How to File ITR for Salaried Individuals: FY 2025-26 Guide

FY 2025-26 (AY 2026-27) · Last date: July 31, 2026 · ITR-1 and ITR-2 filing is live

Which form to use, what documents to keep ready, and how to file step by step — without jargon.

Transparency: AI-assisted draft reviewed by the NiveshKarlo team. All deadlines, forms, and tax rules verified on June 13, 2026 from incometax.gov.in and CBDT. Informational only — not tax advice.

| IMPORTANT — FILING DEADLINES FOR FY 2025-26 (AY 2026-27) July 31, 2026 → Last date for salaried individuals (ITR-1 and ITR-2) August 31, 2026 → ITR-3 and ITR-4 (non-audit business/profession cases) December 31, 2026 → Belated return (late fee under Section 234F applies) March 31, 2027 → Revised return (to correct errors in a filed return) Filing on time = faster refund + no interest + no penalty + carry-forward of losses. |

Every year between April and July, the same question circulates across offices, WhatsApp groups, and family dinners: “Have you filed your ITR yet?” For most salaried employees, ITR filing feels more complicated than it actually is. The Income Tax e-filing portal has become genuinely more user-friendly over the last few years — pre-filled data from Form 26AS, the Annual Information Statement (AIS), and your employer’s TDS means most of the numbers are already there when you log in. What trips people up is not the filing itself but the decisions that come before it: which form to use, which regime to pick, which deductions to claim.

This guide answers all of those — in order — for a salaried individual filing for FY 2025-26 (AY 2026-27).

Step 1: Pick the right ITR form — this is where most people go wrong

Filing the wrong ITR form means your return is treated as defective by the Income Tax Department. You will get a notice asking you to refile. The form you need depends on your income sources — not your income level.

| ITR Form | Who should file it | Who should NOT use it |

| ITR-1 (Sahaj) | Salaried income + one house property + income from other sources (FD interest, savings interest) + agricultural income up to ₹5,000. Total income up to ₹50 lakh. | Directors of companies, anyone holding unlisted shares, those with capital gains, income above ₹50 lakh, more than one house property, or foreign assets. |

| ITR-2 | Salaried income + capital gains (mutual funds, stocks, property) + more than one house property + foreign assets + income above ₹50 lakh + NRIs. | Anyone with business or professional income — use ITR-3. |

| ITR-3 | Salaried income + income from business or profession. Also for those with presumptive business income (Section 44ADA, 44AE) if not choosing ITR-4. | Not for those with only salary and no business income. |

| ITR-4 (Sugam) | Presumptive business income under Section 44AD/44ADA/44AE + salary + one house property. Total income up to ₹50 lakh. | Directors, those with foreign income, capital gains above basic exemption. |

For most salaried employees with no business income or complex capital gains, ITR-1 is the right form. If you have redeemed mutual funds or sold stocks during FY 2025-26, you will need ITR-2. When in doubt, ITR-2 is the safer choice — it covers more scenarios than ITR-1 and is not significantly more complex to file.

Step 2: Keep these documents ready before you log in

Having these ready before you open the portal saves significant time. Most of the data in your ITR is pre-filled — but you need to verify it against your own records.

Documents you will need

- Form 16 (Part A and Part B): Issued by your employer by June 15 each year. Part A shows TDS deducted and deposited. Part B shows your salary breakup and deductions. If you changed jobs during the year, collect Form 16 from each employer.

- Form 26AS: Your consolidated tax credit statement. Available on the income tax portal. Shows all TDS deducted on your PAN — by employer, bank (FD interest), and others.

- Annual Information Statement (AIS): More detailed than Form 26AS. Covers salary, interest income, dividends, mutual fund transactions, property purchases, and more. Download from the portal and compare with your records. Discrepancies should be flagged before filing.

- Taxpayer Information Statement (TIS): A summarised version of AIS. Use this as a quick cross-check.

- Bank interest certificates: From all savings accounts and FDs. Even interest below the TDS threshold is taxable income and must be declared.

- Investment proofs for deductions: 80C (PPF passbook, ELSS statements, LIC receipts, EPF passbook), 80D (health insurance premium receipt), 80G (donation receipts with 10BE certificate if applicable).

- Home loan statement: If claiming Section 24(b) interest deduction — up to ₹2 lakh for self-occupied property in the old regime.

