How to Increase Your SIP Amount Over Time

Every year your salary goes up. For most people, their SIP does not. This is what happens when it does — followed through one career, including the years it could not.

Transparency: AI-assisted draft reviewed by the NiveshKarlo team. All step-up SIP mechanics and corpus figures were live-verified on June14, 2026. Informational only — not investment advice.

In April 2026, Priya — 26 years old, two years into her first job — got her annual appraisal letter. Her salary went from ₹7.2 lakh to ₹8.1 lakh. A 12.5% hike. She felt good about it. She updated her resume’s CTC line, told her parents, and treated herself to dinner.

Her SIP — ₹5,000 a month, started when she got her first job — stayed exactly the same. It had stayed the same for two years, and it would stay the same for the next several, because nobody had ever told her it didn’t have to.

This is the story of what happens to Priya’s SIP over the next 20 years under two different versions of her life — one where the ₹5,000 never changes, and one where it grows every year the way her salary does. The second version includes two years where she could not increase it at all. That part matters, because it is the part most articles about step-up SIPs leave out.

What nobody told Priya when she started her SIP

When Priya set up her SIP through her mutual fund app in 2024, the form asked for an amount, a date, and a fund. It did not ask: ‘What is your salary likely to do over the next 20 years?’ It did not need to — a SIP is just a standing instruction. Set it once, and it runs unchanged until you log back in and change it.

This is the quiet design flaw in how most people use SIPs. The instrument itself — Systematic Investment Plan — has no opinion about your career. It will happily debit ₹5,000 from an account that, ten years later, receives a salary five times larger than it did when the SIP started. The amount is frozen at the moment of setup, while everything else about the investor’s financial life keeps moving.

