What Are Mutual Funds? A Plain Guide for New Investors

A mutual fund pools money from thousands of investors and uses it to buy a diversified mix of assets. Here is what that actually means, how it works, and what you need to know before you start.

Transparency: AI-assisted rewrite reviewed by the NiveshKarlo team. All AMFI figures updated from official May 2026 data. SEBI fund categories referenced from the SEBI circular on Categorisation and Rationalisation of Mutual Fund Schemes (October 2017). Informational only — not investment advice.

The mutual fund industry in India manages ₹81.58 lakh crore in assets as of May 2026 — up from ₹13.82 lakh crore just ten years ago. That is a 6x increase in a decade. There are now 27.66 crore mutual fund folios in the country, and 9.64 crore active SIP accounts contributing monthly. This is no longer a niche product for sophisticated investors. It is where a significant portion of household savings is going.

Yet for someone encountering mutual funds for the first time, the basic question — what exactly is a mutual fund and how does it work — often gets answered with either jargon-heavy explanations or oversimplifications that leave out the parts that actually matter. This article is an attempt at a plain, complete answer.

What a mutual fund actually is

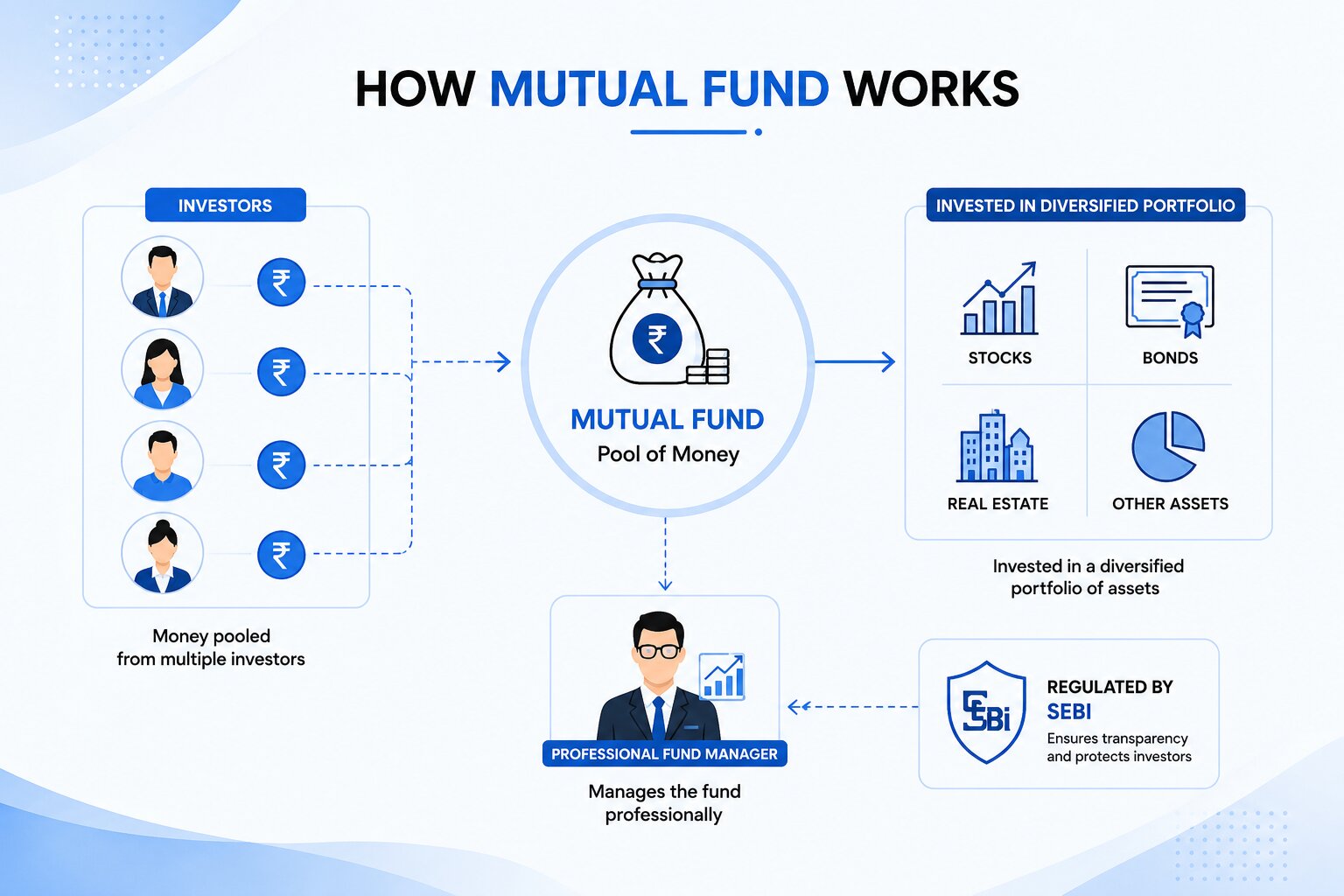

A mutual fund is a financial vehicle that pools money from many investors — sometimes thousands of them — and uses that combined capital to invest in a portfolio of assets. Each investor in the fund owns a proportional share of that portfolio, in the form of units.

