Term Insurance: How Much Cover Do You Actually Need?

“Buy cover worth 10-20 times your income” is the most repeated piece of insurance advice in India. It is also, for most people, not specific enough to act on. Here is what three different calculation methods actually produce for one household — and why the differences between them matter more than any single number.

Transparency: AI-assisted draft reviewed by the NiveshKarlo team. All premium ranges, multiplier guidance, and tax rules were live-verified on June 15, 2026. Informational only — not insurance advice.

Arjun is 34. He works in IT, earns ₹18 lakh a year, has a wife who works part-time, two kids — aged 6 and 3 — and a home loan with 14 years remaining. Three years ago, an agent sold him a term plan with ₹50 lakh cover, calculated as roughly 3x his salary at the time. He has paid the premium every year since without thinking about it again.

This week, a colleague mentioned they had just bought a ₹2 crore term plan. Arjun did the maths — that colleague earns about the same as him. He felt suddenly underinsured, and briefly considered buying another large policy on the spot.

Neither the ₹50 lakh nor the ₹2 crore figure is necessarily right or wrong. What both numbers have in common is that they were not actually calculated for the person holding them — they were approximations based on a rule of thumb, applied without the underlying maths. This article walks through what the maths actually says for someone in Arjun’s position, using three distinct methods that most term insurance calculators in India offer — and what to do when, as is almost always the case, the three methods disagree.

The three methods — and why they don’t agree

Most Indian term insurance calculators — HDFC Life, PolicyBazaar, Axis Max Life, and independent tools — offer some combination of three approaches. They are not alternative ways of arriving at the same number. They measure different things, which is precisely why they produce different answers.