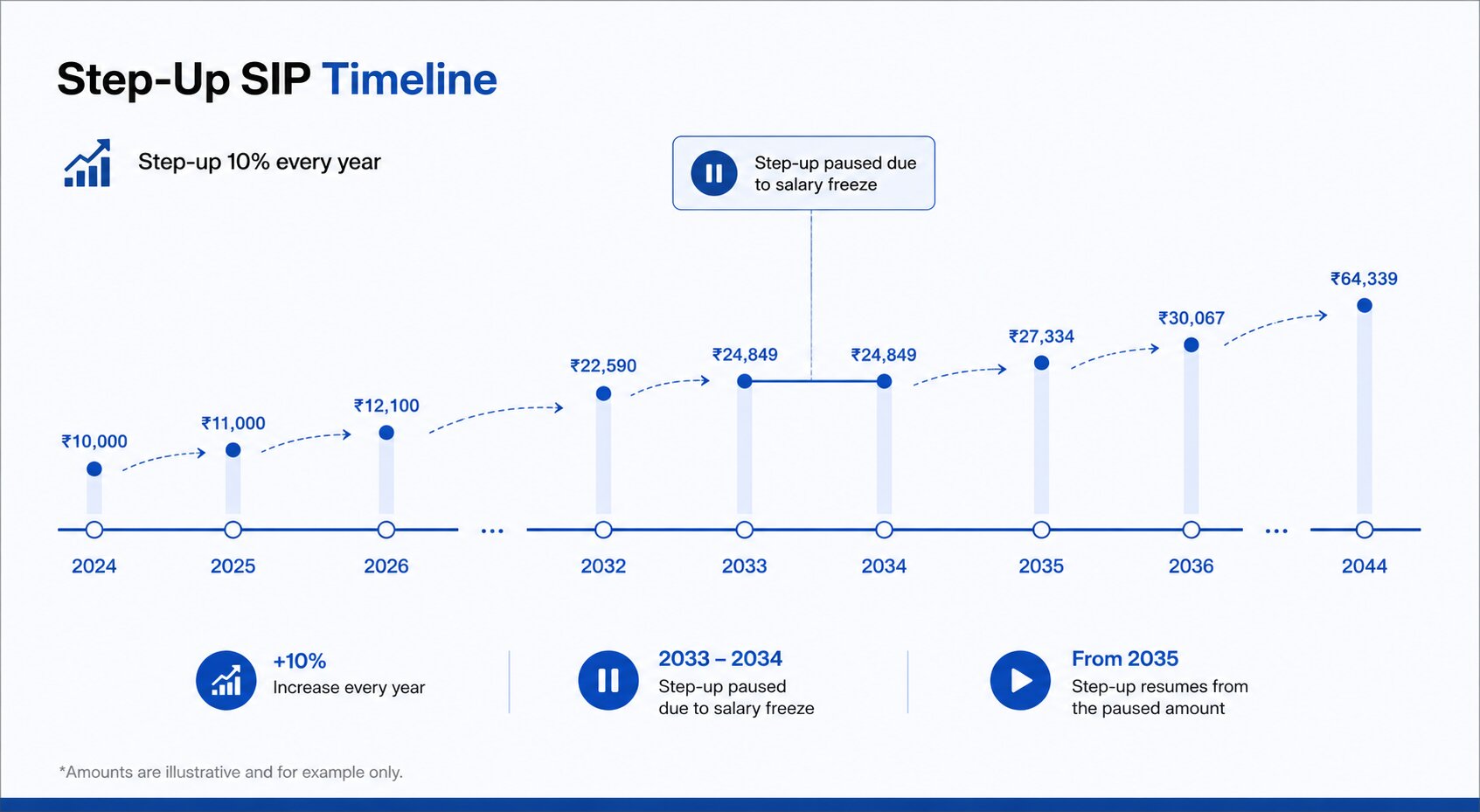

Most mutual fund platforms in India — Zerodha, Groww, and the AMC apps directly — have a feature for exactly this. It is called a step-up SIP, or sometimes a top-up SIP. It does one simple thing: increases your SIP amount automatically by a fixed percentage, once a year, on a date you choose. Priya’s app had this option the entire time. She had never opened that screen.

Years 1 to 5: the difference is small enough to ignore — which is the problem

Suppose Priya had discovered the step-up option in 2024 and set it to increase her SIP by 10% every year — roughly in line with her typical annual increment. Here is what her monthly SIP amount would look like over the first five years, compared to leaving it at ₹5,000:

| Year | Flat SIP (₹/month) | Step-up SIP at 10% (₹/month) |

| 2024 (start) | 5,000 | 5,000 |

| 2025 | 5,000 | 5,500 |

| 2026 | 5,000 | 6,050 |

| 2027 | 5,000 | 6,655 |

| 2028 | 5,000 | 7,321 |

By 2028, the step-up version is investing ₹2,321 more per month than the flat version — about ₹27,800 more for that year alone. In isolation, this looks like a modest adjustment. Most people, looking at this table, would shrug. The difference over five years feels too small to bother changing a standing instruction for.

This is exactly why almost nobody does it. The benefit of stepping up is invisible in years 1 through 5. It becomes visible only when those early increases have had 15 more years to compound — which is precisely the period that has not happened yet when someone is deciding whether it’s worth the effort.

Years 9 and 10: the part every step-up SIP article skips

In 2033, Priya is 33. Her company goes through a restructuring. There is no increment that year — in fact, there is a brief pay cut before things stabilise. In 2034, salaries are frozen company-wide as the business recovers.

If a step-up SIP were a rigid commitment — an automatic 10% increase that simply happens whether or not it can be afforded — this would be the moment it breaks. Priya’s bank balance that year cannot support a SIP that is 21% larger than it was two years ago on top of a smaller paycheque.

| What actually happens in this situation: Step-up SIPs in India are not contractual obligations. They are standing instructions that can be paused, reduced, or skipped for any given year through the same app screen used to set them up. Most AMCs explicitly allow this. Priya’s options in 2033 and 2034: — Skip the step-up for those two years (SIP stays at the 2032 amount) — Reduce the step-up percentage for those years only (e.g. 0% instead of 10%) — Pause the SIP entirely if the situation is severe (not the first choice — see our article on what happens to your SIP during a market fall for why continuity matters) Priya chooses the first option. Her SIP amount freezes at the 2032 level for two years, then resumes its 10% annual step-up from 2035 onward — calculated from where it left off, not from the original 2024 base. |

This flexibility is what makes step-up SIPs realistic rather than aspirational. One calculator analysis notes this explicitly — if income does not increase in a specific year, the SIP simply doesn’t increase for that period either. The strategy survives two flat years without falling apart, because it was never a single irreversible decision. It is twenty small decisions, most of which Priya will never have to think about because the app handles them automatically — except in the years she chooses to intervene.

