ELSS vs PPF vs FD: Which Tax-Saving Option Is Best?

All three give you the same ₹1.5 lakh deduction under Section 80C. What they do with your money after that is where the real difference lies — and it is not the headline interest rate that matters most.

Transparency: AI-assisted draft reviewed by the NiveshKarlo team. PPF rate, ELSS lock-in rules, FD rates, and tax treatment verified July01, 2026. Informational only — not investment advice. This article applies only to the old tax regime, where 80C deductions are available.

Three investments. The same ₹1.5 lakh deduction under Section 80C. And almost nothing else in common.

ELSS, PPF, and tax-saver FD get compared constantly — but most comparisons stop at the headline rate: ELSS returns 13%, PPF returns 7.1%, FD returns 7%. On that basis, ELSS looks like the obvious winner and FD looks barely worth the trouble. That comparison is misleading, because it ignores what happens to each return after tax — and after tax, the gap between PPF and a tax-saver FD is much larger than the headline rates suggest, even though their pre-tax rates look almost identical.

This article works through what actually survives in your pocket from each instrument — not just what each one advertises.

Start here: PPF’s 7.1% and a tax-saver FD’s 7% are not the same number

Here is the comparison most articles skip entirely. On paper, PPF and a tax-saver FD look like close cousins — both government-adjacent, both low-risk, rates a fraction of a point apart. They are not close once tax is applied, because PPF’s return is entirely tax-free while FD interest is taxed at your full income slab rate.

| Headline rate | Tax on returns | Effective post-tax return (30% slab) | |

| PPF | 7.1% | 0% — fully exempt (EEE) | 7.1% |

| Tax-saver FD | 7.0% | 30% — taxed at slab rate | 4.9% |

| ELSS | ~13% (long-term average, not guaranteed) | 12.5% LTCG above ₹1.25L/year gains | ~11.5% (approx., after typical LTCG) |

For someone in the 30% tax slab, a tax-saver FD’s effective post-tax return drops to approximately 4.9% — meaningfully below PPF’s 7.1%, even though the headline rates looked almost the same. This is the single most important number in this comparison, and it is the one most FD-vs-PPF articles never calculate explicitly.

ELSS’s tax treatment is also more favourable than FD’s: long-term capital gains above ₹1.25 lakh in a financial year are taxed at 12.5% — far below the 30% slab rate applied to FD interest. Even after accounting for this tax, ELSS’s post-tax return remains the highest of the three, primarily because its pre-tax return is structurally higher due to equity exposure — not because of a tax advantage alone.