The portfolio is managed by a professional fund manager employed by an Asset Management Company (AMC) — a firm registered and regulated by SEBI (Securities and Exchange Board of India). The fund manager decides which stocks, bonds, or other assets to buy and sell, based on the fund’s stated investment objective.

The value of your investment changes daily, because the underlying assets — shares, bonds — change in value every day. This daily value per unit is called the Net Asset Value, or NAV. When NAV goes up, your investment is worth more. When it falls, it is worth less. At any point, you can buy more units at the current NAV or redeem (sell) your units at the current NAV.

For a detailed explanation of how NAV is calculated and what it tells you, see our guide on what NAV means in mutual funds.

Why mutual funds exist — the problem they solve

Imagine you have ₹5,000 to invest this month. On your own, that amount buys you a handful of shares of one or two companies — which means your money is entirely dependent on how those specific companies perform. If one of them has a bad quarter, your investment suffers.

A mutual fund solves this by aggregating your ₹5,000 with thousands of other investors’ contributions. The combined pool is large enough to be invested across dozens or hundreds of different securities. Your ₹5,000 now effectively owns a small slice of all of them. This diversification means no single company’s bad performance significantly damages your overall investment.

The second problem mutual funds solve is expertise. Researching and selecting stocks or bonds well requires time, access to data, and financial knowledge that most people don’t have or don’t want to develop. A professional fund manager — whose full-time job this is — makes those decisions on behalf of all investors in the fund.