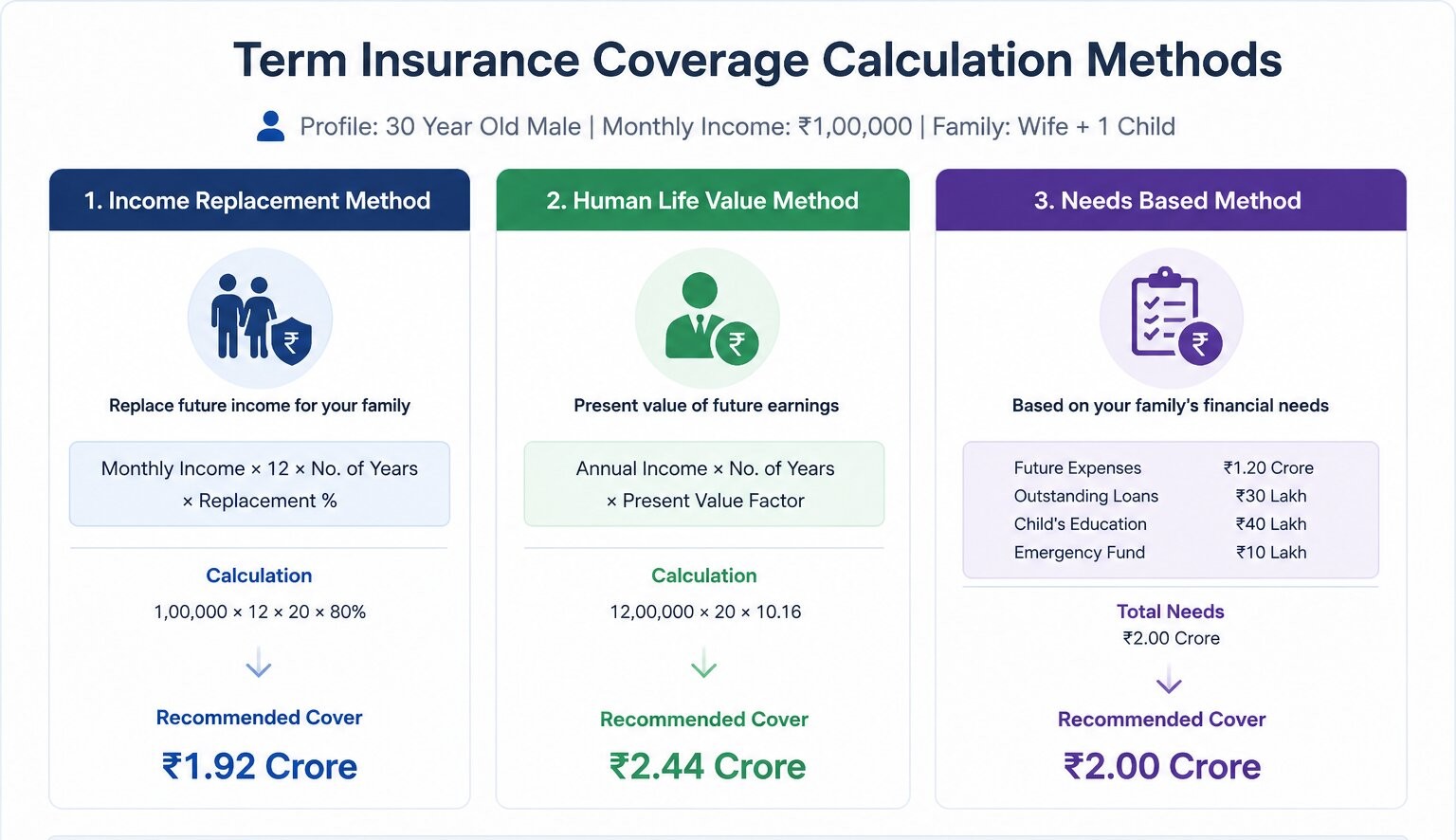

Method 1: Income replacement

This is the method behind the famous “10-20x your annual income” rule. The logic: if Arjun were to pass away, his family would lose his income stream. A lump sum invested conservatively should be able to replace that income for a meaningful number of years. The multiplier typically scales with age — 15-20x for someone in their early career, lower for someone closer to retirement, because a younger person has more income-earning years ahead of them that need replacing.

For Arjun, at 34 with an income of ₹18 lakh, a multiplier of around 15x (reflecting his age bracket) gives a figure of ₹2.7 crore. This is close to what his colleague has — which is exactly why income replacement, applied without further thought, can lead two people earning similar salaries toward similar cover amounts despite having very different family situations.

Method 2: Human Life Value (HLV)

HLV is more granular. Instead of a flat multiplier, it calculates the present value of Arjun’s future net earnings — his income minus his own living expenses, projected until retirement, then discounted back to today’s value using an assumed rate of return. This is the method recommended by IRDAI as a framework, and it accounts for the actual number of years until retirement, expected income growth, and a discount rate — rather than a single fixed multiplier.

For Arjun, with 26 years until a typical retirement age of 60, even modest assumptions about income growth and discount rates produce an HLV figure that can be meaningfully different from the income replacement number — sometimes higher, because it captures decades of future earning potential, and sometimes lower, because the discounting reduces the value of money far in the future.

Method 3: Needs-based (the bottom-up approach)

This method ignores income entirely and instead adds up specific obligations: the outstanding home loan balance, the cost of both children’s education through to a postgraduate degree, a buffer for the family’s living expenses for a defined number of years, and any other large liabilities. It is the most concrete of the three methods because every number in it corresponds to an actual, nameable expense — not a projection.

For Arjun, this looks like: ₹62 lakh outstanding home loan, an estimated ₹40 lakh per child for education (₹80 lakh total, spread over the next 15-20 years), and roughly ₹54 lakh for 5 years of family living expenses at his current household spending rate. That totals approximately ₹1.96 crore — a number that, unlike the other two, is built entirely from things Arjun could list on paper without a calculator.