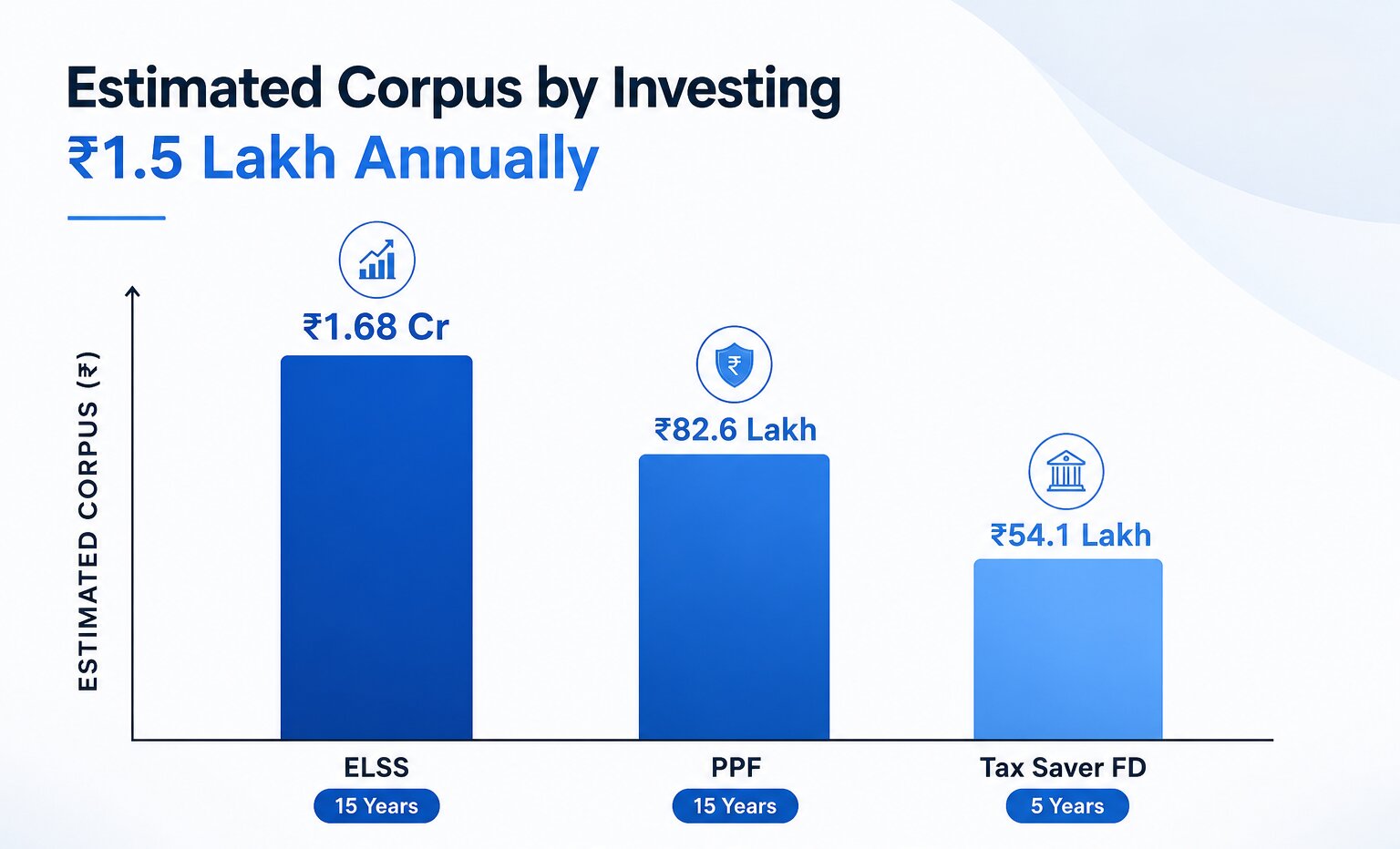

What ₹1.5 lakh, invested every year, actually becomes

Numbers in isolation are hard to act on. Here is what an annual ₹1.5 lakh investment — the full 80C limit — produces over each instrument’s natural holding period.

PPF — ₹1.5 lakh/year for 15 years (full lock-in)

| Total invested: ₹22,50,000 Maturity value (7.1%): ~₹40,68,000 Tax-free gain: ~₹18,18,000 Entirely risk-free, government-guaranteed, fully tax-exempt at every stage. |

ELSS — ₹1.5 lakh/year for 15 years (held well beyond the 3-year lock-in)

| Total invested: ₹22,50,000 Estimated value at ~13% CAGR: ~₹74,00,000 (illustrative — not guaranteed) Estimated gain: ~₹51,50,000 (before LTCG tax) Market-linked — could be meaningfully higher or lower depending on market conditions over the period. The 3-year lock-in is a minimum, not a recommended holding period — ELSS is most effective when held well beyond it. |

Tax-saver FD — ₹1.5 lakh/year for 5 years (mandatory lock-in)

| Total invested (5 years): ₹7,50,000 Maturity value (~7%): ~₹8,86,000 Gain before tax: ~₹1,36,000 Tax on interest at 30% slab: ~₹40,800 Effective post-tax gain: ~₹95,200 Shortest commitment in rupee terms here is misleading — most investors renew the FD or treat it as a recurring annual commitment, similar to PPF and ELSS. |

Image Source: AI

Risk and liquidity — the part the returns table doesn’t show

A higher number on paper does not automatically make an instrument the right choice. Risk tolerance and liquidity needs matter as much as the return calculation.

| Risk level | Liquidity | |

| PPF | None — sovereign guarantee, principal and interest both protected | Locked 15 years; partial withdrawal from year 7; loan from year 3 |

| ELSS | Market risk — value can fall, especially in the short term | Locked 3 years per instalment; no early exit even in emergencies |

| Tax-saver FD | Low — bank deposit, but not sovereign-guaranteed like PPF | Locked 5 years; no premature withdrawal under any circumstances |

None of these three should be treated as an emergency fund — all three involve a lock-in that makes them unsuitable for money you might need on short notice. An emergency fund in a liquid, accessible instrument should exist separately, before allocating money to any of these three for tax saving.

One caveat before going further: this entire comparison applies only to the old tax regime. Under the new tax regime, Section 80C gives no deduction at all — PPF and ELSS keep their underlying tax treatment, but neither reduces taxable income. A tax-saver FD loses its only reason to exist over a regular FD once the deduction disappears. On the new regime, this becomes a pure investment decision, not a tax-saving one.