- Capital gains statement: If you redeemed mutual funds or sold shares — download from your broker or platform. Required for ITR-2 only.

| One important check before filing: Download your AIS and compare it with your Form 26AS and your own records. If any income is shown in AIS that you did not earn, raise a feedback on the portal before filing — do not ignore it. If any income is missing from AIS but you earned it, declare it anyway. The AIS does not override your obligation to report all income. |

Step 3: Decide your tax regime — old or new

The new tax regime is the default for FY 2025-26. If you do nothing, you are on the new regime. If you want to opt for the old regime, you must actively declare it — either to your employer at the start of the year (for TDS purposes) or while filing your ITR.

Salaried individuals with no business income can switch between regimes every year. This means even if your employer deducted TDS under the new regime, you can switch to the old regime at filing time if it saves you more tax — and claim a refund on the excess TDS. For a detailed breakdown of which regime saves more at each salary level, see our guide on the old vs new tax regime for FY 2025-26.

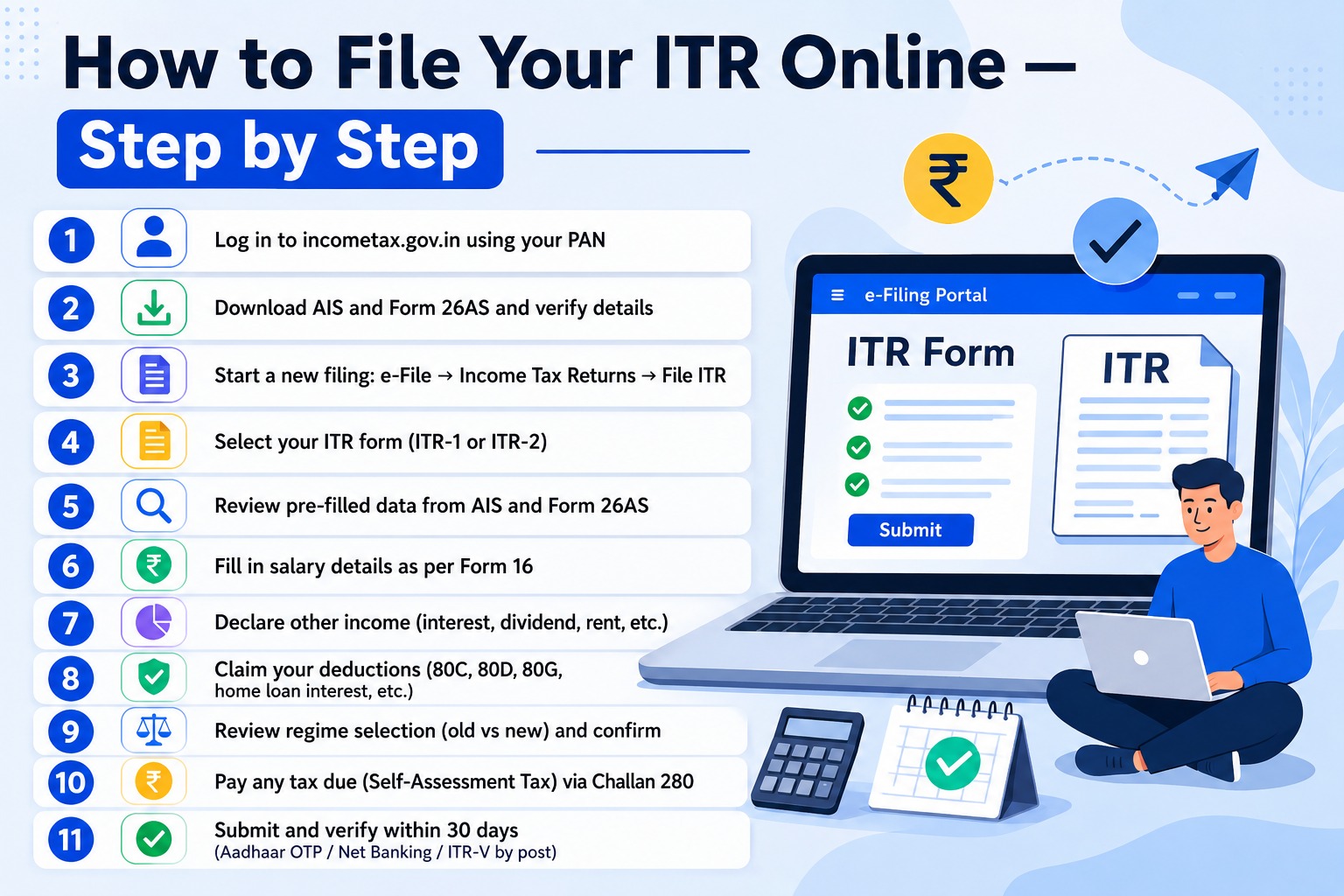

Step 4: How to file your ITR online — step by step

The income tax e-filing portal (incometax.gov.in) is the official platform. ITR-1 and ITR-2 for AY 2026-27 are live as of May 2026. Here is the process from login to verification.