Year 20: what the gap actually looks like

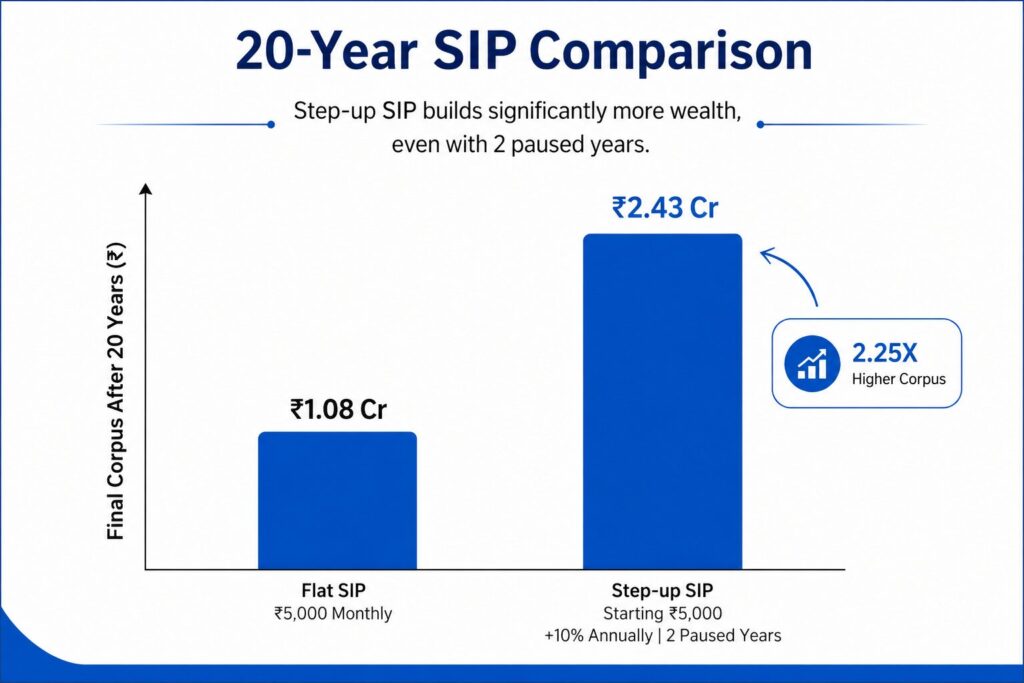

By 2044, Priya is 46. Her flat ₹5,000 SIP has been running for 20 years. Her step-up SIP — which paused for two years in 2033-34 and otherwise increased 10% annually — has also been running for 20 years, but at a monthly amount that reached over ₹28,000 by the final year. Using a 12% CAGR assumption (the same conservative figure used in our article on the power of SIP over time), here is what the two paths produce:

| Flat ₹5,000/month SIP (20 years) | Step-up SIP, 10% (20 years, 2 paused) | |

| Total amount invested | ₹12,00,000 | ₹26,84,000 (approx.) |

| Estimated corpus at 12% CAGR | ₹49,96,000 | ₹83,40,000 (approx.) |

| Gain over invested amount | ₹37,96,000 (3.2×) | ₹56,56,000 (2.1×) |

Two things are worth sitting with here. First, the step-up version produces a corpus roughly 67% larger — even after accounting for two years where Priya could not increase her contribution at all. This aligns with the 40-60% larger corpus typically cited for step-up SIPs, on the higher end here because the step-up percentage (10%) and duration (20 years) compound significantly.

Second — and this is the part that surprises people — the gain multiple is actually lower for the step-up SIP (2.1× versus 3.2×). This is not a flaw. It happens because a larger share of the step-up corpus is recently-invested money that has had less time to compound. The flat SIP’s early ₹5,000 instalments have had the full 20 years to grow; the step-up SIP’s later, larger instalments (₹20,000+, ₹25,000+) have had only a few years. The step-up SIP wins on absolute corpus despite a lower multiplier — because the absolute amounts being multiplied are so much larger in the later years.

So how much should the step-up actually be?

Priya used 10% because it roughly matched her typical annual increment — a 5-10% annual increase is the range most commonly cited as aligning with standard salary increments in India. But this is a starting point, not a rule. The honest answer is that the step-up percentage should track something real in your life — your actual increment, your inflation-adjusted expense growth, or a fixed amount you decide you can comfortably add each year.

