Good Debt vs Bad Debt: What You Need to Know

Some debt builds your life. Some quietly empties your wallet. The difference is not which loan you took — it is what the money did after you borrowed it.

Transparency: AI-assisted draft reviewed by the NiveshKarlo team. All interest rates live-verified June 9, 2026. Informational only — not financial advice.

Debt has a reputation problem in India. Most people either fear all of it or treat it too casually. The fear side avoids home loans and ends up renting for decades when buying would have made more financial sense. The casual side swipes a credit card for a phone upgrade and spends the next year paying 36% interest on a gadget that lost half its value the moment it was unboxed.

The truth is simpler than either extreme. Debt is a tool. Like any tool, what matters is whether you are using it to build something or just spending it. A home loan at 9% that gives you an asset appreciating at 6–8% annually is a fundamentally different instrument from a personal loan at 18% taken to fund a vacation. Understanding this distinction — not as theory but as ₹ and paise — is what this article is about.

RBI data shows India’s household debt reached 41.3% of GDP by March 2025, driven primarily by consumption-oriented retail loans. That is not inherently bad — but it does mean more households are carrying debt than ever before, and not all of it is working in their favour.

What makes debt ‘good’ or ‘bad’

These labels are imprecise — no debt is unconditionally good, and even expensive debt can be justified in a genuine emergency. But as a working framework, here is the distinction that actually holds up in practice.

Good debt is borrowed money that either creates an asset, generates income, or saves you more money than it costs you. A home loan is the clearest example: the EMI replaces rent, the property appreciates, and you build equity over time. An education loan that results in a meaningfully higher salary is another. Even a business loan that generates returns above its interest cost qualifies.

Bad debt is borrowed money spent on things that depreciate, disappear, or deliver no financial return. Credit card debt rolled over at 36–42% annually to fund lifestyle spending. A personal loan taken for a wedding that costs more in interest than the celebration was worth. Buy-now-pay-later used for daily expenses. The defining characteristic is not the type of loan — it is that the money is gone, and what remains is only the repayment obligation.

The line gets blurry in the middle. A car loan at 9% for a vehicle you genuinely need for work is different from a car loan at 12% for an upgrade from a perfectly functional existing car. A personal loan to consolidate four high-interest credit card balances into one lower-rate repayment plan is arguably good debt doing the work of clearing bad debt. Context always matters.

The credit card debt trap — and why 60% of cardholders are in it

Credit card debt is the most expensive form of debt available to retail borrowers. Monthly interest rates range from 2.5% to 3.75% — which translates to 30% to 45% annually. For context: a fixed deposit pays you roughly 6.5% per year. A credit card charges you up to 45% per year. The gap between those two numbers is where financial lives quietly fall apart.

RBI data cited by PL Wealth Management shows only 40% of credit card holders repay their full outstanding amount every month. The other 60% carry a revolving balance — and that balance compounds at those 30–45% annual rates. CRIF High Mark data shows credit card delinquencies in the 91–360 day overdue category rose 44.3% year-on-year, from ₹23,476 crore in March 2024 to ₹33,887 crore in March 2025.