- Log in to incometax.gov.in using your PAN as user ID, and your password. If you have not registered, use your PAN to register — you will need your Aadhaar linked to PAN for OTP verification.

- Download AIS and Form 26AS before you start filling your form. Go to ‘Annual Information Statement’ under the ‘e-File’ menu. Compare with your Form 16 and bank statements. Note any discrepancies.

- Start a new filing — go to ‘e-File’ → ‘Income Tax Returns’ → ‘File Income Tax Return’. Select Assessment Year 2026-27. Choose ‘Online’ mode for the simplest experience.

- Select your ITR form — ITR-1 for most salaried employees, ITR-2 if you have capital gains or income above ₹50 lakh. The portal may suggest a form based on your pre-filled data.

- Review pre-filled data — your name, PAN, address, employer details, and TDS information will already be populated from your AIS and Form 26AS. Verify each field against your Form 16.

- Fill in salary details — enter salary as per Form 16 Part B: basic salary, HRA, allowances, perquisites, and deductions allowed by employer. Do not leave any component blank.

- Declare other income — savings account interest (even below ₹10,000), FD interest, dividend income, rental income if any. These are pre-filled from AIS but must be verified and confirmed.

- Claim your deductions — enter 80C, 80D, 80G, home loan interest (24b), HRA exemption, and any other deductions applicable to your situation and chosen regime.

- Review regime selection — the portal will now calculate your tax under both regimes and highlight which one results in lower tax. Confirm your choice.

- Pay any tax due (Self-Assessment Tax) — if your tax liability exceeds TDS already deducted, pay the balance using Challan 280 before submitting. The portal will prompt you if there is a shortfall.

- Submit and verify — after submitting, verify within 30 days using Aadhaar OTP (fastest), net banking EVC, or by sending ITR-V to CPC Bengaluru by post. An unverified return is treated as not filed.

Image Source: AI

What changed in AY 2026-27 that affects salaried filers

A few specific changes from the Income Tax Department apply to returns filed for FY 2025-26 (AY 2026-27). These are worth knowing before you file.

| Change | What it means for you |

| Two house properties can now be treated as self-occupied | Previously only one property could be self-occupied if you owned two and could not occupy both. From AY 2026-27, both can be self-occupied — useful if you own two properties and live in neither due to work location. |

| Capital gains: pre/post July 23 2024 split removed | Last year, capital gains had to be split based on whether the transaction was before or after July 23, 2024 (when LTCG/STCG rates changed). This split is no longer required in AY 2026-27 — single reporting applies. |

| New Income Tax Act 2025 does NOT apply yet | The new Income Tax Act 2025 came into force from April 1, 2026 but applies only to Tax Year 2026-27 (returns filed in 2027). AY 2026-27 returns are still governed by the Income Tax Act 1961. |

| ITR-1 now allows two house properties | From AY 2026-27, ITR-1 allows reporting of two house properties (previously only one). If you own two houses but no capital gains or foreign assets, you may still qualify for ITR-1. |

| 80G donation deductions: PAN of political party required | If claiming 80GGC (donation to political party), you must now provide the PAN of the political party in your ITR. |

Common mistakes salaried employees make while filing

- Not verifying AIS before filing. If AIS shows income you did not earn (common with dividend or interest mismatches), file an AIS feedback first. If you ignore it and the ITR contradicts AIS, you may receive a scrutiny notice.

- Missing interest income. Savings account interest, FD interest, and RD interest are all taxable. Even if TDS was not deducted (below the threshold), the income must be declared. Banks report all interest to AIS.

- Not declaring income from previous employer. If you changed jobs, you must collect Form 16 from both employers and combine the salary figures. Filing based on only one employer’s Form 16 is a common error that leads to notices.

- Wrong bank account for refund. Pre-validate your bank account on the portal before filing. An unvalidated account delays refunds significantly.

- Not verifying the return after submission. A submitted but unverified return is treated as not filed. Verify within 30 days using Aadhaar OTP — it takes under 2 minutes.

- Filing ITR-1 when ITR-2 is required. If you redeemed any mutual funds, sold shares, or have capital gains of any amount — even small — you need ITR-2. Filing ITR-1 in this case makes your return defective.

