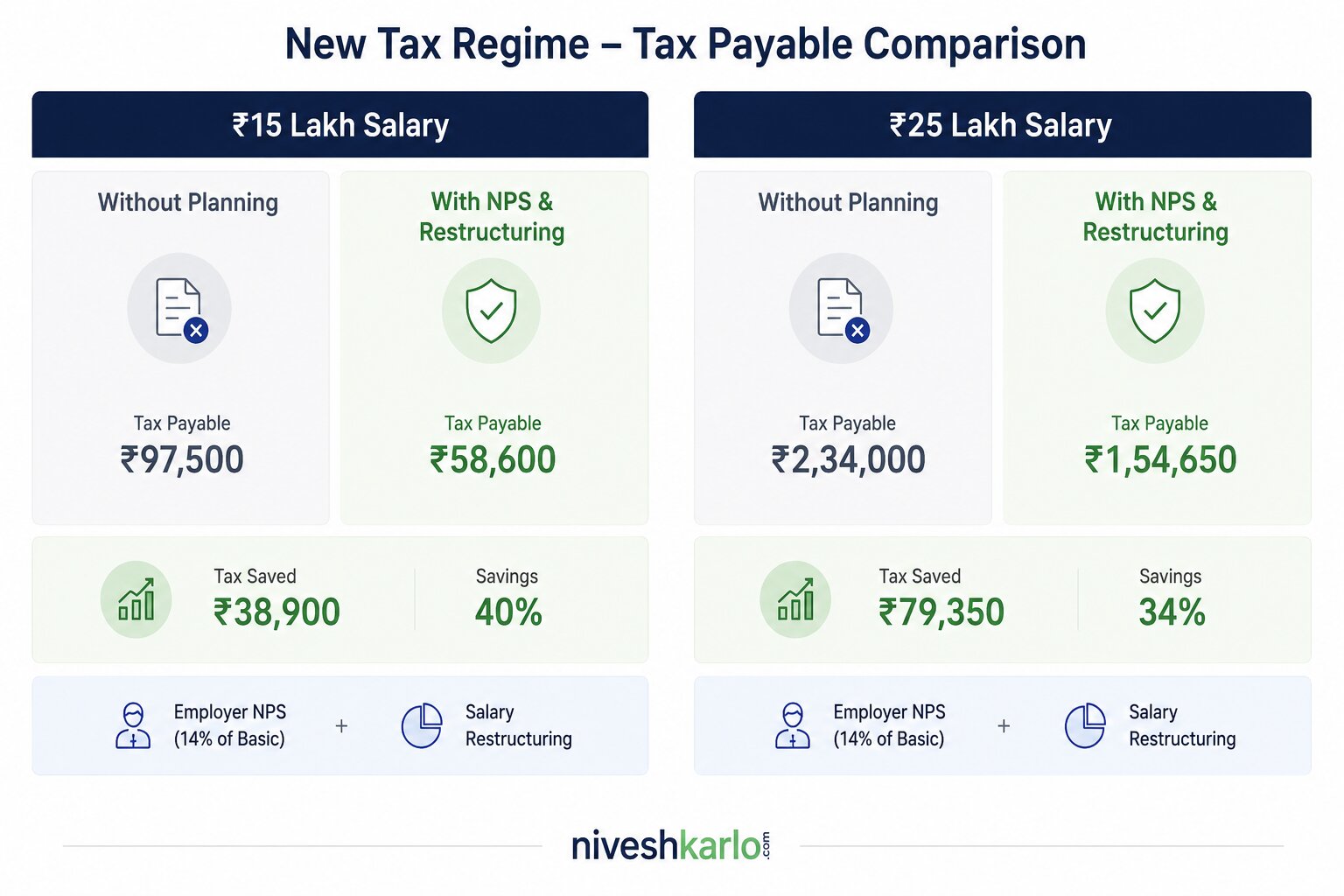

₹15 lakh gross salary — 30% of basic as employer NPS

| Gross salary: ₹15,00,000 Less: Standard deduction −₹75,000 Less: Employer NPS contribution (14% of ₹6L basic) −₹84,000 Less: Food allowance (₹2,200/month × 12) −₹26,400 Less: Mobile reimbursement (₹2,000/month × 12) −₹24,000 Taxable income: ₹13,90,600 Tax at new regime slabs: ₹1,33,590 4% cess: ₹5,344 Total tax payable: ₹1,38,934 Without any restructuring (only std deduction): ₹1,54,700 Tax saving from active levers: ₹15,766/year [Illustrative — actual figures depend on basic salary split and employer policies] |

₹25 lakh gross salary — full employer NPS + restructuring

| Gross salary: ₹25,00,000 Less: Standard deduction −₹75,000 Less: Employer NPS (14% of ₹10L basic) −₹1,40,000 Less: Food + mobile + books allowances −₹62,400 Taxable income: ₹22,22,600 Tax at new regime slabs: ₹4,33,780 4% cess: ₹17,351 Total tax payable: ₹4,51,131 Without any restructuring: ₹5,07,000 (approx.) Tax saving from active levers: ~₹56,000/year [Illustrative — employer NPS reduces in-hand pay by the same amount] |

Image Source: AI

If 80C is gone — where should your savings go?