What minimum-due payment actually costs you

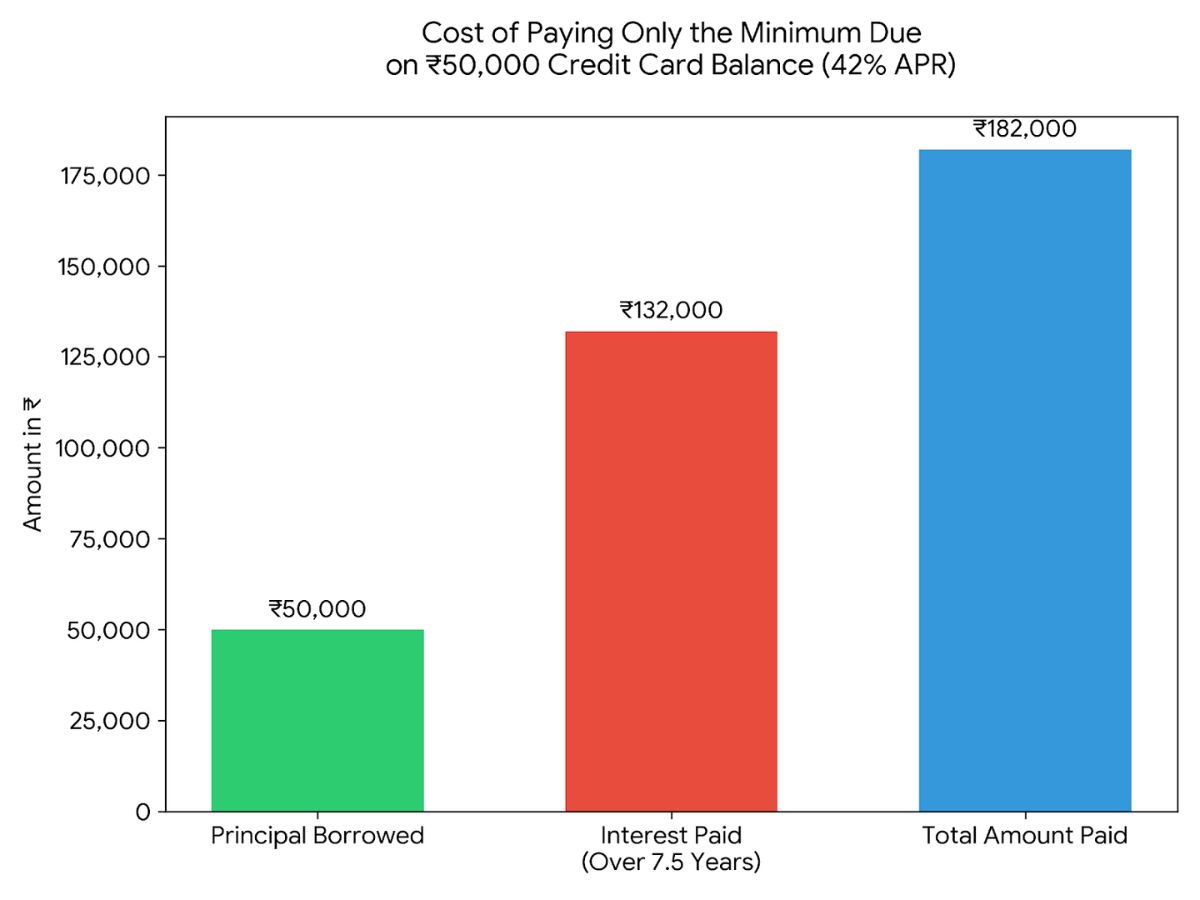

This is the number most credit card users have never calculated. Banks are required to show the minimum due — usually 5% of the outstanding balance or ₹100–200, whichever is higher. Paying only the minimum feels manageable. What it does to your balance is not.

| Example: ₹50,000 credit card outstanding at 3.5% monthly interest (42% p.a.) Minimum due (5%): ₹2,500 per month Interest charged (3.5%): ₹1,750 that month Amount actually reducing the principal: ₹750 At this rate, paying only the minimum, it takes approximately 7.5 years to clear ₹50,000. Total interest paid over that period: ~₹1,32,000 You paid ₹1,32,000 in interest on ₹50,000 borrowed — 2.6 times the original amount. This is not an edge case. This is what minimum-due payment does arithmetically. |

The trap deepens because credit limits increase automatically with good payment history. A ₹50,000 limit becomes ₹1,00,000, spending adjusts upward, and the revolving balance grows. By the time the problem is visible, the outstanding may be ₹2–3 lakh with monthly interest charges of ₹7,000–10,500 — amounts that exceed what many people can pay in full each month.

The solution is not to avoid credit cards entirely. A card used correctly — full outstanding cleared every month, within 30% of the credit limit — is a free 45-day loan and a useful tool for tracking expenses. The danger is treating available credit as available money. It is not. It is borrowed money at the most expensive rate available to retail borrowers.