Image Source: AI

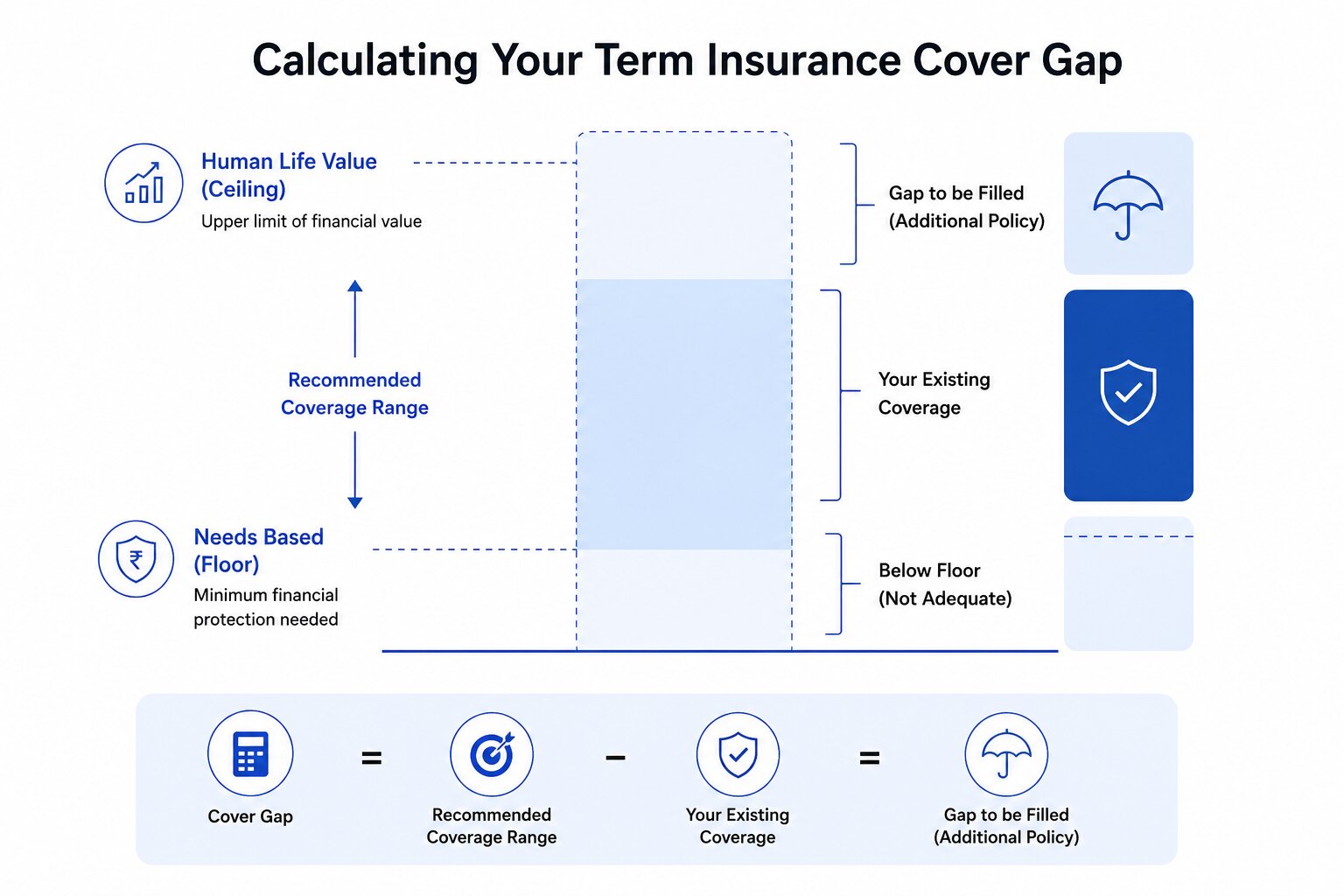

Arjun’s three numbers — and what the gap between them means

| Method | Arjun’s result | What it captures |

| Income replacement (15x) | ₹2.70 crore | A simple multiple of current income, adjusted for age bracket |

| Human Life Value | ₹3.10 crore (illustrative) | Present value of future earnings minus personal expenses, discounted |

| Needs-based | ₹1.96 crore | Sum of specific obligations: loan, education, living expenses buffer |

Three methods, three numbers, a spread of over ₹1 crore between the lowest and highest. This is normal — and it is also where most people stop, pick whichever number feels most comfortable (often the lowest), and move on.