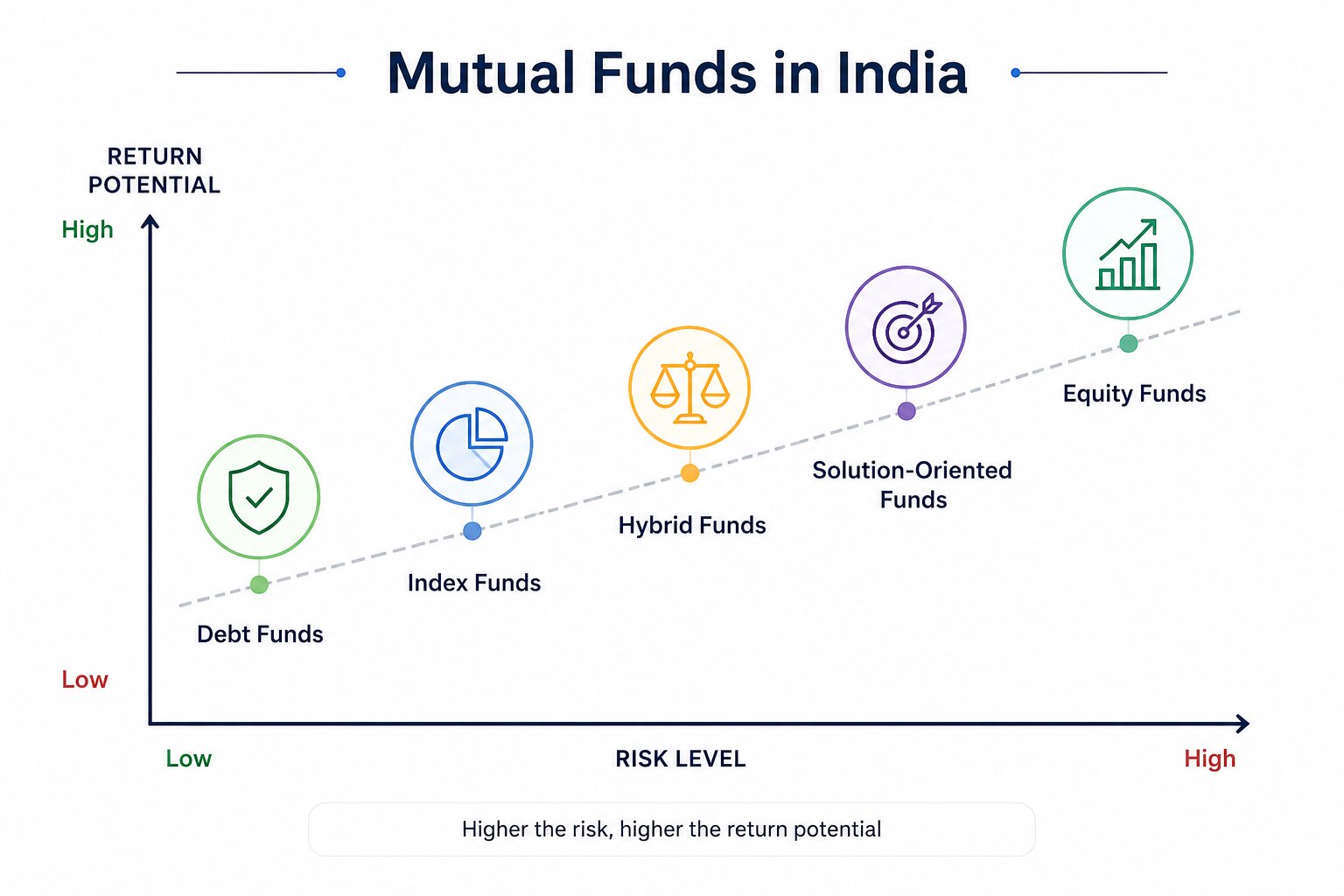

The five categories of mutual funds — as defined by SEBI

In October 2017, SEBI issued a circular on the categorisation and rationalisation of mutual fund schemes. This standardised how AMCs could classify their funds into five broad categories. Understanding these categories is the starting point for deciding which type of fund suits your goal.

1. Equity funds

Equity funds invest primarily in stocks. Their goal is capital growth — meaning the value of your investment is expected to grow over time, though it will fluctuate with the stock market. These are further classified by SEBI into sub-categories based on the market capitalisation of the companies they invest in: large-cap (top 100 companies by market cap), mid-cap (101st to 250th), small-cap (251st and below), flexi-cap (no restriction), and others. See our comparison of debt vs equity mutual funds for a fuller picture of how these differ in risk and return profile.

2. Debt funds

Debt funds invest in fixed-income instruments — government bonds, corporate bonds, treasury bills, and similar securities. They are generally more stable in value than equity funds because bond prices don’t fluctuate as dramatically as stock prices. They are used for goals with shorter time horizons, or by investors who want lower volatility. They are not risk-free — bond prices do change, and credit risk (the risk of a bond issuer defaulting) exists.

3. Hybrid funds

Hybrid funds invest in a mix of equity and debt in varying proportions. An aggressive hybrid fund might hold 65–80% in equity and the rest in debt; a conservative hybrid does the reverse. The mix varies by sub-category and provides a middle ground between the growth potential of equity and the relative stability of debt.

4. Solution-oriented funds

These are funds designed for specific financial goals — retirement and children’s education are the two SEBI-defined sub-categories. They come with a lock-in period of at least five years, which encourages investors to stay invested for the duration needed to meet the goal.