Personal loans: when they make sense and when they don’t

Personal loan rates range from 9.99% p.a. at the best private banks (HDFC, ICICI, Axis, IndusInd as of May 2026) to 24% or more for NBFCs and fintech lenders, depending on your CIBIL score, employer profile, and income. The rate you are offered is not the headline rate — it is the rate calculated after your risk profile is assessed.

A personal loan at 12–14% is not inherently bad. It becomes bad when the purpose is consumption that delivers no financial return — a destination wedding, an international holiday, an electronics upgrade. The interest compounds through your monthly EMIs, and the experience or product is gone long before the loan is paid off.

A personal loan is arguably justified when:

- It consolidates higher-interest debt — for example, clearing ₹80,000 in credit card debt at 40% with a personal loan at 13%, reducing your effective interest rate by more than half

- It covers a genuine emergency where no alternative exists and the cost of not having the money is higher than the interest

- It bridges a short, specific gap — a known expense in 3 months that you will have the cash for, where the personal loan avoids disrupting investments

What it is not justified for: aspirational lifestyle spending that can be deferred. India’s household debt growth is being driven primarily by unsecured consumption loans — personal loans and credit cards used for spending rather than investing. The RBI’s Financial Stability Report has flagged this trend as a concern precisely because these loans carry no collateral and no asset on the other side.

What good debt actually looks like

Home loans

A home loan at 8.5–9.5% p.a. (indicative, May 2026) is the most commonly cited example of good debt — but only under specific conditions. The property must be one you intend to live in or rent out. The EMI must be within 35–40% of your take-home income so it does not crowd out other financial goals. And you should have already built an emergency fund before committing to a long-tenure EMI, because missing a home loan EMI has consequences — penalty interest and a CIBIL score hit — that missing a SIP contribution does not.

The home loan interest deduction under Section 24(b) — up to ₹2 lakh annually for self-occupied property — reduces the effective cost of borrowing for those in the old tax regime. For someone in the 30% slab, a 9% home loan effectively costs about 6.3% after the tax benefit. That matters when evaluating whether to prepay aggressively or continue investing via SIP — in many scenarios, the investment return over a long horizon can exceed the effective post-tax loan cost.

Education loans

An education loan is good debt when the degree or skill it funds produces a measurable salary increase. The question to ask before taking one is not just the interest rate — it is what the incremental income from the education will be and whether that increment, even conservatively estimated, exceeds the total repayment cost. Education loans also carry Section 80E deductions — interest paid is fully deductible under the old tax regime for up to 8 years, with no upper limit.

Business loans

A business loan is good debt when the business generates returns above the loan’s interest cost — and when the business plan is grounded enough to make that outcome probable rather than aspirational. The risk here is higher than with home loans because business income is variable. The same loan that makes sense when revenue is strong can become unmanageable when a client delays payment or a slow quarter hits.