A few ways people in Priya’s position think about the number:

- Match it to your increment, with a lag. If your increment is announced in April and takes effect immediately, but you don’t actually feel the extra money until your next salary credit, set the step-up date a month or two after the increment date — so the step-up uses money you’ve already adjusted to having.

- Step up by a fixed rupee amount instead of a percentage. Some platforms allow this. Increasing by ₹1,000 every year is simpler to reason about than a percentage, and avoids the step-up becoming uncomfortably large in later years if salary growth slows but the percentage doesn’t.

- Step up only the portion above what you need to live on. If a ₹70,000 raise (post-tax, annualised) arrives and the actual cost-of-living increase that year is ₹40,000, the remaining ₹30,000 — roughly ₹2,500/month — is a natural step-up amount. This keeps the increase tied to genuine surplus rather than an arbitrary percentage.

Whatever the number, the step-up should never come before an emergency fund is in place and any high-interest debt is under control. A step-up SIP increases the fixed monthly outflow — which means it also increases the financial strain if income becomes irregular. Priya’s 2033-34 pause worked smoothly because her emergency fund covered the gap without forcing a SIP disruption.

Setting it up takes less time than reading this sentence will

Most AMCs and platforms in India — Zerodha, Groww, and the major fund houses directly — offer a built-in step-up or top-up facility at the time of setting up a SIP, or as a modification to an existing one. The screen typically asks for two things: the percentage (or amount) to increase by, and the frequency (almost always annual). Some platforms also ask for a cap — a maximum SIP amount beyond which the step-up stops, useful if the increase should level off after a certain point.

For an existing SIP — like Priya’s two-year-old ₹5,000 SIP — the step-up is usually added as a modification, not a new SIP. The existing SIP continues; the step-up instruction is layered on top of it, taking effect from the next applicable cycle (commonly the SIP’s anniversary date).

Also Read: The Power of SIP: How Your Money Grows Over Time | Savings Account vs Fixed Deposit: Which Is Better for You?

Questions that come up once you’ve decided to do this

Is a step-up SIP a separate product from a regular SIP?

No. It is the same SIP, with an additional instruction attached that increases the amount on a schedule. The underlying mutual fund, folio, and units are identical to a regular SIP — the only difference is the monthly debit amount changes over time according to the step-up rule chosen.

Can the step-up be removed later if circumstances change?

Yes. The step-up instruction can be modified or cancelled at any time without affecting the underlying SIP or the units already accumulated. If removed, the SIP continues at whatever amount it had reached at the time of removal — it does not revert to the original starting amount.

What happens if the step-up amount becomes larger than affordable in a given month?

If there are insufficient funds on the debit date, that month’s instalment simply fails — similar to any SIP. No penalty is charged by the AMC for a failed instalment, though banks may charge a small fee for insufficient balance (typically ₹0-500 depending on the bank). If this happens repeatedly, reducing the step-up percentage is preferable to letting instalments fail repeatedly, since failed instalments mean missed unit purchases.

Does the step-up percentage compound on the previous year’s amount or the original amount?

It compounds on the previous year’s amount — this is what makes it a percentage increase rather than a flat addition. A 10% step-up on a ₹5,000 SIP makes year 2 equal to ₹5,500, year 3 equal to ₹6,050 (10% of ₹5,500, not 10% of ₹5,000), and so on. This is the same compounding logic explained in our article on how compound interest works, applied to the contribution amount rather than the returns.

Should an existing SIP be stepped up, or should a new SIP be started alongside it?

Either works, and the end result is mathematically similar. Adding a step-up to an existing SIP is operationally simpler — one folio, one set of statements, one place to track. Starting a new SIP alongside an existing flat one gives more granular control if the incremental amount should go to a different fund — for example, if the original SIP is in a large-cap fund and the step-up portion should go into a different category. For guidance on evaluating funds for this kind of allocation, see our guide on how to analyse a mutual fund.

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice. The example of ‘Priya’ is illustrative and fictional, created to explain the mechanics of step-up SIPs. All corpus projections use a 12% CAGR assumption for illustration and are not guarantees — mutual fund returns are market-linked and can be higher or lower. Past performance is not indicative of future results. NiveshKarlo does not endorse any specific mutual fund, platform, or step-up percentage. Please consult a SEBI-registered investment advisor for guidance specific to your situation.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.