This is the question most new-regime employees face after the first year: their March deadline pressure to make 80C investments disappears, their LIC agent calls asking them to renew the endowment policy, and they are not sure whether they should. The honest answer: without the 80C deduction, investment decisions should be made purely on financial merit rather than tax-saving compulsion. That can actually be a better outcome.

Without needing to hit ₹1.5 lakh in specific qualifying instruments, savings can go wherever the risk-return profile makes the most sense: an emergency fund first if one does not exist, then a mix of instruments suited to your time horizon and goals. A regular SIP in an index fund, a PPF account for the tax-free compounding even without the deduction, or a mix of debt and equity based on your risk tolerance — none of these require the 80C framework to make sense. The deduction was a reason to invest in specific instruments. Without it, the choice of instrument becomes freer.

Also Read: How To File Income Tax Return | How To Save Money From Salary

Questions about tax saving in the new regime

Can I claim 80C deductions if I am in the new tax regime?

No. Section 80C deductions — PPF, ELSS, LIC premium, ULIP, home loan principal, tuition fees, NSC, tax-saving FDs, and others — are not available under the new tax regime. The only deductions available are those listed in Section 115BAC of the Income Tax Act: standard deduction (₹75,000 for salaried), employer NPS contribution under 80CCD(2), and a specific set of Section 10 exemptions.

Is HRA exempt under the new tax regime?

No. House Rent Allowance exemption under Section 10(13A) is not available in the new tax regime. The entire HRA component of your salary is taxable. This is one of the most significant losses for employees in metro cities paying high rents — and is often a key reason why someone with large HRA claims is better off on the old regime.

My employer contributes to NPS. Does it save tax in the new regime?

Yes — this is the one deduction that works better in the new regime than the old. Employer NPS contribution under Section 80CCD(2) is deductible up to 14% of basic salary + DA in the new regime (versus only 10% in the old regime). If your employer contributes to NPS as part of your CTC, this deduction applies and reduces your taxable income. If your employer does not currently contribute to NPS or contributes less than 14%, it is worth asking HR whether this can be restructured. For more on how NPS works as a retirement savings tool, see our guide on NPS.

Can I switch back to the old regime next year if the new regime does not suit me?

Salaried employees with no business income can switch between regimes every financial year. The switch can be made at the time of filing your ITR — even if your employer deducted TDS under the new regime throughout the year. Any excess TDS will be refunded. To switch, declare the old regime at the time of filing. For more details on the ITR filing process, see our guide on how to file ITR for salaried individuals.

Does investing in mutual funds via SIP save tax in the new regime?

Investing in mutual funds via SIP does not save tax under the new regime — the ELSS category (which provided 80C deduction) is not allowed in the new regime. However, long-term capital gains from equity mutual funds held for more than one year are taxed at 12.5% on gains above ₹1.25 lakh per year — regardless of regime. This is not a tax saving per se, but it is the tax cost to understand before redeeming. The investment decision to continue SIPs should be based on their wealth-building merits, not tax saving.

What is the break-even deduction level where old regime is better?

This varies by salary level — our detailed comparison at old vs new tax regime for FY 2026-27 shows the break-even at each salary level with worked examples. The broad principle: if your total old-regime deductions (80C + 80D + HRA + home loan interest) exceed approximately ₹3.75 lakh at ₹15 lakh salary, or ₹4.5 lakh at ₹20 lakh salary, the old regime saves more. Below those thresholds, the new regime is cheaper — even before any NPS or restructuring.

Disclaimer: This article is for educational and informational purposes only. It does not constitute tax advice. All deduction rules and slab rates are based on incometax.gov.in and verified sources as of June 22, 2026. Budget 2026 confirmed no changes to FY 2026-27 slab rates or deduction rules. Tax laws are subject to change. Worked examples are illustrative — actual tax liability depends on individual income composition, employer policies, and specific circumstances. Please consult a qualified Chartered Accountant for advice specific to your situation. NiveshKarlo does not recommend any specific tax-saving instrument or investment.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.