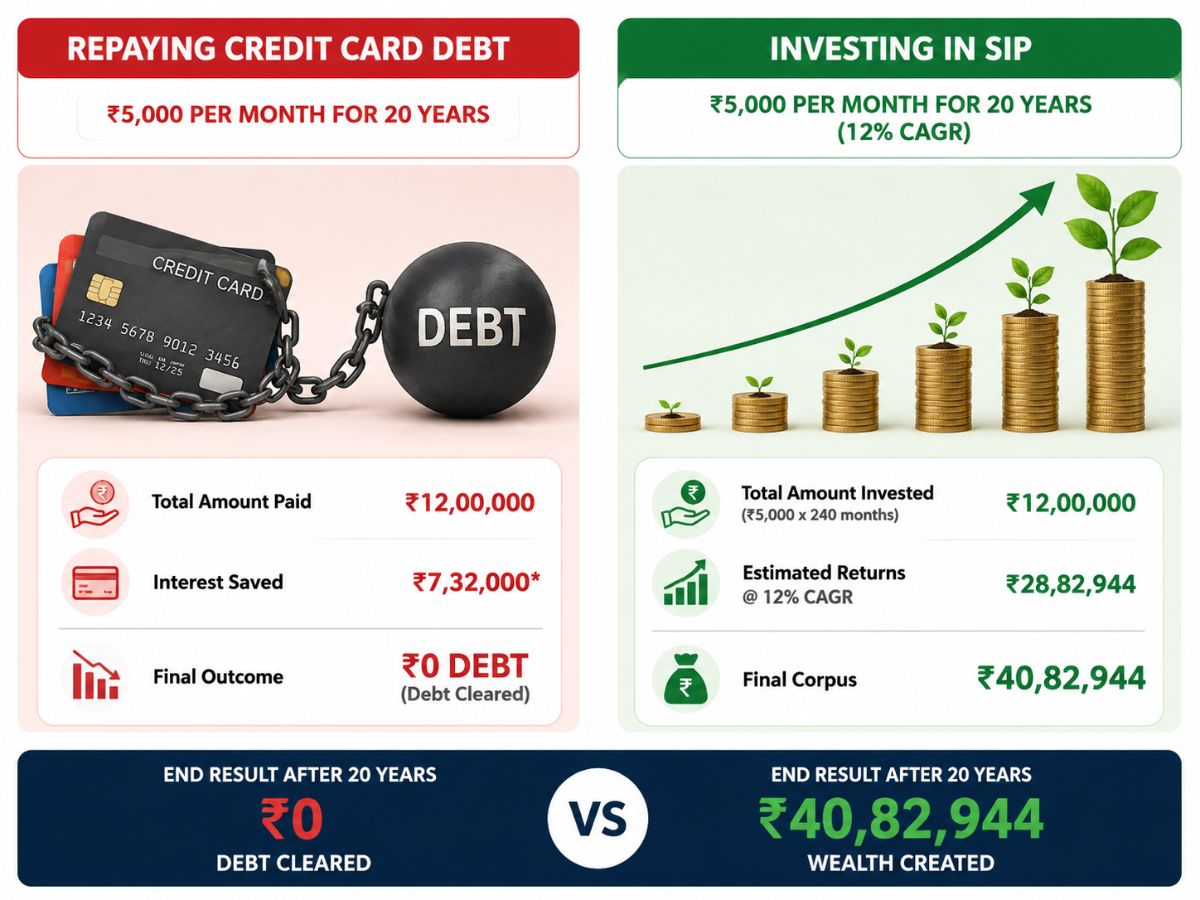

Side by side: the same ₹5,000 per month as debt repayment vs as investment

This is the most useful way to feel the real cost of bad debt — not as an interest rate percentage, but as what the same money could have become.

| Credit card EMI (bad debt) | SIP in index fund (investing) | |

| Monthly amount | ₹5,000 | ₹5,000 |

| Where it goes | Repaying ₹50,000 borrowed at 42% p.a. | Growing at ~12% CAGR (Nifty 50 historical) |

| After 5 years | Debt cleared — net worth: ₹0 gain | Estimated corpus: ~₹4,08,000 |

| After 10 years | If cycle repeats: ₹0 again | Estimated corpus: ~₹11,61,000 |

| After 20 years | Continuous EMI drain | Estimated corpus: ~₹49,96,000 |

| What ₹5,000/month builds | Nothing — it unbuilds | ₹49.96 lakh over 20 years |

The last row is the one that matters. ₹5,000 per month trapped in a debt repayment cycle builds nothing. The same ₹5,000 invested consistently over 20 years — as explored in our article on the power of SIP — can produce close to ₹50 lakh. That gap — roughly ₹50 lakh — is the actual cost of the debt trap over a 20-year horizon, not just the interest paid on the loan.

This is also why the order of financial priorities matters. Building an emergency fund first means you never need to reach for a credit card in a crisis. Clearing bad debt before starting to invest aggressively removes the drag. And understanding how compound interest works in both directions — growing your investments and multiplying your debt — makes the stakes of each borrowing decision much clearer.