5. Other funds (index funds, ETFs, and fund of funds)

This category includes index funds — funds that passively track a market index like the Nifty 50 or Sensex rather than having a fund manager actively pick stocks — and Exchange Traded Funds (ETFs), which work similarly but trade on the stock exchange like shares. Index funds and ETFs typically have significantly lower expense ratios than actively managed funds. The Nifty 50 has delivered approximately 12–13% CAGR over the past 10 years — which is the benchmark that actively managed large-cap funds aim to beat.

How a SIP fits into this picture

A Systematic Investment Plan (SIP) is not a type of mutual fund — it is a method of investing in one. Instead of putting in a lump sum, you invest a fixed amount every month automatically. The amount buys units at whatever the NAV is on that date. When NAV is lower (market is down), you buy more units. When NAV is higher, you buy fewer. Over time, this averages out your cost per unit — a mechanism called Rupee Cost Averaging.

The practical effect is that you do not need to time the market or accumulate a large sum before starting. AMFI data for May 2026 shows 9.64 crore SIP accounts contributing ₹30,953 crore every month — demonstrating how widely this approach has been adopted. For the full explanation of how SIP investing grows over time, see our guide on the power of SIP over time, which includes corpus tables for different monthly amounts and time horizons.

What a mutual fund costs you — expense ratio and exit load

Two costs matter when investing in mutual funds. Most people understand returns but overlook costs. Over long periods, the difference between a 0.1% and a 1.5% annual expense ratio on the same underlying portfolio compounds into a significant rupee difference.

Expense ratio

The expense ratio is the annual fee charged by the AMC for managing the fund, expressed as a percentage of your investment. It is deducted from the fund’s returns — meaning the NAV you see already accounts for it. You do not pay it separately. A fund with an expense ratio of 1.5% takes ₹1,500 per year on every ₹1 lakh invested. SEBI has set maximum limits on expense ratios by fund category. Index funds and ETFs typically have expense ratios between 0.05% and 0.5% — significantly lower than actively managed equity funds, which can range from 1% to 2.5%.

Exit load

An exit load is a fee charged when you redeem your units within a specified time period — typically within 1 year for equity funds. The most common exit load structure is 1% if redeemed within 12 months, and nil after that. The purpose is to discourage short-term trading in a fund designed for long-term investing. Before investing in any fund, check its exit load and ensure your investment horizon is longer than the exit load period.

What can go wrong — understanding the risks

Mutual funds are not bank deposits. They are not guaranteed by any government body. All mutual fund investments carry risk, and understanding what kind of risk applies to which type of fund is essential before choosing one. Our full guide on understanding mutual fund risk covers this in detail, but the key risks are:

- Market risk: The value of equity fund units can fall when the stock market falls. This is the primary risk for equity fund investors and is the reason these funds are recommended only for goals that are at least 5 years away.

- Credit risk: For debt funds, there is a risk that a bond issuer defaults on its obligations — reducing the fund’s NAV. Higher-yielding debt funds typically carry higher credit risk.

- Interest rate risk: Debt fund NAVs also fluctuate with interest rate changes. When interest rates rise, existing bond prices fall, and the NAV of debt funds holding those bonds drops. Longer-duration debt funds are more sensitive to this.

- Inflation risk: Parking money in very low-yield instruments — like liquid funds or savings accounts — means inflation erodes real returns over time. This is the risk of being too conservative for your actual time horizon.

Direct plans vs regular plans — a difference most beginners miss

Every mutual fund in India is available in two versions: a direct plan and a regular plan. They invest in exactly the same portfolio, managed by the same fund manager. The only difference is cost.

A regular plan is bought through a distributor or agent — the AMC pays the distributor a commission, which is embedded in a slightly higher expense ratio. A direct plan is bought directly from the AMC (or through platforms that offer direct plans) — no distributor, no commission, lower expense ratio.

Over a 10- or 15-year investment horizon, the difference in expense ratio between a direct and regular plan of the same fund can result in a meaningfully larger corpus in the direct plan. This is worth understanding before you choose where to invest.

How to actually start investing in mutual funds

The process is simpler than it was five years ago. Most investors today start through a mutual fund app or platform, complete a KYC (Know Your Customer) process digitally, and begin a SIP within a single session.