The more useful question is not “which number is correct” but “why do they differ, and what does that difference tell me about my situation specifically?”

| Reading the gap, for Arjun specifically: The needs-based number (₹1.96 crore) is the LOWEST of the three. This means Arjun’s specific, nameable obligations are comfortably covered even by the smallest estimate. That is reassuring — it sets a credible floor. The HLV number (₹3.10 crore) is the HIGHEST. This is largely driven by 26 remaining earning years. The further someone is from retirement, the larger this number tends to be relative to the needs-based figure — because there is simply more future income to replace. The income replacement number (₹2.70 crore) sits between the two — which is often the case, since age-adjusted multipliers are themselves a rough proxy for the HLV calculation, just without the granular inputs. For Arjun, a cover amount in the ₹2.5-3 crore range — between the needs-based floor and the HLV ceiling — covers both his concrete obligations and a substantial share of his future earning potential. His CURRENT ₹50 lakh cover, bought three years ago at a much lower salary, covers roughly 17-25% of any of these three numbers. |

Why Arjun’s existing ₹50 lakh policy is not ‘3x income’ anymore

When Arjun bought his ₹50 lakh policy three years ago, his salary was around ₹16.5 lakh — so the policy was roughly 3x his income at the time. Three things have changed since then, none of which his policy adjusted for automatically:

- His income has grown. From ₹16.5 lakh to ₹18 lakh — a modest increase, but every increase widens the gap between his cover and any income-based recommendation, because the recommendation scales with income while the policy’s sum assured is fixed at purchase.

- His liabilities have changed shape. Three years ago his home loan balance was higher; today it is ₹62 lakh and falling. But his children are three years closer to expensive education years, and education inflation in India has historically outpaced general inflation.

- Three years of his working life have passed. In HLV terms, this technically reduces the total future-earnings figure slightly — but the effect of this is dwarfed by the income growth and the approaching education costs.

None of this means Arjun’s original policy was a mistake. It means term insurance cover is not a one-time decision — it is a number that should be revisited at major life events: a salary increase, a new loan, the birth of a child, or simply every 3-5 years as a check-in. The same logic applies to an emergency fund — both exist to protect a family’s finances from a shock, and both need to be resized as the underlying financial picture changes.

Turning three numbers into one decision

Having three numbers is more useful than having one — but at some point, a single sum assured has to be chosen for a policy application. Here is how someone in Arjun’s position might reason through it, without it being a recommendation of any specific amount.

- Start from the needs-based floor. This is the number built from things that must be paid regardless of anything else — the outstanding loan, in particular, is a fixed, contractual obligation that does not disappear if income stops.

- Add a buffer toward the HLV figure based on time horizon. Someone 25+ years from retirement has more reason to lean toward the higher end of the range than someone 10 years out, because there is more future income at stake.

- Account for what already exists. Arjun’s existing ₹50 lakh policy does not need to be replaced — it can be supplemented with an additional policy for the gap. Buying a second term policy alongside an existing one is common and straightforward; insurers do not require previous policies to be cancelled.

- Reassess the premium against the budget — but don’t let premium affordability alone set the cover amount. A ₹1 crore term plan for a 30-year-old non-smoker male costs roughly ₹8,000-12,000 per year — the cost scales with cover, but term insurance remains one of the most cost-efficient products available precisely because the premium-to-cover ratio stays favourable even at higher sums assured.

Image Source: AI

Two factors that change the premium more than most people expect

Smoking status

A smoker can see up to a 100% increase in premium for the same sum assured and policy term compared to a non-smoker, according to HDFC Life’s published rate structures. This is not a minor adjustment — it can mean the difference between a ₹1 crore policy costing ₹10,000/year versus ₹20,000/year. For someone who has recently quit smoking, insurers may reassess risk classification at renewal or on a new application after a sustained tobacco-free period, though this varies by insurer and is not automatic.

Buying early versus buying later

Term insurance premiums are locked in at the age of purchase for level-term policies — meaning a policy bought at 30 for a 30-year term has a fixed annual premium that does not increase as the policyholder ages within that term. Buying the same cover later, at 40, means a materially higher starting premium, because the insurer’s risk assessment is based on age at entry. This is one of the few places in personal finance where ‘buy now’ is straightforwardly better than ‘wait and buy more later with a higher salary’ — the cost of waiting compounds in the form of permanently higher premiums for any policy bought later.