Questions people ask when comparing 80C options

Can I invest in all three — ELSS, PPF, and tax-saver FD — in the same year?

Yes, you can split your contributions across all three. However, the combined deduction across all 80C-eligible instruments — including EPF, life insurance premiums, and home loan principal repayment if applicable — is capped at ₹1.5 lakh per financial year. Investing ₹50,000 each in PPF, ELSS, and a tax-saver FD still only gives you a ₹1.5 lakh deduction in total, not three separate deductions.

Which has the shortest lock-in — ELSS, PPF, or tax-saver FD?

ELSS has the shortest lock-in at 3 years. PPF requires 15 years for full maturity (though partial withdrawal is allowed from year 7). Tax-saver FD requires a mandatory 5 years with no premature withdrawal option, making it stricter than PPF’s partial withdrawal flexibility despite the shorter headline period.

Is ELSS riskier than a regular SIP in an equity mutual fund?

No — ELSS funds invest in the same kind of equity portfolio as a regular equity mutual fund. The risk profile is similar; the difference is the 3-year lock-in and the 80C tax deduction, neither of which changes the underlying market risk. For a broader understanding of how mutual funds and SIPs work, see our guides on what is SIP in mutual funds and the power of SIP over time.

Can I withdraw from PPF before 15 years if I have an emergency?

Partial withdrawal is allowed from the 7th financial year onward, capped at 50% of the balance at the end of the 4th preceding year or the immediately preceding year, whichever is lower. A loan against the PPF balance is available between the 3rd and 6th year. Before year 7, no withdrawal option exists at all — which is why PPF should never be the primary destination for money that might be needed within the first 6-7 years.

Does a tax-saver FD allow premature withdrawal in a medical emergency?

No. Unlike a regular fixed deposit, a tax-saver FD’s 5-year lock-in is strictly enforced with no premature withdrawal provision — not even for medical emergencies. This is a meaningful difference from a regular FD, which typically allows premature withdrawal with a penalty. This rigidity is a frequently overlooked drawback of tax-saver FDs.

Is PPF or ELSS better for retirement planning?

Both can play a role, and many long-term investors use both. PPF’s guaranteed, tax-free return makes it a stable foundation for retirement savings, particularly for the portion of a portfolio meant to be risk-free. ELSS, with equity exposure, has historically offered higher growth potential over very long horizons (15-20+ years), which suits the portion of retirement savings that can tolerate market volatility in exchange for higher expected returns. For retirement-specific planning beyond 80C instruments, see our guide on how compound interest works to understand the long-term mechanics that make early, consistent investing effective regardless of instrument.

So which one should I actually pick?

It depends on what the ₹1.5 lakh is meant to do. If the priority is capital preservation and zero risk, PPF wins on post-tax return without any market exposure. If the priority is long-term growth and a 10+ year horizon, ELSS has historically produced the highest post-tax outcome of the three, with the shortest lock-in. A tax-saver FD is mainly useful for splitting an allocation across instruments or wanting a shorter horizon than PPF without equity exposure — on pure post-tax return, it is the weakest option for anyone above the lowest tax slabs. Many investors split the limit rather than choosing one — a common pattern cited by planners is roughly 60% toward PPF for the guaranteed floor and 40% toward ELSS via SIP for growth, adjusted based on individual risk tolerance and time horizon.

The one calculation worth doing before you choose

Before deciding between these three, calculate your own post-tax effective return at your specific tax slab — not the headline rate. A 7% FD rate at the 30% slab becomes roughly 4.9% in your pocket. A 7.1% PPF rate stays 7.1%. That gap, more than any qualitative description of risk appetite, is the number that should drive the decision for anyone choosing between PPF and a tax-saver FD specifically.

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment or tax advice. PPF rate (7.1% p.a.) is as of Q1 FY 2026-27 and is revised quarterly by the Ministry of Finance — verify the current rate before investing. ELSS returns are illustrative based on historical category averages and are not guaranteed; mutual fund investments are subject to market risk. Tax-saver FD rates vary by bank and are subject to change. All post-tax calculations are illustrative examples at the 30% tax slab and will differ at other income levels. This comparison applies to the old tax regime only — Section 80C deductions are not available under the new tax regime. NiveshKarlo does not recommend any specific fund, bank, or instrument. Please consult a SEBI-registered investment advisor or Chartered Accountant before making investment or tax decisions.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.