- Complete KYC: This is a one-time process required by SEBI. You will need your PAN, Aadhaar, and a photograph. Most platforms do this online in under 10 minutes.

- Choose a fund: Start with the fund’s investment objective, category, and expense ratio. For beginners, a large-cap index fund or flexi-cap fund is a commonly chosen starting point — though this is informational context, not a recommendation.

- Decide lump sum or SIP: If you are investing for a long-term goal and have a regular income, a SIP is the more practical approach. If you have a surplus to deploy immediately, a lump sum is an option.

- Start small if needed: Most funds allow SIPs from ₹500 per month. Starting with a small amount, getting comfortable with how NAV moves, and increasing the amount over time is a reasonable approach.

For a step-by-step guide to starting your first SIP, see how to start a SIP investment. For guidance on evaluating a fund before investing, see how to analyse a mutual fund before investing.

One important point before you begin: mutual fund investing is more effective when you already have an emergency fund in place. An emergency fund in a liquid, accessible account means you never need to redeem mutual fund units at a loss during a personal cash crunch.

Questions new investors ask

Are mutual funds safe?

Mutual funds are regulated by SEBI and all AMCs must be registered with SEBI. Your money is held in a separate trust structure — it cannot be used by the AMC for its own purposes. However, ‘safe’ in mutual funds means something different from ‘safe’ in a bank deposit. Equity fund values fluctuate with markets. Debt fund values can fall if interest rates rise or if a bond issuer defaults. Understanding the specific risks of the fund you choose is more useful than a blanket ‘safe or unsafe’ assessment.

What is the minimum amount to invest in a mutual fund?

Most mutual fund SIPs start at ₹500 per month. The Chhoti SIP category allows ₹250 per month. Lump sum investments typically require a minimum of ₹1,000 or ₹5,000 depending on the fund. There is no maximum.

How long should I stay invested in a mutual fund?

It depends on the type of fund and your goal. Equity funds are typically recommended for goals at least 5 years away — because short-term market volatility can result in negative returns over 1-2 year periods, while longer holding periods have historically smoothed out this volatility. Debt funds and liquid funds are more appropriate for shorter time horizons — 1 to 3 years.

What is the difference between a mutual fund and a SIP?

A mutual fund is the investment product. A SIP is a method of investing in it — through fixed, regular contributions rather than a lump sum. You can invest in the same mutual fund either way. Most people use SIPs because it suits a regular salary income, avoids the need to time the market, and allows starting with small amounts. See our full explanation of how SIP works in mutual funds.

Do mutual funds pay dividends?

Some mutual funds have an ‘IDCW’ (Income Distribution cum Capital Withdrawal) option, previously called the dividend option. Under this option, the fund periodically pays out a portion of its gains to investors rather than reinvesting them. However, these payouts reduce the NAV of the fund and are taxed as income in the year they are received. For most long-term investors, the growth option — where gains are reinvested — is more tax-efficient.

How are mutual fund gains taxed?

Mutual fund taxation depends on the type of fund and the holding period. For equity funds, gains held for more than one year are Long-Term Capital Gains (LTCG) — taxed at 12.5% above ₹1.25 lakh per year. Gains on equity funds held for less than a year are Short-Term Capital Gains (STCG) — taxed at 20%. Debt fund gains are added to your income and taxed at your applicable slab rate, regardless of holding period.

Where to go from here

A mutual fund is a starting point, not a destination. Once you understand what a fund is and how it works, the next questions are: which category suits your goal, how to evaluate a specific fund before investing, and how to build a habit of regular investing. Those questions are covered in depth across NiveshKarlo — including how to analyse a mutual fund before investing, the difference between debt and equity funds, and what index funds are and how they work.

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice or a recommendation to invest in any mutual fund, category, or scheme. All AMFI figures are from the official May 2026 data published June 10, 2026. SEBI fund categories are as per SEBI’s Categorisation and Rationalisation of Mutual Fund Schemes circular (October 2017). Mutual fund investments are subject to market risk — please read all scheme-related documents carefully. Past performance is not a guarantee of future returns. Please consult a SEBI-registered investment advisor before making any investment decisions.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.