- Forgetting to claim 80TTA deduction. If you are in the old regime, savings account interest up to ₹10,000 is deductible under Section 80TTA. Many salaried employees forget to claim this.

Refunds, late filing, and what happens if you miss July 31

If your total TDS deducted (from salary, FD interest, or any other source) exceeds your actual tax liability, you are entitled to a refund. Refunds are processed by the Centralised Processing Centre (CPC) and typically credited within 15–45 days of a verified return for straightforward cases. Filing earlier in the season — April or May — generally results in faster refunds than filing in the last week of July.

| Scenario | What applies |

| Filed on time (by July 31, 2026) | No late fee. Full ability to carry forward losses. Normal refund processing. |

| Belated return (August 1 – December 31, 2026) | Late fee: ₹5,000 under Section 234F (₹1,000 if total income is below ₹5 lakh). Interest under Section 234A on unpaid tax. Cannot carry forward most capital losses. |

| Revised return (any time up to March 31, 2027) | Can be filed if you discover an error in an already filed return. No penalty for revising — you can revise as many times as needed before March 31, 2027. |

| Not filing at all | Notice from Income Tax Department under Section 142(1). Possible penalty under Section 270A. Tax demand with interest under Sections 234A, 234B, 234C. |

Image Source: AI

Also Read : Good Debt vs Bad Debt: What You Need to Know | Emergency Fund: How Much Is Enough?

Questions salaried employees ask every filing season

Is it mandatory for salaried employees to file ITR?

Yes, if your gross total income before deductions exceeds the basic exemption limit — ₹3 lakh under the new regime or ₹2.5 lakh under the old regime. Even if your employer has deducted all TDS and your tax liability is zero, filing is mandatory if your income exceeds these limits. Filing is also mandatory if you want to claim a refund, carry forward capital losses, or apply for certain loans or visas. Check the complete list of mandatory filing conditions on incometax.gov.in.

Can I file ITR without Form 16?

Yes. Form 16 is a convenience, not a mandatory prerequisite. If your employer has not issued Form 16 by the time you want to file, you can use your salary slips, AIS, and Form 26AS to reconstruct the income and TDS figures. The AIS in particular has become comprehensive enough to file without Form 16 for straightforward cases.

I switched jobs during FY 2025-26. What do I do?

Collect Form 16 from both employers. Add the salary figures from both, along with TDS from both. Your total income is the combined salary from both employers for the full year. A common mistake is filing based on only one employer’s Form 16 — this understates your income and leads to a tax demand notice later.

Do I need to declare FD interest if TDS was already deducted?

Yes. TDS deducted by the bank is an advance payment of tax, not a final settlement. You must still declare the gross FD interest as income in your ITR. The TDS already deducted will be shown as a credit in your return and offset against your final tax liability. If TDS exceeds your actual tax on that income, you get a refund. See our guide on Savings Account vs FD for how FD interest is taxed in detail.

What is the difference between Form 26AS and AIS?

Form 26AS is a consolidated tax credit statement — it shows TDS deducted on your PAN by various deductors (employer, banks, others), advance tax paid, and self-assessment tax paid. The AIS is a broader statement that additionally includes purchases, sale of property, mutual fund transactions, dividends, foreign remittances, and other financial information. Before filing, download both and verify against your records. AIS is the more complete of the two.

Can I change my tax regime while filing ITR?

Yes. Salaried employees with no business income can choose their regime at the time of filing, regardless of what regime they declared to their employer during the year. If you switch to the old regime and it saves you more tax, any excess TDS deducted by your employer (who used the new regime) will be returned as a refund. The portal will show you the tax under both regimes side by side. For a full comparison at your salary level, see our old vs new tax regime guide.

What is Section 234F and how much is the late filing penalty?

Section 234F charges a late filing fee if you file after July 31. The fee is ₹5,000 if filed between August 1 and December 31, 2026. If your total income is below ₹5 lakh, the maximum fee is ₹1,000. This is separate from the interest under Section 234A charged on any unpaid tax liability. Filing before July 31 avoids both.

Disclaimer: This article is for educational and informational purposes only and does not constitute tax advice. All deadlines, forms, and rules are based on verified information as of May 23, 2026 from incometax.gov.in and CBDT. Tax laws are subject to change and CBDT may issue notifications extending deadlines — always verify the current deadline on the official income tax portal before filing. NiveshKarlo does not recommend any specific tax filing platform or service. Please consult a qualified Chartered Accountant for advice specific to your situation.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.