The Section 80C angle — and why it shouldn’t drive the decision

Term insurance premiums qualify for deduction under Section 80C, up to ₹1.5 lakh, provided the premium does not exceed 10% of the sum assured (for policies issued after April 2012). For most term plans, premiums are well below this threshold relative to the cover amount, so the deduction applies in full to whatever premium is paid.

This is worth knowing, but it should not be the primary reason to buy term insurance, or to size the cover. The 80C limit is shared across multiple instruments — EPF, PPF, ELSS, and others — so for many people the ₹1.5 lakh limit is already filled by retirement contributions alone, making the tax benefit on insurance premiums marginal. The cover amount should be driven by the three methods above; the tax deduction is a secondary benefit that applies regardless of which cover amount is chosen.

Also Read: National Pension Scheme(NPS): A Smart Way To Build Your Retirement Fund | How to Reduce Taxes on Mutual Fund Investments

Questions people ask when sizing their cover

Is 10-20x my annual income the right amount of term insurance cover?

It is a reasonable starting estimate, but as the three-method comparison above shows, it can differ substantially from a needs-based or HLV calculation for the same person. The multiplier method is most useful as a sanity check against the other two methods, not as a final answer on its own. If all three methods point to a similar range, that range is likely a reasonable target. If they diverge significantly — as they often do — the reasons for the divergence (years to retirement, size of specific obligations) are informative.

Should I buy multiple term insurance policies or one large one?

Both are common in India. Buying multiple smaller policies from different insurers can provide some diversification in claim-settlement risk, though all insurers in India are regulated by IRDAI and claim settlement ratios are publicly disclosed. A single larger policy is operationally simpler — one premium, one renewal date, one set of paperwork for beneficiaries to navigate. There is no rule against holding multiple term policies simultaneously, and insurers do not require disclosure of other term policies to affect pricing in most cases, though total cover across all policies may be capped relative to income by some insurers.

Does term insurance cover need to reduce as my home loan reduces?

Not automatically, and this is a common point of confusion. A standard level-term policy maintains the same sum assured throughout the term, regardless of how the home loan balance changes. Some insurers offer ‘decreasing term’ or mortgage-specific policies where the cover reduces in line with a loan schedule — these typically have lower premiums but also lower cover in later years. Whether a reducing structure makes sense depends on whether the loan is the only major obligation being covered — for someone like Arjun with ongoing education costs and living expenses that don’t reduce over time, a level cover that doesn’t shrink may be more appropriate.

How often should term insurance cover be reviewed?

There is no fixed rule, but major life events are natural trigger points: a significant salary increase, taking on a new loan, the birth of a child, or a spouse’s change in employment status. In the absence of a specific trigger, reviewing every 3-5 years — similar to how an investment portfolio might be reviewed — ensures the cover amount has not drifted too far from current needs, as happened with Arjun’s three-year-old policy.

Can I get term insurance if I already have some savings and investments?

Yes — term insurance and investments serve different purposes and are not substitutes for each other. Investments, including those built through SIPs over time, grow a corpus for the policyholder’s own future use. Term insurance provides an immediate lump sum to dependents specifically in the event of the policyholder’s death during the term — a risk that no amount of existing savings can fully offset for a family in the early years of wealth-building, when the gap between current savings and long-term goals is largest.

Disclaimer: This article is for educational and informational purposes only. It does not constitute insurance advice or a recommendation for any specific cover amount, policy, or insurer. The example of ‘Arjun’ is illustrative and fictional. All premium ranges and figures are indicative as of June 15, 2026 and vary by insurer, health profile, and underwriting. Term insurance is subject to underwriting and claim approval based on policy terms and disclosures. NiveshKarlo does not endorse any specific insurer or policy. Please consult a licensed insurance advisor or use IRDAI-approved comparison tools before purchasing any policy.

Hello there, my name is Phulutu, and I am the Head Content Developer at Nivesh Karlo. I have 13 years of experience working in fintech companies. I have worked as a freelance writer. I love writing about personal finance, investments, mutual funds, and stocks. All the articles I write are based on thorough research and analysis. However, it is highly recommended to note that neither Nivesh Karlo nor I recommend any investment without proper research, and to read all the documents carefully.