Before you borrow: three questions worth answering

No article can tell you whether a specific loan is right for your situation. But these three questions, answered honestly, will tell you more than the interest rate alone.

1. What is this money going to do?

If the answer is “build an asset”, “reduce a higher-cost liability”, or “generate income” — the debt has a productive purpose. If the answer is “fund an experience” or “buy something I want now” — you are choosing consumption credit. That is not automatically wrong, but it should be a conscious choice made with full awareness of the cost, not a default response to an available credit limit.

2. What is the effective interest rate — not just the headline rate?

Banks often advertise a monthly rate, not the annual rate. 3% per month sounds manageable. It is 36% per year — and with processing fees and GST, the actual cost can be higher. Before taking any loan, ask for the annual percentage rate (APR) inclusive of all fees. Compare this against what the same money would return if invested — using the RBI’s EMI calculator or a loan comparison tool gives you a more complete picture than the headline rate alone.

3. What does this do to your CIBIL score if something goes wrong?

Every loan you take is reported to credit bureaus. A missed EMI stays on your CIBIL report for years and affects every future borrowing cost. Before committing to an EMI, check whether your monthly cash flow can comfortably absorb it even in a difficult month — one with an unexpected medical expense, a delayed salary, or a reduced bonus. If the only way the EMI fits is in a best-case income scenario, the loan is carrying risk your cash flow cannot absorb.

Questions people ask about debt

Is a home loan always good debt?

Not always. A home loan becomes bad debt when the EMI exceeds 40% of take-home pay and crowds out all investing and saving. Or when the property is bought in a location with weak appreciation prospects purely for speculation. Or when no emergency fund exists and one disrupted income month means missing an EMI. A home loan is good debt when the EMI is manageable, the property serves a real need, and it does not eliminate your ability to invest simultaneously.

Should I invest or repay debt first?

The answer depends on the interest rate on your debt relative to the expected return on your investment. If you carry credit card debt at 36–42%, no investment reliably outperforms that — clear the debt first. If you have a home loan at 9% (or lower effective rate after tax benefits), and your SIP in an index fund earns 12% CAGR historically, simultaneously investing while making regular EMI payments may make more sense than prepaying aggressively. This is an informational framework — the right answer depends on your specific situation and risk tolerance.

What is a debt trap and how do I know if I am in one?

A debt trap is when your income is no longer sufficient to service your debt without taking on more debt. Signs to watch for: you are paying the minimum due on one credit card using another card or a personal loan, your total EMI obligations exceed 50% of take-home pay, you have taken a personal loan to pay off a credit card but the credit card balance has grown again, or you are unable to save anything because all surplus income goes to repayments.

Is it a good idea to take a personal loan to invest in the stock market?

This is a high-risk approach that most financial planners caution against — and NiveshKarlo cannot recommend it. Markets can fall 30–40% in a short period, as happened in 2020. A personal loan at 12–15% charges you regardless of what the market does. If the market falls, you still owe the EMI. The combination of leverage and market volatility can result in a significantly worse financial position than not investing at all.

How does debt affect my CIBIL score?

Every loan and credit card are reported to CIBIL and other bureaus. Timely payment of all EMIs and full credit card outstanding improves your score. Missed payments, high credit utilisation (above 30% of your card limit), and multiple loan applications in a short period reduce it. A high CIBIL score (750+) gets you lower interest rates on future borrowing — sometimes 1–2% lower than the standard rate — which compounds over a long loan tenure into significant savings.

Disclaimer: This article is for educational and informational purposes only. It does not constitute financial advice or a recommendation to take, repay, or avoid any specific loan or financial product. All interest rates are indicative as of May 23, 2026 and are subject to change. Actual rates depend on individual credit profile and lender policies. NiveshKarlo does not endorse any specific lender or financial institution. All examples are illustrative only. Please consult a qualified financial advisor for guidance specific to your situation.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.